This wasn’t supposed to happen. The week was already on a crummy downhill path globally, and emerging-market currencies were blowing up, when on Friday in China the Caixin’s Purchasing Manager’s Index hit the worst level since March 2009; manufacturing is sinking deeper into the mire.

So the Shanghai stock index plunged 4.3% for the day, and 11.5% for the week, to 3,508, closing at the same level as the bottom of its July rout.

The entire machinery that the Chinese government and the People’s Bank of China had set in motion to bail out the markets during the July rout, which had worked for a couple of weeks, has now proven to be useless. And the markets, thought to be controllable by fiat or manipulation, suddenly regained a will of their own.

Other Asian stock markets plunged too: Hong Kong’s Hang Seng dropped 1.5% on Friday and 6.6% for the week; it’s 5.1% in the hole for the year. The Nikkei fell 3% on Friday and 5.3% for the week.

Europe was next. The German Dax, the British FTSE 100, French CAC 40, the Spanish IBEX 35, the Italian FTSE MIB, they all plunged about 3% for the day and lost between 5% and 6.5% for the week, except for the German Dax which lost nearly 8% for the week. It has now plummeted 18% since its dizzying peak in early April. Easy come, easy go.

Have central banks lost their omnipotence?

That despicable, unpredictable force that central banks were thought to have vanquished – markets with a will of their own – ricocheted in its unruly manner around the world.

In Europe and Japan, the central banks are currently engaging in relentless QE programs to inflate stocks, and China is doing a whole lot more, and yet, this debacle! A few more episodes of this – and folks are going to question the omnipotence of central banks, and they’re going to doubt the central banks’ vaunted ability to inflate the markets. If those doubts spread, not even QE can prop up the markets. Omnipotence only works if people believe in it.

For US stocks, an apt close of a lousy week.

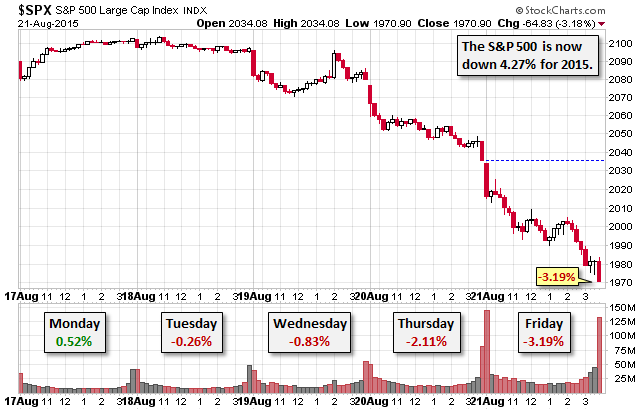

The Dow plunged 541 points to 16,460, or 3.2%, after having already plunged 358 points on Thursday. It’s down 5.8%, for the week, the worst percentage drop since September 2011, and off 10.3% from its peak in May, and thus in a “correction.”

The Nasdaq plummeted 171 points for the day, or 3.5% to 4,706. It too is in a correction, having lost 10% in a month.

The S&P 500 index dropped 65 points, or 3.2%, to close at 1,971, after losing 2.1% on Thursday, and is down 5.8% for the week, also its worst week since September 2011. It’s 4.3% in the hole for the year.

This chart by Doug Short, of Advisor Perspectives, shows the dismal trend for the week. In the bottom section of the chart, note how volume rose sharply each day during the four-day selloff. That’s not necessarily a good omen:

But wait…. The S&P 500 is down only 7.5% from its all-time high, and still not in a correction. Doug Short’s chart of the index shows the selloffs going back to 2007. The last time there was a correction of 10% or more was in 2011. And even that selloff the Fed got ironed out pretty quickly.

Stocks lost their grip into the close. Volume soared. Dip buyers had already checked out. And sellers were lining up to dump their wares so that they could sleep and party over the weekend.

Bill Bonner, Chairman of Bonner & Partners, commented in his mix of cynicism, humor, and razor-sharp observation: “What puzzles us is not why stocks are going down but why anyone thought they were worth so much in the first place.”

It’s just that folks have forgotten after years of QE and ZIRP what a selloff looks and feels like, that stocks can actually decline year-over-year. Folks have come to believe that the Fed will prevent these sort of dastardly events.

But here’s the thing…

All of the gains in the S&P 500 since 2009 piled up when the Fed’s QE and Operation Twist were cranking out trillions of dollars in new play money. But when QE was tapered out of existence last year, the S&P began to lose steam.

ZIRP alone isn’t enough anymore, apparently, to prop up the markets. And now the Fed is even thinking about ending ZIRP….

So Volatility is back with a vengeance.

The CBOE Volatility Index VIX jumped 47% on Friday to 28.2, a level last seen during the heady days of December 2011. For the week, it soared 120%, the largest ever weekly percentage increase.

Nerves had gotten rattled, after years of Fed-induced somnolence, by the insufferable nightmare that central banks might not be omnipotent after all in propping up stock markets forever, and that the markets might be once again developing a will of their own.

“A Global Meltdown…”

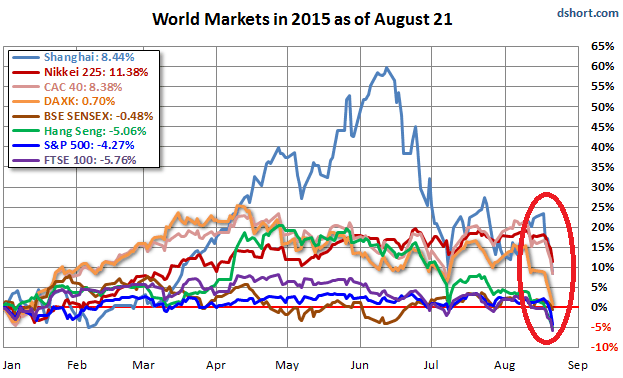

That’s what Doug Short called it in his World Markets Weekend Update. All its eight indexes finished in the red for the week. India’s SENSEX, he points out, “was the top performer, down a ‘mere’ -2.5%.” For the rest, they ranged from the Nikkei’s -5.28% to the Shanghai Composite’s -11.54%. The China bubble and implosion (blue line) is the most salient feature this year. By comparison, the selloff this week looks practically benign:

And oil got hammered for the eighth week in a row.

It was the longest weekly losing streak since March 1986. And on Friday, West Texas Intermediate plunged below the $40-mark intraday, hitting $39.86 before bouncing off to take a breath at $40.29, the worst level since the Financial crisis.

Since mid-June, when the delusions of an oil rebound came to an abrupt end, WTI has plummeted 33.6%.

US drillers have accelerated their drilling programs again. Global production, powered by Saudi Arabia, Russia, the US, and especially Iraq – and soon Iran – gives off no substantive signs of slowing down. Hopes for global demand growth are hitting the realty of economic turmoil in China and elsewhere. Crude oil in storage has reached disconcerting levels for this time of the year. And people are starting to pray for miracles.

The overall commodity complex hit new multi-year lows this week. But gold has been an exception, rising from its own dismal multi-year low at the end of July.

Shocked and appalled that the market had somehow rediscovered this dastardly will of its own, Wall Street is already clamoring for ZIRP Infinity and QE4 Infinity, a real “infinity” this time, because everyone knows that at these ludicrous valuations, the market can never stand on its own two feet again, and folks simply don’t want to give up the trillions that the Fed has so magnanimously shoveled their way.

To top it off, currency turmoil tore into the emerging markets, and a debt crisis is starting to build up on the horizon. Read… It Starts: Broad Retaliation against China in Currency War