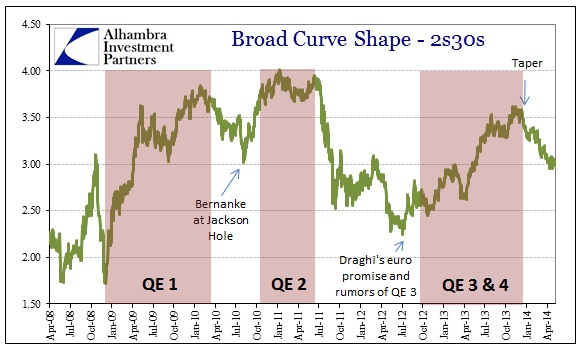

By now the bond market is really starting to annoy all the “right” people. The bear flattening that has taken place since operational taper commenced is a direct contradiction to those that implore dismissal of recent GDP (after pleading quite the opposite during the inventory build last year). Mainstream, orthodox economists have settled that Q1 is an aberration, a speed bump on the road to systemic riches – the bond market is far from assured.

The indications of that split have been evident for some time, in what I called “confused stasis.” I still think that term applies, but it wasn’t ever going to remain as such forever. Now that flattening has broken into open buying, the economists’ best hope for their narrative is short covering; as in the 10-year’s breakout lower is being driven more by short covering technicals than repositioning. While I do believe that momentum is pressured by exactly that imbalance in trade, the curve shape argues for bearishness in addition, not optimism set against.

I believe it is useful to put together a narrative over the history of the past year or so. Beginning with the first utterances of taper, the Fed and then-Chairman Bernanke (for various reasons) saw a clear downside to perpetual, even heavy, QE intrusion. I think that counted housing prices as well as MBS and even treasury repo; maybe even a small consideration for the PE expansion in at least some stock sectors. To try to talk markets down, the policy chatter attempted a “soft landing” through moral suasion. The bond market took high notice and nearly crashed right off.

The FOMC effort, however, was not simply about QE, it included the rational expectations theory component. Paired with every expression of taper was stapled a choreographed highlight of the Establishment Survey and especially the official unemployment rate. In other words, tapering QE, for the public, was not about financial risks as much as successfully achieving that mythical recovery. That set the pace of the bond selloff and dollar tightening. Mainstream economists jumped on board enthusiastically.

While the bond market sold off, it was never fully convinced of the econ side. You can understand the selloff, then, in the context of being over-positioned and aggressive on the previous regime of “unlimited” QE. In other words, bonds and dollar markets were simply unprepared for this new policy narrative and had to adjust, violently as it turned out (due in large part to the changing character of liquidity and dollar markets).

The changing in expectations (especially volatility) for the funding side drove the gulf in treasury selling and dollar tightening. Where the curve steepened almost everywhere, including eurodollars, inflation expectations entered the “confused stasis.” In fact, breakevens have remained in that range throughout regardless of curve shape distortions and movements.

Even the recent jump in the 5-year breakeven remains within this range, and 50bps below where it was at the end of 2012 (when QE3 was still promising).

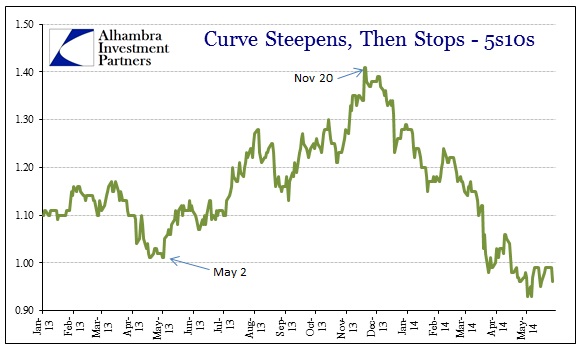

As the overall UST curve ran steeper during the selloff/tightening period, the Fed seems to have had at least a minor fit of remorse. It was no doubt aware of the collapse in the mortgage pipeline that was evident almost from the start of all this, especially by September and October when the major banks began to layoff thousands of employees in their mortgage departments. Since QE3 takes the operational form of production coupons in the TBA market, pipeline collapse would have been front and center for the Open Market Desk. I don’t think there is much doubt that the obvious adjustment in POMO right at November 20 was intended in that direction.

Rescuing the 10-year meant upsetting the steepening trend. While the overall curve continued to sell, interest rates ran slightly higher from there, the shape had begun to move in the opposite direction. It started in the belly.

It is certainly possible that the early flattening in the 5s10s sector had no influence on what came next, but I have to believe it was at least a factor. Once taper became a reality in December, the broader curve began to behave exactly as it had in other periods where the Fed disengaged.

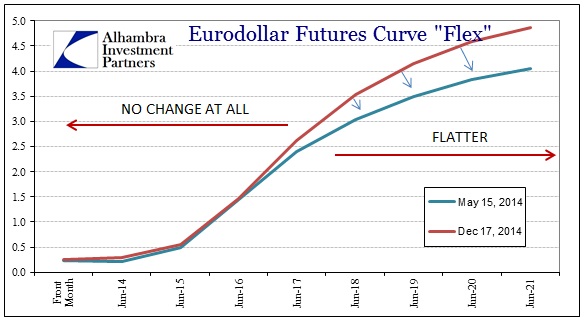

At exactly the same moment, the economy conspicuously detached from the acceleration narrative (retail sales’ worst Christmas since 2009, inventories, even GDP). This dichotomy was perhaps most clear in the behavior of the eurodollar curve. The shorter end, the money end, held almost blatantly steady to the policy trajectory (taper) while the longer term funding positioning went flat like the UST curve. That signaled the dollar market was expecting both a benign to tightening policy mix at the same time as lower growth in the future.

Further into 2014, with more muddied signals from Chairman Yellen about what really is a sea change in expectations and theory, the bearishness in bonds have only been further encouraged. Where economists have remained on the Bernanke-driven trajectory of less monetarism because of more growth, credit and money seems to have picked up both less monetarism and less growth.

That course seems to have again altered more recently. Suddenly, in my opinion, funding markets have begun to factor a lower rate trajectory even inside the policy window.

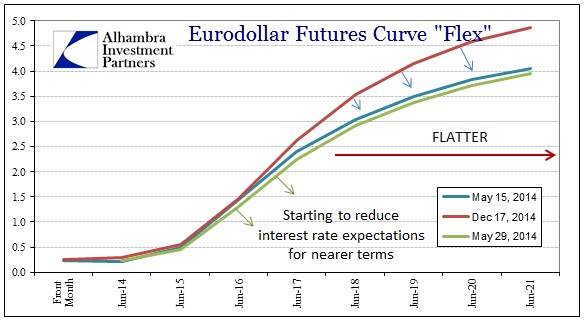

While the slight drop into the middle of 2015 looks to be indistinguishable from simple calendar roll, into 2016 and 2017 the curve is clearly moving lower, even if slightly. That would suggest, and only mildly at this point, some nervousness about economic weakness not just down the road in the form of lower potential, but closer in. That would also be consistent with what I think is being done in the form of optimal control, as in taper is also about the Fed conserving “dry powder” in case the economy falters not in 2018, but in 2015 (or even closer!).

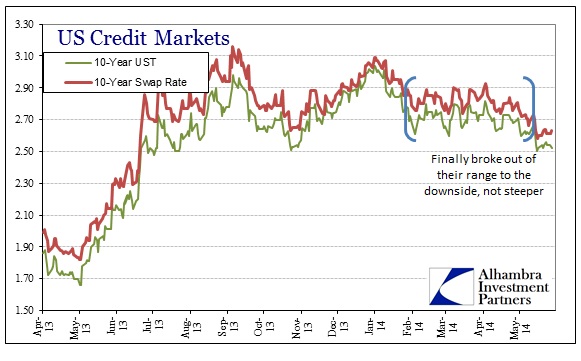

The speed at which the curve flattened certainly echoes prior episodes of more immediate weakness in both the real economy and financial economy. I think that is also consistent with the 10-year finally breaking down out of its “stasis” not to the upside (which I wrongly expected to happen first, before falling back lower) but immediately lower and flatter.

That sets up another “titanic” struggle between economists and money markets – academic models against those with actual money positions. The economist side sees taper as a signal that the economy is going to take off (as intended under the Bernanke scenario of influencing expectations), whereas the credit and dollar markets may be coming around to taper as optimal control, preserving policy margins ahead of economic turbulence.

We know which side stocks are betting on.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@alhambrapartners.com