By Administrator at The Burning Platform

On October 2 the BLS reported absolutely atrocious employment data, with virtually no job growth other than the phantom jobs added by the fantastically wrong Birth/Death adjustment for all those new businesses springing up around the country. The MSM couldn’t even spin it in a positive manner, as the previous two months of lies were adjusted significantly downward. What a shocker. At the beginning of that day the Dow stood at 16,250 and had been in a downward trend for a couple months as the global economy has been clearly weakening. The immediate rational reaction to the horrible news was a 250 point plunge down to the 16,000 level. But by the end of the day the market had finished up over 200 points, as this terrible news was immediately interpreted as good news for the market, because the Federal Reserve will never ever increase interest rates again.

Over the next three weeks, the economic data has continued to deteriorate, corporate earnings have been crashing, and both Europe and China are experiencing continuing and deepening economic declines. The big swinging dicks on Wall Street have programmed their HFT computers to buy, buy, buy. The worse the data, the bigger the gains. The market has soared by 1,600 points since the low on October 2. A 10% surge based upon lousy economic info, as the economy is either in recession or headed into recession, is irrational, ridiculous, and warped, just like our financial system. This is what happens when crony capitalism takes root like a foul weed and is bankrolled by a central bank that cares only for Wall Street, while throwing Main Street under the bus.

The employment situation continues to deteriorate on a daily basis as Challenger, Grey & Christmas has reported layoff announcements by major corporations in 2015 that already exceed the total announcements in 2014. This is the reality versus the BLS 5.1% unemployment rate fantasy. Retail sales, which make up two thirds of the economy, are putrid and confirm the dreadful employment market. Corporate profits among S&P 500 companies have fallen for two straight quarters and are picking up steam in a negative direction, as accounting shenanigans cannot disguise falling revenue forever. Earnings per share estimates for future quarters fall on a daily basis.

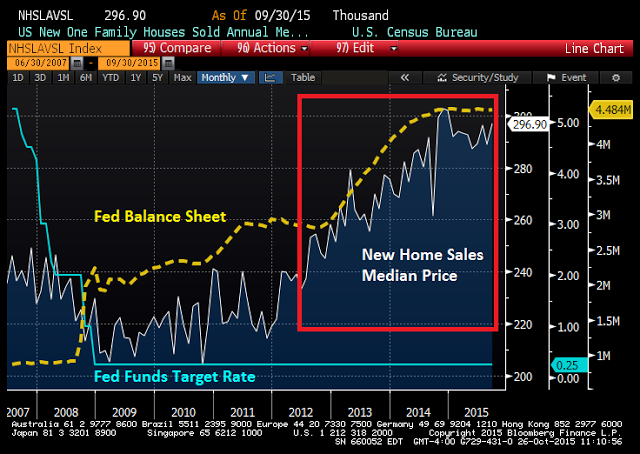

Every manufacturing and services survey flash recession warning. Despite propaganda from the NAR, government and the MSM, the housing market is dead in the water. Major home builders continue to report declining orders as new home sales are plummeting and existing home sales, without NAR adjustments, show a negative trend. But prices continue to rise as that has been the Fed’s purpose all along – to repair Wall Street bank balance sheets at any cost. Sacrificing the well being of tens of millions of senior citizens and millennials has been well worth it for Ben ($300,000 per Wall Street bank speaking engagement) and Janet, as the million dollar banker bonuses have done wonders for high end NYC penthouses and beachfront estates in the Hamptons.

The awful U.S. economic data pales in comparison to the absolute implosion occurring in China, as they desperately falsify economic growth data, threaten to prosecute stock sellers, censor truth tellers, bail out failing government entities, and manipulate their currency, to fend off impending disaster. Europe wallows in an ongoing depression as youth unemployment in most EU countries ranges between 20% and 50%. A bankrupt union of socialist states, dependent solely on central bankers issuing more debt to pay off old debt, have signed their own death warrant by allowing themselves to be overrun by hordes of Muslim refugees.

As John Hussman explains, the global economic situation has gotten so bad, central bankers have again come to the rescue by promising to prop stock markets up like they’ve been doing for the last six years.

The market rebound of recent weeks has essentially been grounded in exuberance that the global economy is deteriorating so quickly that central banks will insist on accelerating their monetary interventions. While both corporate earnings and revenues are now in retreat, we also see enthusiasm about the remaining economic activity being captured by a handful of winner-take-all companies. Those two dynamics largely summarize the tone of the market here.

U.S. economic data unequivocally indicates a recessionary environment on par with 2001 and 2008. Those periods did wonders for the wealth of stock investors, if you recall.

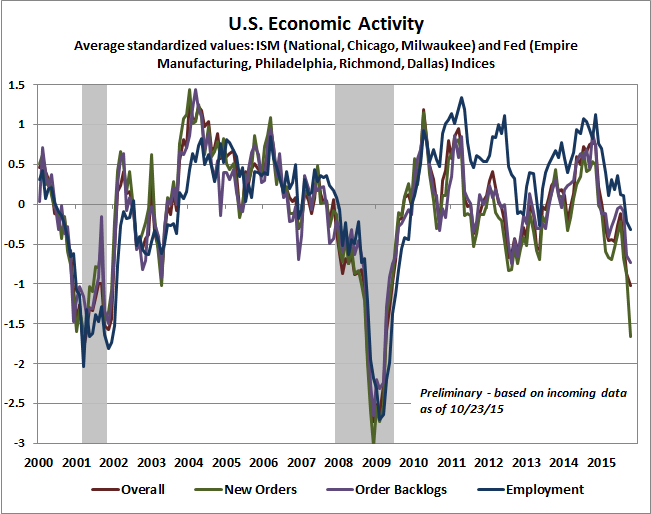

The following chart updates our standard economic review of regional and national Fed and purchasing managers’ surveys. The October Philadelphia Fed report was particularly weak on the new orders front, which is complicated by the fact that it’s also one of the more reliable surveys as an indication of broad economic activity. The chart below reflects available data through Friday.

The Pavlovian dog response of Wall Street traders to any hint of monetary easing or continued ease is as predictable as a monthly billion dollar fine being paid by an upstanding Wall Street financial institution. Obscene valuations, plunging corporate profits, and a low volume extremely narrow advance are not the ingredients of a new bull market. They are the ingredients of a dead cat bounce.

The underlying thesis, of course, is that monetary easing — regardless of its fruitless effects on the real economy — is a reliable signal that the financial markets are open for speculation. Valuations are the central driver of long-term investment returns, while market returns over shorter portions of the market cycle are primarily driven by the preference of investors to seek or avoid risk. At present, valuations remain obscene and market internals remain unfavorable. Credit spreads remain wide, and despite last week’s market advance, the percentage of individual stocks above their own respective 200-day moving average hardly budged, increasing only from 37% to just over 38%. Our broader measures of market internals remain unfavorable here as well.

The pessimism overriding the markets from August through October was warranted, based on reality, facts and historically accurate valuation methods. The 1,600 point reversal has been based solely on hope and faith in central bankers who have failed miserably in spurring economic recovery with their monetary machinations. With valuations at nose bleed levels, rising P/E ratios due to declining earnings, record margin debt, and overly optimistic bulls, years of gains are poised to evaporate.

It’s essential to keep in mind that the equity market moves in cycles between extreme optimism, rich valuations, and poor prospective returns at market peaks, to extreme pessimism, favorable valuations, and high prospective returns at market lows. Even a run-of-the-mill bear market decline typically wipes out more than half the gain of the preceding bull market. Based on our current methods of classifying market return/risk profiles, the most severe market losses across history are captured by observable conditions that have emerged only about 9% of the time — a subset that that includes the present.

The coming violent devastating crash, which will not be avoided through further central banker intervention, has been perpetuated, financed and encouraged by the Federal Reserve. They have trained the Wall Street Pavlovian dogs to salivate at the ringing of the QE/ZIRP bell. They’ve managed to delay the day of reckoning, but will not permanently fend off reality. Booms fueled by easy money, ALWAYS go bust.

The dogmatists running global central banks have encouraged investors to believe that volatility and downside risk have been, and can sustainably be, removed from the financial markets. No — by encouraging the illusion that normal cyclical fluctuations have been eliminated from the dynamics of the markets and the economy, the result has been far more risk taking, far heavier issuance of low-quality and covenant-lite debt, far more yield-seeking misallocation of capital, and far more extreme equity valuation in this cycle than would have been possible otherwise. The consequence will be far more violent market behavior over the completion of the cycle than investors would have faced otherwise.

We’ve seen it all before. Two epic stock market collapses within the last fifteen years have been long forgotten by the Wall Street lemmings who ignore the fact the Fed eased during both market collapses. The fact the Fed has absolutely no ability to ease further as the economy deteriorates doesn’t seem to bother the perpetual bulls. Their level of historical ignorance is only matched by their hubris and arrogance.

The declines and recoveries we’ve seen over the past year are nothing that we did not also see during the extended 2000 and 2007 top formations. Once persistently overvalued, overbought, overbullish conditions were followed by deteriorating earnings growth and a breakdown in market internals, the goal wasn’t to speculate on rebounds, but only to limit the amount of frustration one had to endure during the top formation — in anticipation of the more severe market losses that followed.

Denial and putting trust in Ivy League educated academics who are terminally wrong in their predictions, policies, and solutions is not a logical plan. It’s a recipe for disaster and another 50% haircut.

Based on the most historically reliable valuation measures, the S&P 500 would have to lose literally half of its value for prospective returns to rise to that level. A 50% market loss isn’t a worst-case scenario. Given current valuations, it’s the standard, run-of-the-mill outcome that investors should expect over the completion of this cycle.

As John Hussman points out, we are about to be transported back to the wonderful days of 1929. Time is growing short as the grains of sand in the hourglass run out.

Investors are now facing the second most extreme episode of equity market overvaluation in U.S. history (current valuations on similar measures already exceed those of 1929). The belief that zero interest rates offer no alternative but to accept risk in stocks is valid only if one believes that stocks cannot experience profoundly negative returns. We know precisely how similar valuation extremes have worked out for investors over the completion of the market cycle, and those outcomes have never been deferred indefinitely. The only question at present is how many grains are left in the hourglass.

Source: The Worse Things Get For You, The Better They Get For Wall Street – The Burning Platform