The Potential Of A Policy Error Has Risen

Yesterday, the Fed clearly showed they are trapped in their decision to raise rates. Despite an ongoing deterioration in the underlying economic and financial market fabric, Yellen & Co. stayed firm in their commitment to a gradual increase in interest rates.

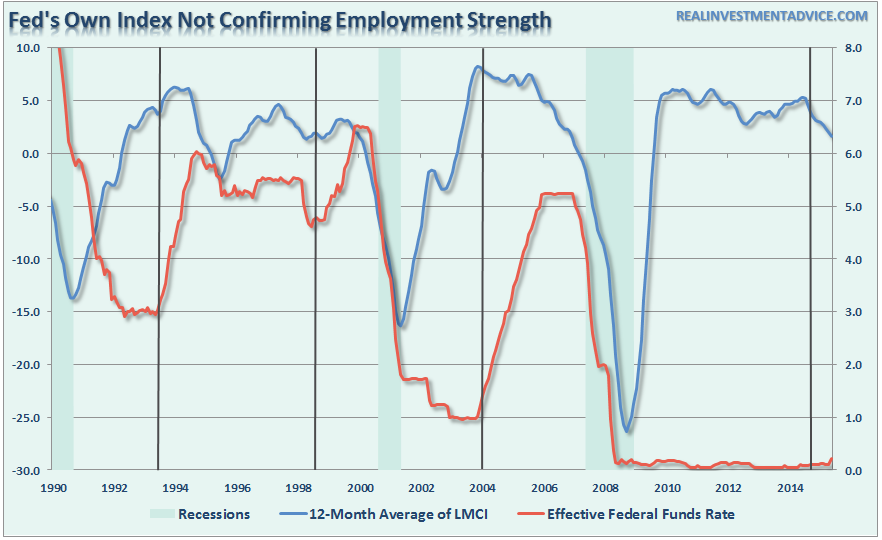

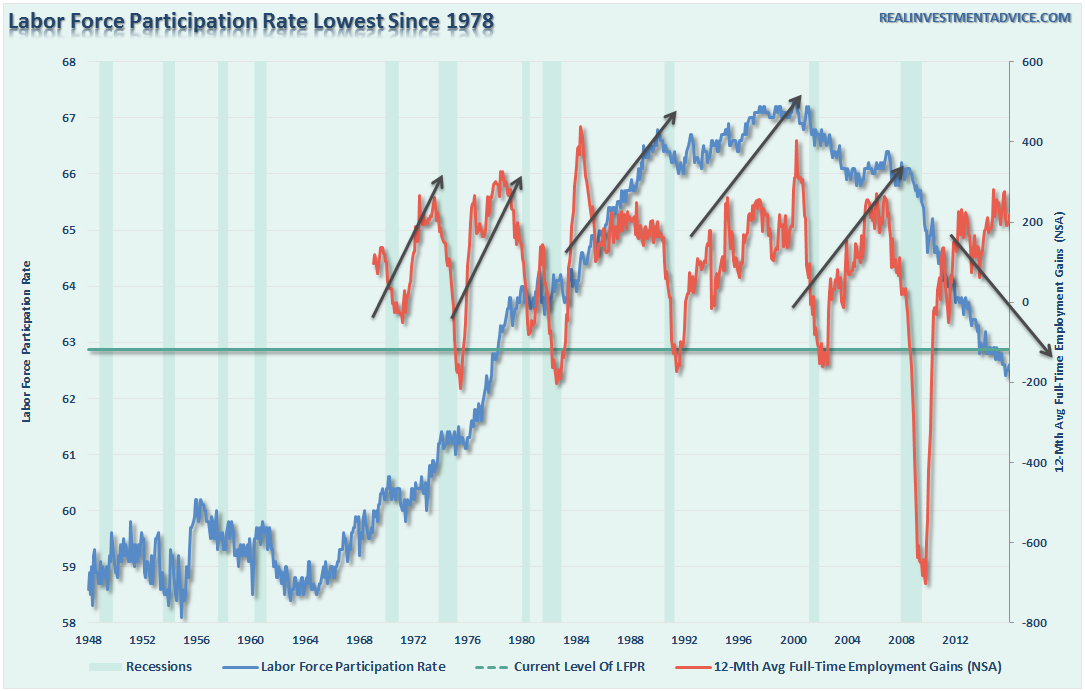

What is most interesting is their focus on headline employment data while ignoring their very own Labor Market Conditions Index (LMCI) which shows a clear deterioration in the employment underpinnings.

But here is the potential problem for the Fed’s dependence on current employment data as justification for tightening monetary policy – it is likely wrong. Economic data is very subject future revisions. While the current employment data has indeed been the strongest since the late 1990’s, there is a probability that the data is currently being overestimated.

The reason is shown in the chart below.

If the employment gains were indeed as strong as the Fed, and the BLS, currently suggest; the labor force participation rate should be rising. This has been the case during every other period in history where employment growth increased. Since the financial crisis, despite employment gains, the labor force participation rate has continued to fall.

This suggests that at some point in the future, we will likely see negative revisions to the employment data showing weaker growth than currently thought.

The issue for the Fed is by fully committing to hiking interest rates, and promoting the economic recovery meme, changing direction now would lead to a loss of confidence and a more dramatic swoon in the financial markets. Such an event would create the very recession they are trying to avoid.

Inflation expectations are also a problem which compounds the probability of a policy error at this point. As Danielle DiMartino Booth, who left the Fed earlier this year, stated:

“Less anticipated was the adamancy of Committee members that inflation would hit their stated goal of ‘two percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further.’

‘Strengthens further?’ Anyone bother to share the last few weekly jobless claims reports with monetary policymakers?

As for inflation’s prospects, a year and a half into crashing oil prices, the FOMC’s use of the word ‘transitory’ leads one to wonder if they are stuck in some space age time warp. Or maybe they declared it Opposite Day but failed to share that with the rest of us.

While the Fed clearly remains giddily detached from reality, the bond market communicated unequivocally what it thinks about the economy’s prospects: the 10-year Treasury closed below the two percent line in the sand that’s been drawn since the start of the year.“

With fourth quarter GDP likely to be closer to 0% than 2%, the Fed has clearly gotten on the wrong side of the economic landscape. This puts the possibility of a monetary policy error at extremely high levels, the outcomes of which have historically been severe.

Houston Has A Problem – Commercial R/E

In February of 2015, I penned the following missive discussing the coming real estate crisis for the Houston market:

“Houston has a problem when it comes to tumbling oil prices.

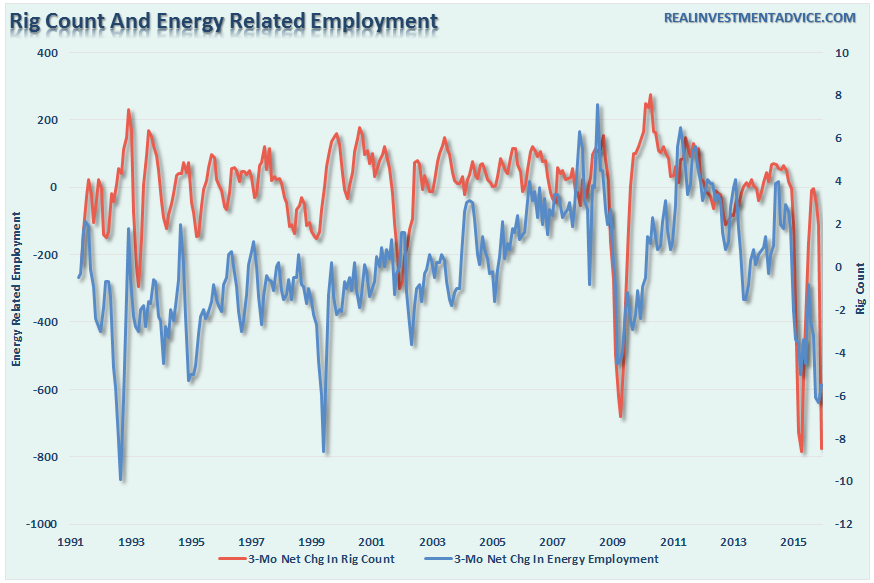

As oil prices rise and fall so does the number of rigs being utilized to drill for oil which ultimately also impacts employment. This is shown in the chart below of rig count versus employment in the oil and gas sector of the economy.”

“Obviously, the drawdown in energy prices is going to start to weigh on the Texas economy rather sharply over the next several months. Several energy companies have already announced layoffs, rig count reductions and budgetary cuts going into 2015. It is still very early in the cycle so it is likely that things will get substantially worse before they get better.”

While much of the mainstream media continues to tout that falling oil prices are good for the economy, (read here for why that is incorrect) the knock-off economic impacts are job losses through the manufacturing sector and all other related industries are quite significant.

However, most importantly as I pointed out at the beginning of 2015:

“One of those areas is commercial real estate. If you look in any direction in Houston, you see nothing but cranes. The last time I saw such an event was just prior to 2008 when I commented then that overbuilding was a sign of the maturity of the boom. The same has happened yet again, and not surprisingly, the “sirens song” has been “this time is different.”

Unfortunately, not only is this time not different, the economic impacts are likely to much more substantial, not only in the Houston economy, but nationwide. To wit:

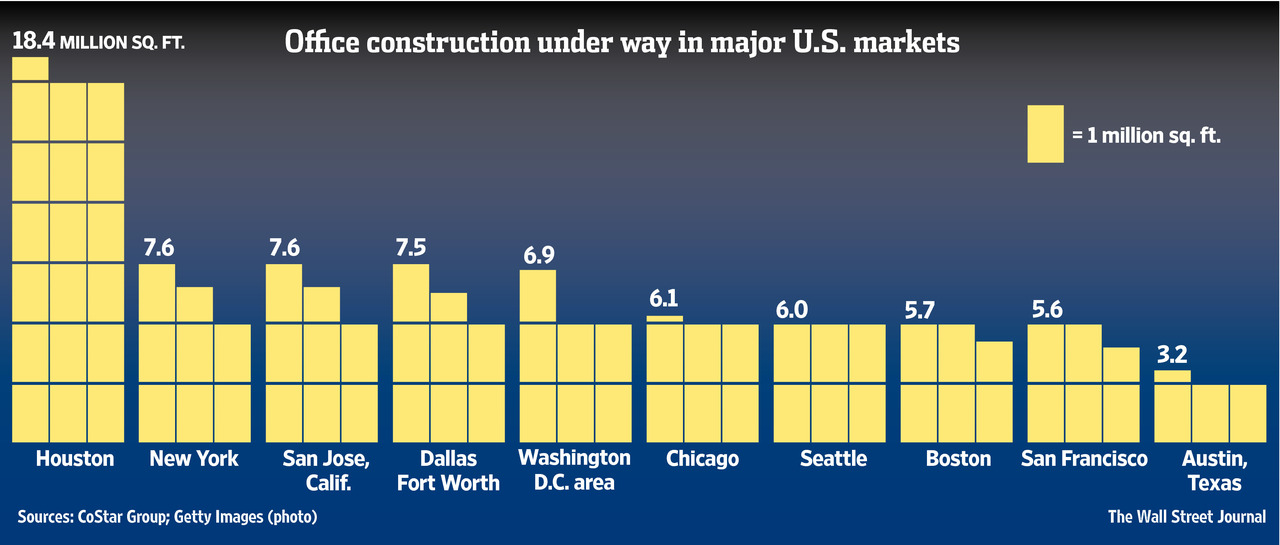

“The jagged skyline of this oil-rich city is poised to be the latest victim of falling crude prices. As the energy sector boomed in recent years, developers flocked to Houston, so much so that one-sixth of all the office space under construction in the entire U.S. is in the metropolitan area of the Texas city.”

But here is the economic problem:

“And as a reminder, every high-paying oil service jobs accounts for up to 4 downstream just as well-paying jobs. Case in point:

The rush of building has created thousands of jobs—not only at building sites, but also at window manufacturers, concrete companies, and restaurants that feed the workers.

But just as the wave of office-space supply approaches, energy companies, including Halliburton Co. , Baker Hughes Inc., Weatherford International and BP PLC, have collectively announced that more than 23,000 jobs would be cut, with many of them expected to be in Houston.

Fewer workers, of course, means less need for office space.“

No one believed me then. However, here is the latest update from real-estate services firm Savills Studly via Business Insider:

“New sublease blocks are expected to hit the market in 2016, particularly in the CBD [Central Business District]. Shell is projected to vacate 250,000 sf in One Shell Plaza and EP Energy, likewise, is anticipated to leave 100,000 sf in the Kinder Morgan Building. Shell would likely also shed space at BG Group Place should its pending $70-billion acquisition of BG Group clear governmental hurdles and finalize.

Many large tenants who paid at the very top of the market in the last few years warehoused space in anticipation of continued headcount growth. As a result, many firms had surplus space even prior to the implementation of layoffs in the last year. In 2016, the office market should see more shadow space listings….

Occupancy, after five years in a row of increases, fell by 1.4 msf (“negative absorption”), the biggest decrease in occupancy since 2009. Going forward, M&A and bankruptcies “will contribute to additional negative absorption” and will hit the vacancy rate. It already spiked to 23.2%.

After a tremendous building boom in 2013 and 2014, a total of 17 msf is expected to hit the market over the next few years, with 7.9 msf scheduled for completion in 2016. Only about two-thirds have been pre-leased. Some of these pre-leased properties will enter the shadow inventory as soon as they’re completed. But 5.5 msf has not been leased.

These new buildings will hit the market at the worst possible time, competing with 7.9 msf of sublease space and large amounts of shadow inventory, during a period of negative absorption.“

While the media and mainstream analysts discount the negative economic impact of falling energy costs, I have personally witnessed it in the mid-80’s, the late 90’s and just prior to 2008. In all cases, the negative outcomes were far worse than predicted which left economists scratching their heads as to what went wrong with their models.

This time won’t be different.

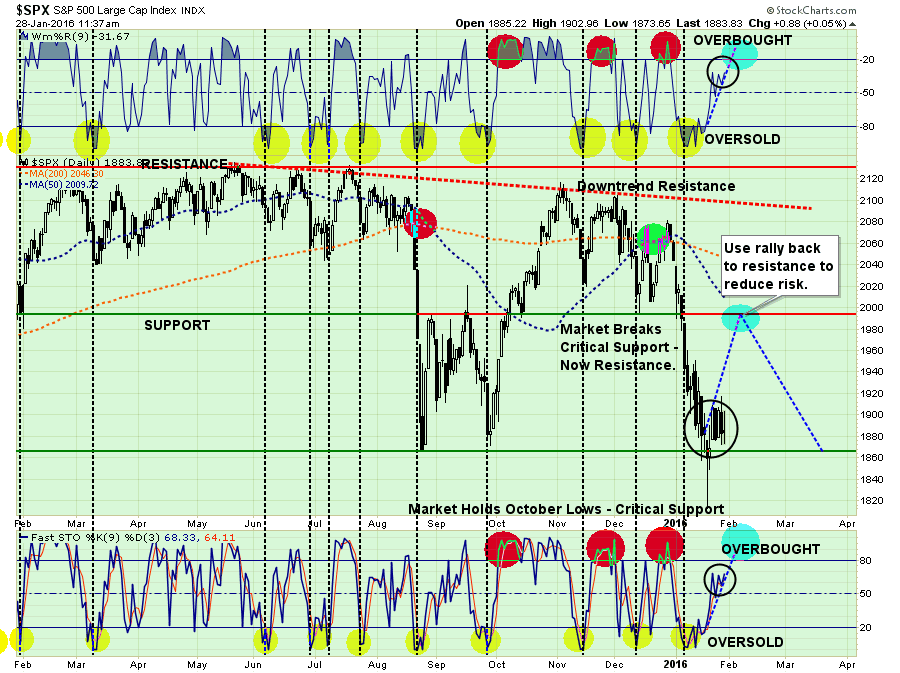

Markets May Not Bounce

Over the last few weeks, I have suggested the markets would likely provide a reflexive rally to allow investors to reduce equity risk in portfolios. This was due to the oversold condition that previously existed which would provide the “fuel” for a reflexive rally to sell into.

I traced out the potential for such a reflexive rally to weeks ago as shown in the chart below.

The oversold conditions that once existed have been all but exhausted at this point due to the gyrations in the markets over the last couple of weeks without the markets making any significant advance.

Just as an oversold condition provides the necessary “fuel” for an advance, the opposite is also true. This almost overbought condition comes at a difficult time as I addressed earlier this week:

“February has followed those 20 losing January months by posting gains 5-times and declining 14-times. In other words, with January likely to close out the month in negative territory, there is a 70% chance that February will decline also.

The high degree of risk of further declines in February would likely result in a confirmation of the bear market. This is not a market to be trifled with. Caution is advised. “

Just some things to think about.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In