It wouldn’t be a day ending in “y” without some funky news about what the PBOC is now doing. Today’s edition includes the unconfirmed rumors of forex deposits. Apparently the PBOC is going to require, starting October 15 (are they trying to force the bottleneck?), banks to reserve 20% of some figure which isn’t at all clear at the moment. The mainstream media is reporting “sales” as the whispered indication but that may mean netted sales or something else.

The People’s Bank of China will impose a reserve requirement on financial institutions trading in foreign-exchange forwards for clients, according to six people familiar with the matter. The change, which takes effect on Oct. 15, will mandate a deposit of 20 percent of sales to be held at zero interest for a year, said the people, who asked not to be identified because they aren’t authorized to speak on the issue.

“It’s a move to ease the reduction in foreign-exchange reserves,” said Tommy Ong, managing director for treasury and markets at DBS Bank Hong Kong Ltd. “It’s also meant to discourage speculation and ensures the yuan’s rates are reflecting genuine demand and supply. That includes cross-border yuan investment into fixed assets.”

While it is tempting, as always, to frame this as aimed against “undue” speculation, the wholesale reality of the “dollar” again rears its ugly and devastating head. To figure out exactly why, it is necessary to take a few steps back and rerun these escalating measures in the wider “dollar” context. Much of what is believed about the world of forex is taken from two positions; the first, as if “reserves” were themselves a meaningful idea and even the tabulations that are reported to various intra-national institutions like the IMF are solid rather than dynamically amorphous; second, that the current state of the global trade world is derived from lessons purportedly learned in 1997-98 – the Asian flu.

In the past few months, concerns about reserves have been expressed in an “unexpected” manner given what was taken as financial gospel even during the building “dollar” strain. The common refrain was something along the lines of the usual “central banks are better prepared” because of how they so disastrously failed before. In the case of forex, that meant some combination of floating currencies and huge “stockpiles” of “reserves.”

From Bloomberg June 2015:

Unlike the 1997-1998 Asia financial crisis governments in the region are now better prepared, having introduced free floating exchange rates and building up forex reserves. Although as the Fed taper tantrum showed, funds can still flow quickly out of Asia, punishing local currencies.

Even just last week, printed in the South China Morning Post, the idea was reworn as if it were a shield against what the author terms, “caught up in a tornado called ‘Fed policy.’”

The emerging countries in aggregate have done significantly better at macroeconomic management this time compared with the shocks of the past two decades. Many of these countries have floated their currencies, paid close attention to their current account deficits, become more fiscally responsible and have amassed a sizeable foreign exchange reserve position that together has left them better placed to deal with increased currency, bond and equity market volatility. Their banking systems are better capitalised, and a significant part of their incremental indebtedness is now denominated in local currency (rather than US dollars).

All of that is true, but I still don’t see how it adds up to whatever protective benefit is being ascribed to it all. Part of that stems, as always, from the under-appreciation (or just completely lack of awareness) of wholesale banking dynamics about the modern “dollar” under the eurodollar standard. It seems quite reasonable that with floating currencies and huge piles of particularly dollar reserves that any foreign central bank would be able to almost easily withstand “capital outflows.” But in the wholesale case, what is thought to be the primary positive countermeasure is actually a measure of vulnerability.

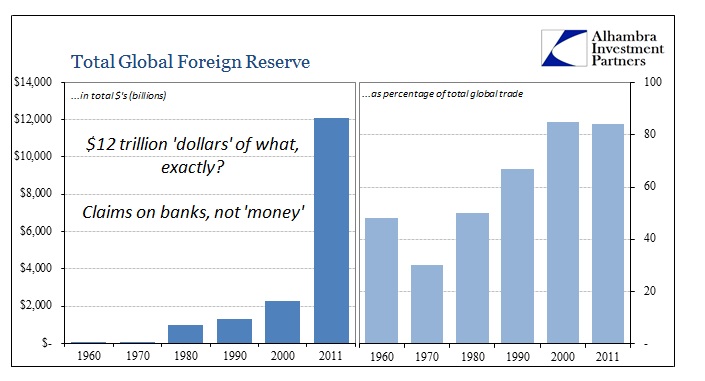

To start with, this rise in “reserves” dating back to the latter 1990’s seems entirely within the scope of this convention. “Prudent” central banks have been piling up dollar assets as a rainy day measure and getting paid to do it. The acceleration has been enormous, particularly in the 2000’s.

There figures are taken from various institutions such as the BIS and IMF (more on that below), but what is immediately clear is that there obviously wasn’t enough actual currency printed in the decade of the 2000’s to turn $2.28 trillion in reported “reserves” into $12.1 trillion. Given that there weren’t any QE’s (until the end) along the way, that cannot be explained by the conjuring of central bank balance sheets either; which means these are not piles of currency or even central bank balances but the creations of the wholesale dynamic.

That much has been the case going back to the start when actual money under Bretton Woods was the external basis. From 1970 to 1980 total “reserves” rose from just $95 billion to $1 trillion! That is the magic (most people call it inflation and aren’t so enamored with its properties even if they can’t directly observe its genesis) of credit-based reserve currencies where bank balance sheets operate as the virtual printing press. The wholesale system went into total overdrive in the late 1990’s and 2000’s, which explains the enormous buildup in “reserve” balances.

Given what we know of the global “dollar short”, then, the combination of the two isn’t a means of defense but rather, to reiterate, a mark of weakness and susceptibility; if a given central bank has a high “reserve” balance in dollars that isn’t a sign of strength but rather a decent proxy about how much of that “dollar” short the national system may be exposed to. The prime example particularly in the past few years has been Brazil. Despite its apparent huge pile of “reserves”, $368 billion at last IMF tally, it has seen its currency devastated as the eurodollar run continues reaching back all the way to 2013.

Part of Brazil’s problems relate to exactly those “reserves” in actual composition. The country’s central bank reported in March that $368 billion figure but also that $360 billion of that was in “convertible foreign currency”; and that $339 billion of that was “securities.” Under its memo portion of the IMF call sheet, Brazil notes $108.182 billion in “financial instruments denominated in foreign currency and settled by other means (e.g., in domestic currency)” which is entirely a derivative “short position.” In other words, there is a lot more than just UST’s and deposits in these so-called reserve balances.

Indonesia, another of those central bank domains that heeded of floating currencies and reserve piles, reports $108 billion in “reserves” of which $101.8 billion in “convertible foreign currencies” and of those $89.2 billion in “securities.” The central bank of Indonesia does have $12.6 billion in actual deposit balances, but only $9.6 billion with other national central banks, the IMF or the BIS. The remaining deposit balance is with unknown “banks headquartered outside reporting country.”

Further, Indonesia has built in its “reserves” $19.2 billion in foreign currency loans, of which $9.5 billion mature within one month (of the March reporting date), to go with a further $7.5 billion short position in futures and forwards with other currency denominations ($1.9 billion maturing in one month). And that’s not all, there is almost $2 billion in securities “lent and on repo” as well as $6.8 billion in swaps (no notation about where, to whom, or at what terms) that is a reported mark-to-market rather than actual notional liability. To say what Indonesia does or does not hold with regard to actual credit-based reserve flows (and its dark leverage) isn’t at all straightforward on its face, which means that central banks are doing what banks themselves do and are modeling based on risk factors and expected volatility. It isn’t any wonder that they are so often behind-the-curve even where they are assumed to have amassed this huge and impressive-sounding war chest.

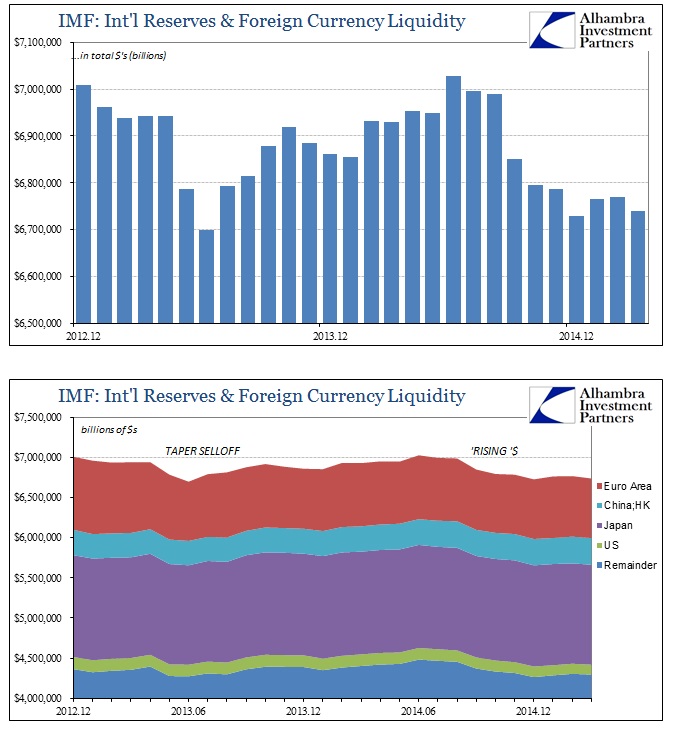

As it is despite all that, their currencies can’t hold water against the agitated wholesale “dollar.” The IMF tabulations for reserves continue to drop, though their own limitations are showing in the presentation. Despite being dedicated to building a comprehensive and global reserve picture (which is one of the primary lessons the IMF itself took from the Asian flu) there are some notable absences and gaps – such as China.

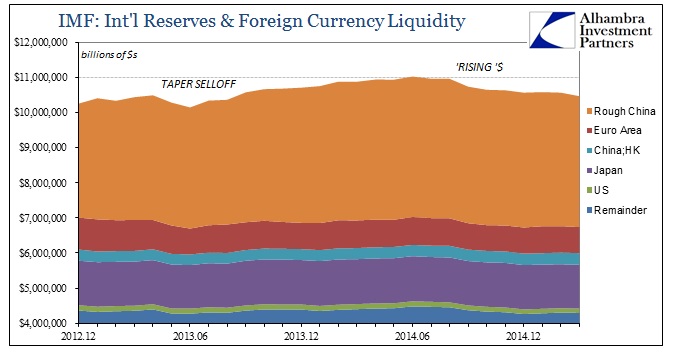

From those reported to the IMF, total reserves have fallen by about $290 billion since June of last year. The total of all reserves for the IMF’s worksheets are about $7 trillion, now just above $6.7 trillion, but that only includes China insofar as they report just the Hong Kong Special Administrative Region; the vast holdings of the PBOC and the rest of China are omitted. We can, from various sources, sketch out a rough approximation for China, with about $4 trillion in reserves (of unknown types of securities) which gets the total closer to $11 trillion and that 2011 figure from above.

Again, we have no idea what is really in that almost $4 trillion; is it like Indonesia? How many swaps or RRP’s? The call sheet for Hong Kong reports $340 billion in reserves, $326 billion in convertible currency of which $313 billion is securities. Other than the reserve deposits reported on Section I, the remaining three sections are almost all left blank (other than $39 million in currency loans, $46 million in “accounts payable” and $765 million net in repo; no more than rounding errors, all).

Clearly, the PBOC is doing something with its reserves and it isn’t just “selling” treasuries. Even the rough estimates for China’s reserve balances have declined by about $270 billion through March from a peak last June – that isn’t all UST or deposits especially as it strikes $400 billion in the latest figures before the August fireworks. Further, we know with very little doubt that it was enough wholesale strain as to essentially break the PBOC’s resolve on August 11 into an open “dollar” run that could have taken on almost any actual format; particularly given the internal liquidity dynamics of the yuan linkage to all that. If the PBOC was engaging swaps as Banco do Brasil, that is not a remedy but invited further disaster (though I should caution that Brazil’s “swaps” aren’t really that, but in similar proposition the comparison is that the central bank, through derivative intrusion, makes it all worse by incentivizing local banks to be even further “short” the “dollar” in what nets out to short-term stability at the cost of kicking the much enlarged can further down the calendar).

If there are swaps into this “reserve mobilization” in China as in so many other places it is the potential for further disaster. At some point, the PBOC swaps would mature and it would have to deliver on them. That is why swaps are a short-term, temporary bridge as it is intended that whatever immediate “dollar” problem would be over by then and that the “cost” of not rolling them over is easily born by a restored private market flow. Might that be why the PBOC chose October 15, as a second monthly rollover from swaps being issued out in the middle of August?

There is another way to look at it, and this is really the nightmare scenario and not just for China but everywhere. By requiring private firms to deposit forex (mostly dollars) in October the PBOC might be planning for the worst case. It has, by now, appreciated just how limited actual mobilization of all those “reserves” actually can be, as even doing heavy intervention so far was largely ineffective despite all the convention about having all those protective reserves in the first place – the yuan still broke and China fell into the crosshairs of open disorder. And that is the larger point and confluence, where the PBOC “reserves” may contain further disruption if they aren’t properly calibrated (and they never are; again Brazil, Indonesia and the rest) just as the rest of the world wakes up to the fact that all those reserve piles were instead of being insurance against the worst case are the very problem itself – wholesale exposure as the decay in wholesale eurodollar reaches almost predetermined amplification.

There is of course, the probability that the theoretical foundation turns out correct, that this is a short-term problem that will be weathered and corrected in short order. While it may still be possible, given that this eurodollar trajectory is eight years on and even that the most recent acute breakout is itself now well over a year old that really doesn’t seem too likely. And while the Fed may be instigative here and there, that eurodollar spiral has survived the “will they/won’t they” drama all throughout with only the expected ebbs and flows within the unrestrained disastrous trend.

As I mentioned yesterday, “I don’t think it ends until a fundamental change is made; either the economy starts living up to the promises or liquidity subtracts until prices actually reflect that it won’t.” Recent economic data all across the world is more than just the usual gloominess, which means if the latter form of my scenario on reversion comes up it is those countries with the most wholesale exposure that will be hit the worst; more so than they already have. Wholesale “reserves”, in that specific case, are the nightmare to which there is no defense.

By taking on these wholesale characteristics, central banks have turned their own “reserves” into, and a full part of, the banking storm. Floating currencies and reserve piles would be terrific if there were actually that, but they aren’t. Actual money even in a floating currency scenario is the exogenous release of pressure; wholesale reserves in a credit-based monetary system are quite instead absorbed endogenously within the wholesale decay itself as just one other element fully part of that struggle. One central bank after another is finding that out the hard way, and if everyone follows Brazil what would be left for not just liquidity but total price support?