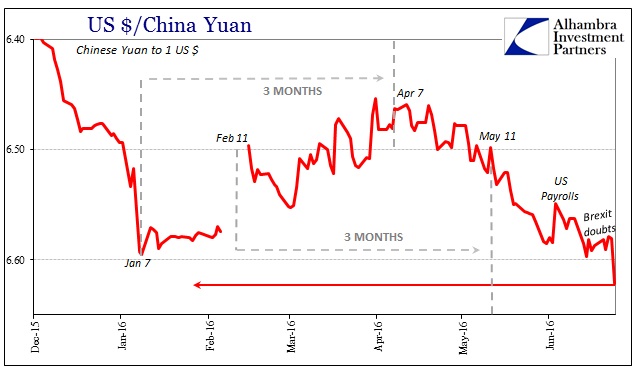

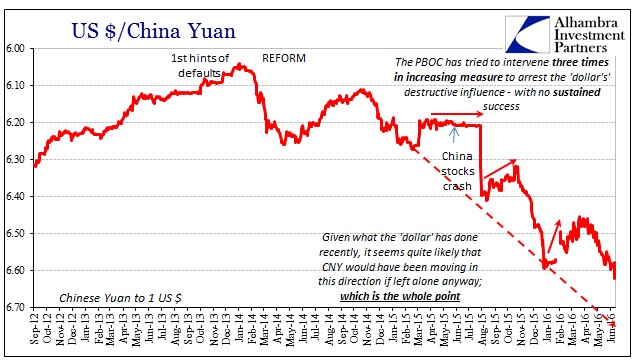

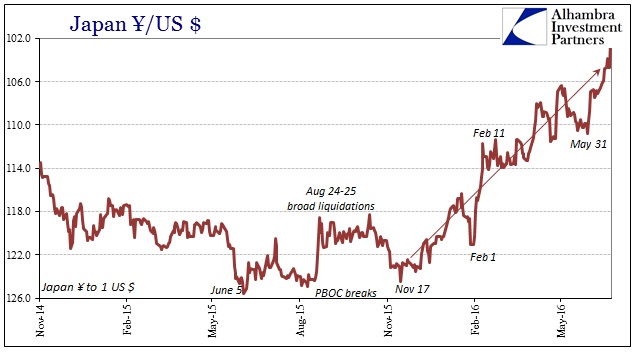

It was a nice diversion while it lasted, I suppose. From the moment of the unfortunate murder of the British MP, funding markets, in particular, had been furiously “selling dollars” to get back some of the pound that was falling as Brexit had gained momentum. Media commentary talks about it as if that were the whole topic – it never was. With the votes counted and the reality setting in, there were going to be overreactions and there certainly have been plenty. But as time progresses, the world goes back to its natural trend:

The UK’s removal from the EU was never going to change anything whichever way Britons voted. It was, again, a fun distraction and a competent scapegoat. As the alluringly optimistic “dollar selling” fades, the world can resume once more. That’s the bad news.

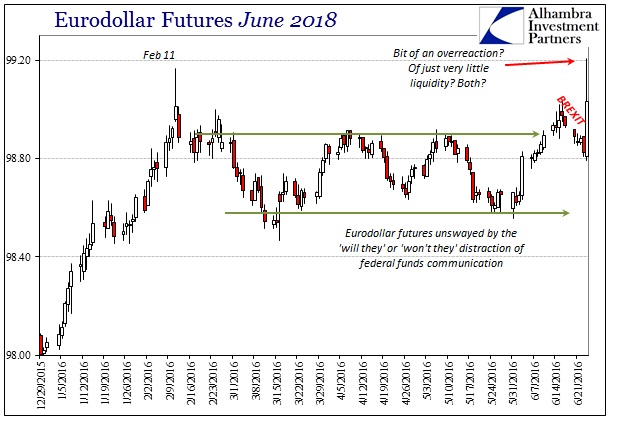

One final note: the June 2018 eurodollar futures contract somehow opened at 98.82 before exploding by nearly 40 bps to 99.20. It has since settled back somewhat to around 99.04 (as of this writing), but a 15 bps move is unusual and extreme. Brexit was 38 bps settling to still more than 20 bps. That’s overreaction for sure, but liquidity is atrocious all over.