The nominal changes in average pay in the past few months, and really going back to October 2012, are not really consistent with the orthodox idea of a reduction in “slack” in the labor market. By that I mean wage growth has been lagging at the same time the mainstream payroll indication has moved upward. It is certainly possible for that to occur with other factors involved, but none of them would agree with the “slack” interpretation.

Nominal wage growth has underperformed the “recovery” trend, such that it is, for some time – precisely when the Establishment Survey says labor growth picked up.

Further, the aggregate indication of total hours worked has also seen a remarkable deceleration. That shows up as the average workweek stopped expanding all way back in early 2012.

Undoubtedly the inability of hours to return to pre-2008 levels of activity relates to the part-time trend during this recovery (which would include the rather large drop in full-time jobs in June). That again raises the quality vs. quantity issue that continues to demonstrate that something is rather dangerously amiss despite all assurances otherwise (for what it’s worth given that none of those assurances have actually panned out to this point).

Whatever the relation to recent months and the Establishment Survey’s “surge” (which times to the birth/death cycle more than anything), in terms of the overall economy there is nothing to suggest an actual broad-based acceleration. It may, however, simply be extrapolating the asset inflation-induced bartender economy. Jobs in the highest paying tiers were destroyed and are being replaced, seemingly on a numerical basis anyway if you actually find validity in the statistics, with low-level service jobs. Those with direct experience to asset inflation, concentrated as its effects are, can “afford” to expand their activity which is why jobs appear at the lowest ends of the service sector. But that creates little broad-based wealth, and the idea of spending as a primary driver of economic expansion (aggregate demand theory) is conspicuously absent. There is no trickle of second order economic derivation.

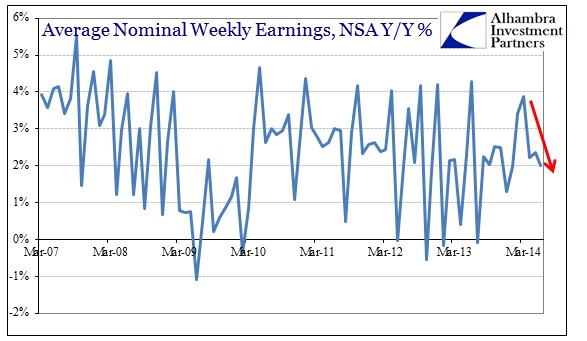

That becomes even more pertinent as the cost of living (not the official inflation rate) continues to batter consumers. Despite the purportedly large gain in June payrolls, average weekly earnings only gained 2% Y/Y – which likely means lower actual purchasing power. Since there appears little enticement to engage those currently outside the labor force (and, apparently, new potential entrants too), on a per capita basis the economy continues to look very sickly.

Inflation does nothing but continue negative redistribution, including the destruction of “good” jobs to be replaced by those far less desirable. And the orthodoxy expects a hearty “thank you” for it.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@alhambrapartners.com