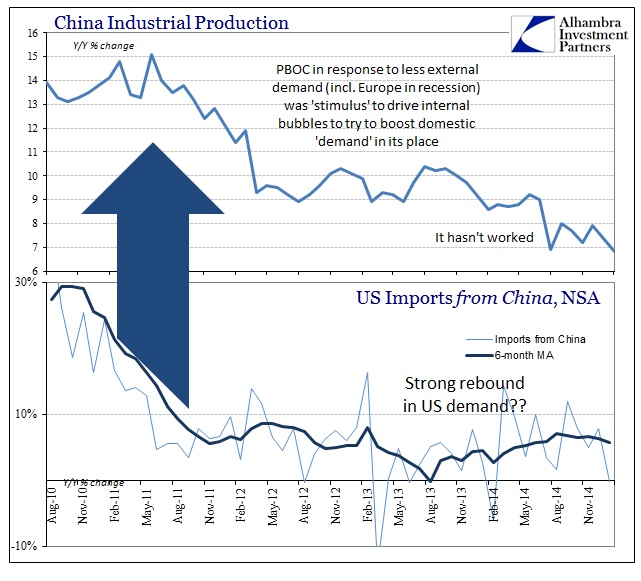

China remains an export economy no matter how hard they try to convince the world they are moving otherwise. The idea of creating internal “demand” as a means to extricate marginal changes from everybody else is undoubtedly a good idea, even a noble one, but the reality of China as it exists top-down isn’t conducive for such a transformation. Further, that just isn’t realistic under the global conditions that have persisted since the Great Recession was declared over.

In that respect, there isn’t much to separate what is occurring now from the Great Recession itself. Certainly there exist positive numbers in economic accounts where deeply negative numbers predominated during the “event”, but the major factors that inaugurated the dislocation remain especially unsolved and more often than not misunderstood. China’s predicament falls into that category.

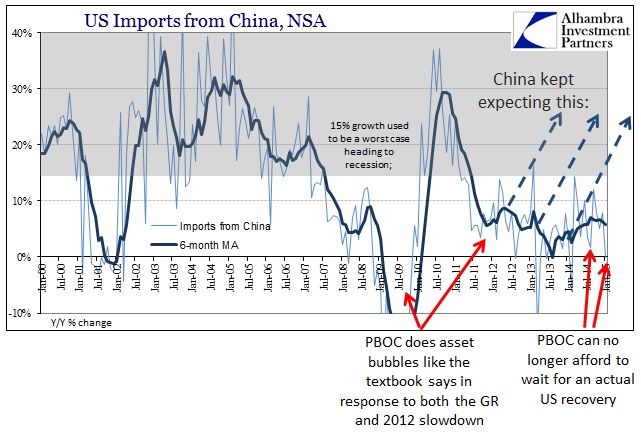

The idea of reform, to reiterate, is as much a rebuke against orthodox monetary economics as it is of China. The Chinese did in 2009 as the textbook says, and embarked upon tremendous “stimulus”, both monetary and fiscal, which “aggregate demand” “should” have led to rebirth. Even if it didn’t, the re-igniting of the global economy from all the other central banks following the same textbook should have resolved any lingering deficiency. “Extend and pretend” is as much about time as anything, and even massive imbalances can be covered and eventually removed by robust and sustained economic advance.

Instead, monetarism hasn’t worked anywhere, leaving little sustainable “aggregate demand” to sustain all the massive financial imbalances created for it. That is the most poignant reckoning out of the PBOC’s reform ideas, that in order to gain even the smallest fit of “demand”, even artificially, it takes an inordinately large asset bubble. Such massive inefficiency is highly problematic in so many ways, but not the least of which under these conditions where bubbles exist almost everywhere without the requisite recovery in economic function and activity.

Therefore the entire point of “reform” in China is an assault on the senses of mainstream commentary as well as theory. Janet Yellen says that the US is booming, even if the data doesn’t agree, so who is the PBOC to proclaim otherwise? Further, orthodox economists tell us over and over that there are no asset bubbles and that monetarism is not just most effective it is the only option – we know this because a credentialed economist is on TV almost all the time and is quoted in almost every mainstream news item in order to reinforce the narrative.

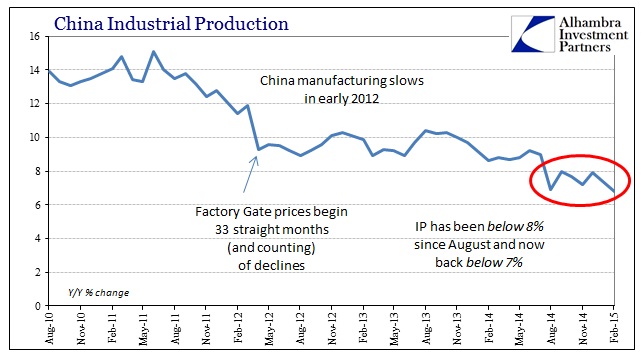

Reality has a way of mugging even the most hardened ideological positions, in particular where ambiguity has been totally drained. The past six months’ data on China, PMI’s aside of course, has left little optimism about anything except unfounded hope for monetary softening. The economic figures were the worst since the Great Recession, and even worse than that drastic decline in a lot of cases, by far. Retail sales were the lowest since 2001, as was “fixed asset investment”, an important indication of Chinese economic fervor. Industrial production fell to 6.8% growth, well below the 7.8% “analysts” were expecting, to yet another new “cycle” low.

It is clear now that this is not a “transitory” problem, so the implications for much more than China are becoming undeniable. Even Reuters has finally conceded to connecting the dots:

The Chinese economy has had a rough ride in the last 15 months as a property downturn compounded slackening growth in foreign and domestic demand and persistent industrial overcapacity. A widening corruption crackdown also has weighed on everything from investment to retail sales. [emphasis added]

It’s surely not a winning endorsement of “global growth” which would at least include the US “miracle.” Further, the same article seems to have finally appreciated what the PBOC is undertaking in that context.

Policymakers have cut interest rates twice since November, and in early February reduced the amount of cash that banks must hold as reserves (RRR), freeing up fresh liquidity to flow into the economy to offset rising outflows of capital.

But because those adjustments so far have been largely defensive in nature, economists say, they haven’t translated into lower real interest rates or increased investment. Chinese companies are cautious about expanding in the face of weak business prospects, and bankers are wary of a spike in non-performing loans.

That is the entire point of “reform”, as the PBOC has no interest in maintaining bubble imbalances anymore. Their entire focus is “defensive” because they have little choice under these conditions. That means accepting the economy as it is on its own, as bad as that may get, in order to at least attempt to restore financial sanity and even a little discipline. These are all anathema to orthodox monetarism, which is why most economists simply cannot grasp the point of the endeavor. As if to leave no doubt about that last point, Reuters quotes a credentialed economist who is clearly confined by the bubble of such narrow theory.

“Activity data surprised the market on the downside by a large margin, suggesting that China’s first quarter GDP growth could likely fall to below 7 percent,” ANZ economist Li-Gang Liu said in a research note.

“In our view, the extremely weak data at the beginning of the year suggest that China needs to engage in more aggressive policy easing, and we see that a reserve requirement ratio (RRR) cut will be imminent,” he said, adding that stimulus measures rolled out since last year seem to have had limited effect.

Good luck with that; the PBOC has already proven it is accepting of this reductive growth trend, as is the government and its continually lowered GDP “target.” “Aggressive policy easing” will be left for those economies where monetary awakening remains, as ever, nothing but a mathematical inequality.