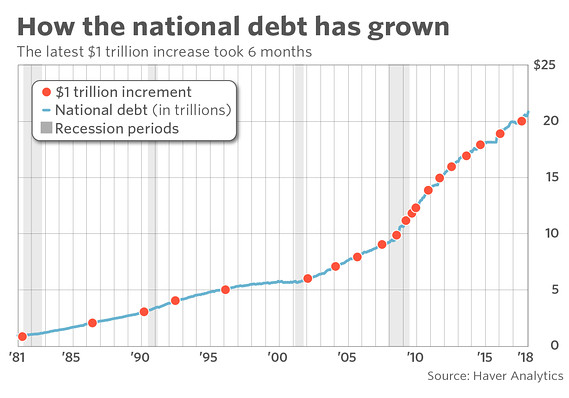

As noted by Robert Schroeder:

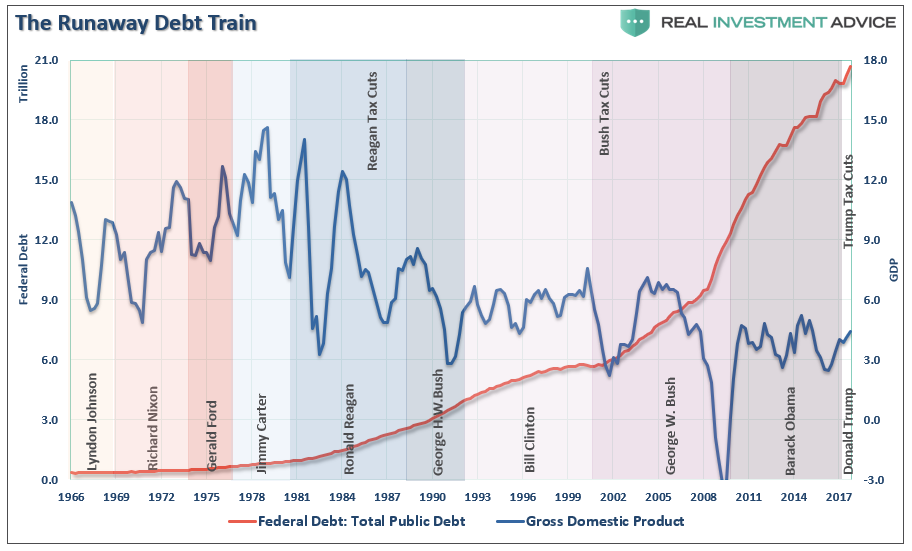

“Last week, the debt hit $21 trillion for the first time, rising from the $20 trillion mark it notched on Sept. 8. The debt is guaranteed to go higher, with President Donald Trump having signed a debt-limit suspension in February, allowing unlimited borrowing through March 1, 2019. Economists expect wider deficits to result from the tax cut Trump signed in December.

While a trillion-dollar increase over roughly six months isn’t unprecedented — there was one in 2009, during the Great Recession, and another in 2010 — it’s certainly fast.”

Excessive borrowing by companies, households or governments lies at the root of almost every economic crisis of the past four decades, from Mexico to Japan, and from East Asia to Russia, Venezuela, and Argentina. But it’s not just countries, but companies as well. You don’t have to look too far back to see companies like Enron, GM, Bear Stearns, Lehman and a litany of others brought down by surging debt levels and simple “greed.” Households too have seen their fair share of debt burden related disaster from mortgages to credit cards to massive losses of personal wealth.

It would seem that after nearly 40-years, some lessons would have been learned.

Apparently not, as Congressional lawmakers once again are squabbling on not how to “save money” and “reduce the federal debt,” but rather “damn the debt, full speed ahead with spending.”

Such reckless abandon by politicians is simply due to a lack of “experience” with the consequences of debt.

In 2008, Margaret Atwood discussed this point in a Wall Street Journal article:

“Without memory, there is no debt. Put another way: Without story, there is no debt.

A story is a string of actions occurring over time — one damn thing after another, as we glibly say in creative writing classes — and debt happens as a result of actions occurring over time. Therefore, any debt involves a plot line: how you got into debt, what you did, said and thought while you were in there, and then — depending on whether the ending is to be happy or sad — how you got out of debt, or else how you got further and further into it until you became overwhelmed by it, and sank from view.”

The problem today is there is no “story” about the consequences of debt in the U.S. While there is a litany of other countries which have had their own “debt disaster” story, those issues have been dismissed under the excuse of “yes, but they aren’t the U.S.”

As I discussed recently in relation to the tax cut/reform package passed by Congress last year:

“Of course, the real question is how are you going to ‘pay for it?’

Even as Kevin Brady noted in our interview, when I discussed the ‘fiscal’ side of the tax reform bill, without achieving accelerated rates of economic growth – ‘the debt will balloon.’”

It is pretty simplistic math:

Cut revenue by $2 Trillion + add $2 Trillion is spending = $4 Trillion shortfall.

While it is true the debt doesn’t have to be repaid today, it does have to be serviced.

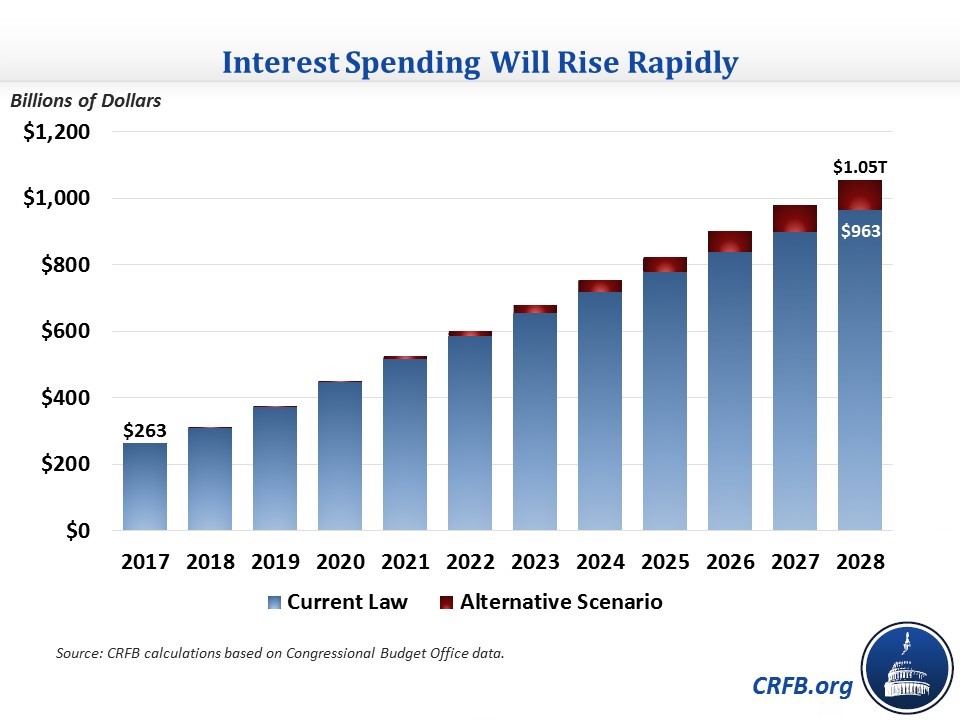

Committee for a Responsible Federal Budget president Maya MacGuineas recently published a commentary describing how interest is on a path to quadruple over the next decade, reaching over $1 trillion per year.

“Interest on the debt is the fastest growing part of the budget. While interest had already been projected to rise rapidly the recent tax and budget deals will significantly accelerate that growth. As a result, our latest estimate finds interest costs will almost quadruple between 2017 and 2028 in dollar terms and reach their highest share of Gross Domestic Product (GDP) in history.

As recently as last June, the Congressional Budget Office (CBO) projected interest spending would grow to above $800 billion and nearly 3 percent of GDP by 2027 as a result of rising interest rates and growing debt levels. Since then, lawmakers have added an additional $2.4 trillion to deficits over the next decade, and it will most certainly result in higher interest payments.

By our estimates, annual interest spending will rise from $263 billion (1.4 percent of GDP) in 2017 to $965 billion, or 3.3 percent of GDP, in 2028. The 3.3 percent of GDP total for interest in 2028 would be the highest on record. The previous record was 3.2 percent of GDP in 1991, a time when debt as a percent of GDP was much lower but interest rates were much higher. Under our “Alternative Scenario,” which assumes policymakers borrow an additional $3.6 trillion through 2028, interest spending will rise to $1.05 trillion, or 3.6 percent of GDP, by 2028.”

The Wrong Kind Of Debt

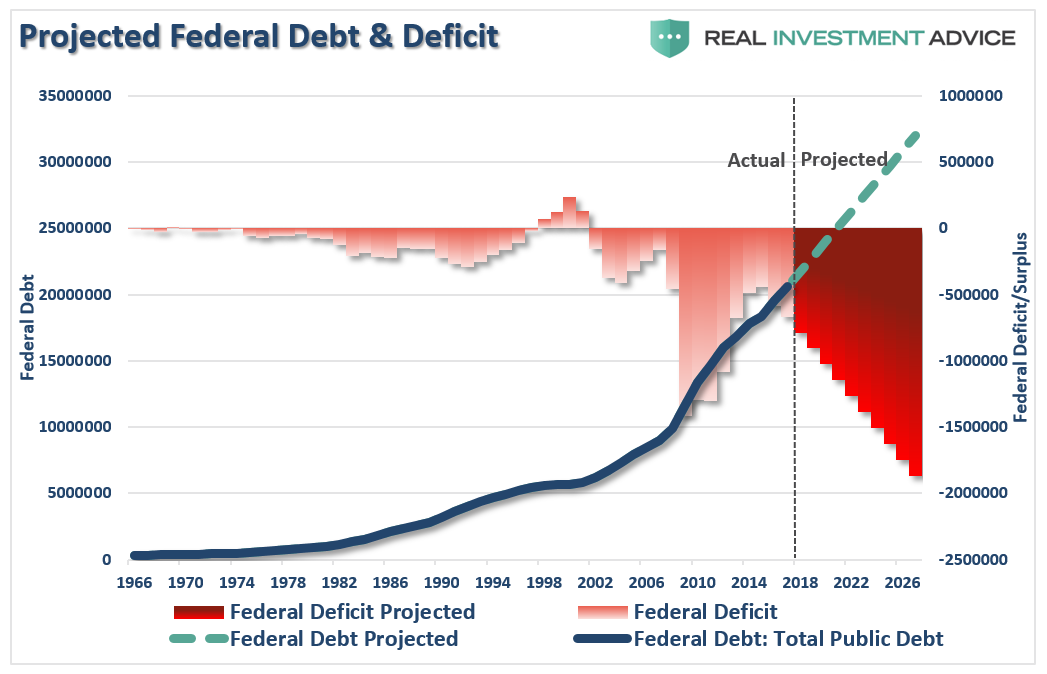

By the end of 2018, the United States, based on its current trajectory, will achieve a new TOP 10 ranking.

“Tell us what we’ve won Bob:

Coming in at #10 – the United States, at 111%, gets nothing but the privilege of being on the list of countries with the highest debt/GDP ratios.”

According to Keynesian theory, some microeconomic-level actions, if taken collectively by a large proportion of individuals and firms, can lead to inefficient aggregate macroeconomic outcomes, where the economy operates below its potential output and growth rate (i.e. a recession).

Keynes contended:

“A general glut would occur when aggregate demand for goods was insufficient, leading to an economic downturn resulting in losses of potential output due to unnecessarily high unemployment, which results from the defensive (or reactive) decisions of the producers.”

In other words, when there is a lack of demand from consumers due to high unemployment, the contraction in demand would force producers to take defensive actions to reduce output.

In such a situation, Keynesian economics states:

“Government policies could be used to increase aggregate demand, thus increasing economic activity and reducing unemployment and deflation. Investment by government injects income, which results in more spending in the general economy, which in turn stimulates more production and investment involving still more income and spending and so forth. The initial stimulation starts a cascade of events, whose total increase in economic activity is a multiple of the original investment.”

Keynes’ was correct in his theory”

In order for government deficit spending to be effective, the “payback” from investments being made through debt must yield a higher rate of return than the debt used to fund it.

Read that again.

The problem is that government spending has shifted away from productive investments that create jobs (infrastructure and development) to primarily social welfare and debt service which has a negative rate of return.

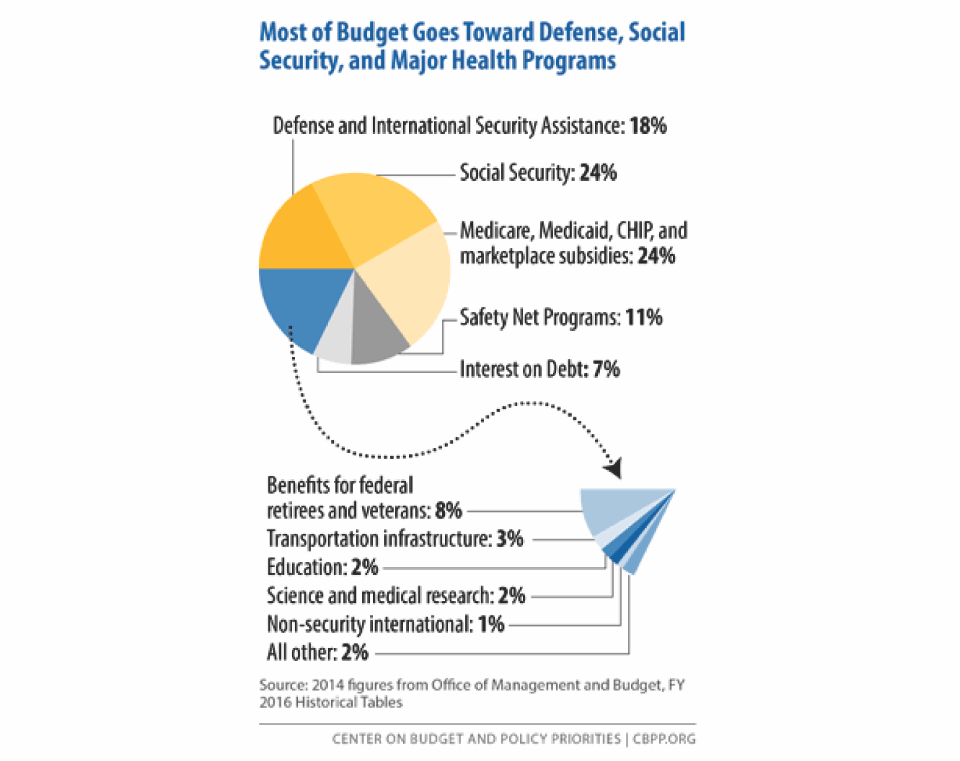

According to the Center On Budget & Policy Priorities, nearly 75% of every tax dollar goes to non-productive spending.

In 2017, the Federal Government spent an estimated $4.3 Trillion which was equivalent to roughly 21% of the nation’s entire GDP. Of that total spending, an estimated $3.68 Trillion was financed by Federal revenues leaving $657 billion to be financed through debt. In other words, it took almost all of the revenue received by the Government just to cover social welfare programs and service the interest on the debt.

Therefore, the larger the balance of debt becomes, the more economically destructive it is by diverting an ever growing amount of dollars away from productive investments to service payments.

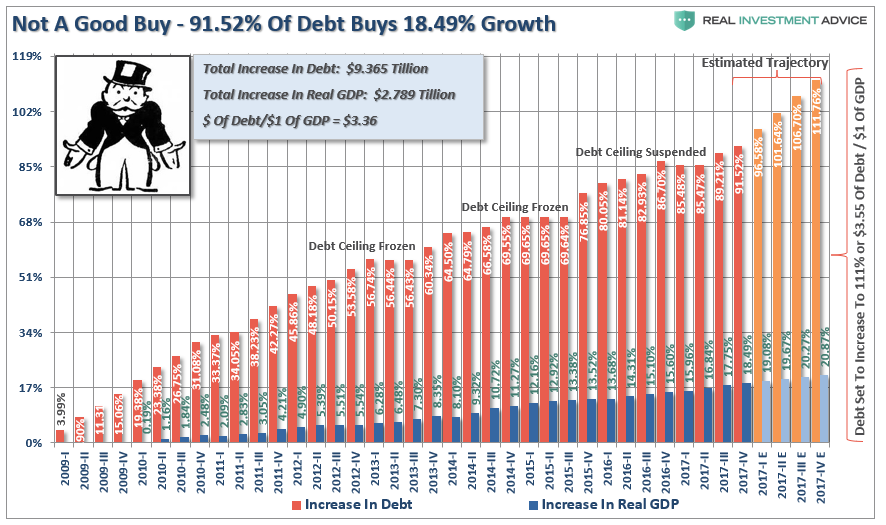

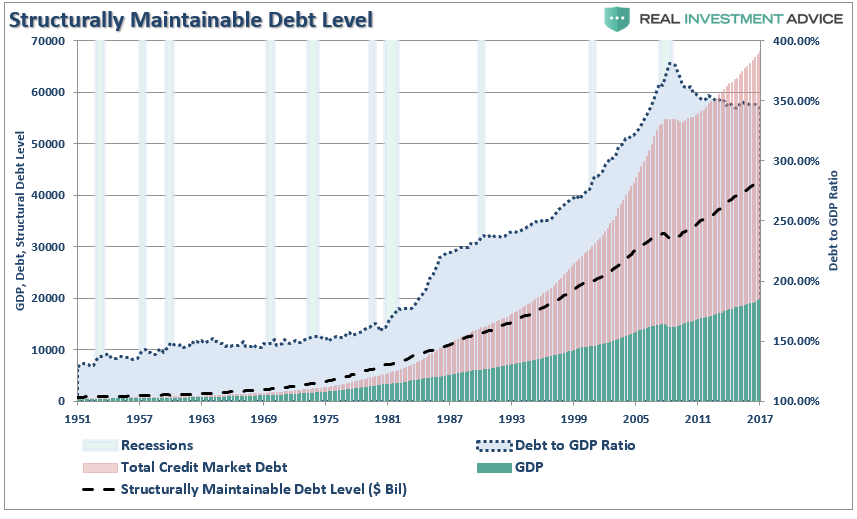

The relevance of debt growth versus economic growth is all too evident as shown below. Since 1980, the overall increase in debt has surged to levels that currently usurp the entirety of economic growth. With economic growth rates now at the lowest levels on record, the growth in debt continues to divert more tax dollars away from productive investments into the service of debt and social welfare.

It now requires $3.71 of debt to create $1 of economic growth.

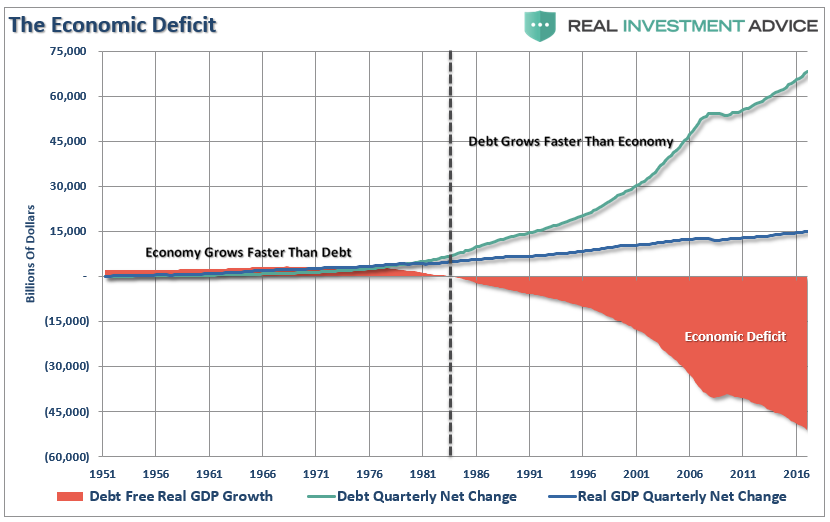

In fact, the economic deficit has never been greater. For the 30-year period from 1952 to 1982, the economic surplus fostered a rising economic growth rate which averaged roughly 8% during that period. Today, with the economy growing at an average rate of just 2%, the economic deficit has never been greater.

The unsustainable credit-sourced boom, which leads to artificially stimulated borrowing, has sought out diminishing investment opportunities. Ultimately these diminished investment opportunities lead to widespread mal-investments. Not surprisingly, we clearly saw it play out “real-time” in everything from sub-prime mortgages to derivative instruments which were only for the purpose of milking the system of every potential penny regardless of the apparent underlying risk.

We see it again today with companies issuing massive amounts of debt to buy back unprecedented levels of outstanding shares and issues dividends.

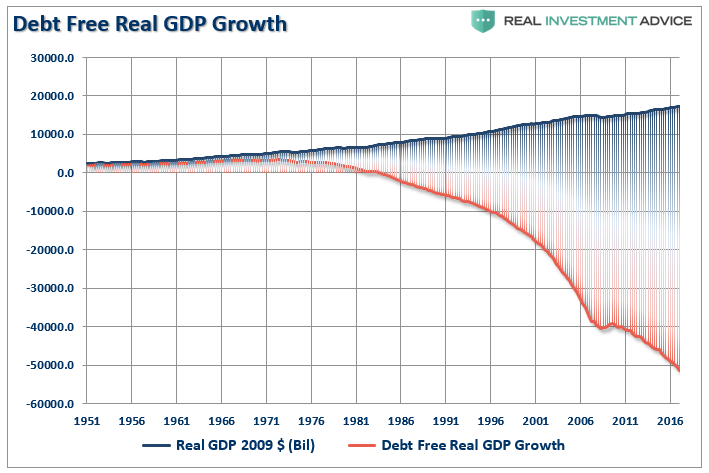

The illusion of economic growth has been fueled by ever increasing levels of debt to support consumption. However, if you back out the level of debt you get a better picture of what is actually happening economically.

When credit creation can no longer be sustained the markets must begin to clear the excesses before the cycle can begin again. That clearing process is going to be very substantial. With the economy currently requiring roughly $3.50 of debt to create $1 of economic growth, the reversion to a structurally manageable level of debt would involve a $25 trillion reduction of total credit market debt from current levels.

The economic drag from such a reduction would be a devastating process, and why Central Banks worldwide are terrified of it. In fact, the last time such a reversion occurred it became known as the “Great Depression.”

Now you understand “why,” despite tax cuts and reforms, the economy continues to grow at sub-par levels. Heading into the future, given the Administrations inability to curb their “spending addiction,” it is highly likely we will witness an economy plagued by more frequent recessionary spats, lower equity market returns and a stagflationary environment as wages remain suppressed while costs of living rise.

Sure, $21 trillion isn’t a problem as long as we “print the money” necessary to make those payments. However, the longer-term consequences of doing so has a very negative consequence. One of those consequences is the ongoing detraction from economic growth.

As Ms. Atwood concluded:

“There’s nothing we human beings can imagine, including debt, that can’t be turned into a game — something done for entertainment. And, in reverse, there are no games, however frivolous, that cannot also be played very seriously, and sometimes very unpleasantly.

But when the play turns nasty in dead earnest, the game becomes what Eric Berne calls a ‘hard game.’

In hard games the stakes are high, the play is dirty, and the outcome may well be a puddle of gore on the floor.”

There is likely only one way the current lack of fiscal control turns out. History is replete with countries that have attempted the same. For now, the limits of profligate spending by Washington has not been reached and the ending of this particular story has not yet been written. But it eventually will be.

Just be careful where you step.