By Tyler Durden at ZeroHedge

If you’re the type who likes black swans this has been the month for you.

On the political front, Portugal’s Socialists, led by Antonio Costa, formed an alliance with the Left Bloc and the Communists on the way to overthrowing the Passos Coelho government and presaging a repudiation of Berlin’s brand of fiscal rectitude. This throws the country’s austerity program into doubt and sets up not only a confrontation with the troika, but also the potential loss of access to ECB QE should a deteriorating fiscal situation prompt a DBRS downgrade.

In Spain, Catalonia is in the midst of a secession bid which, depending on Catalan political infighting and how far Rajoy wants to push things ahead of national elections set for next month, could see a fifth of Spain’s GDP separate, causing Spanish debt-to-GDP to jump by some 25%.

As far as geopolitics goes, ISIS Sinai downed a Russian passenger plane killing all 224 people on board and then, not even two weeks later, ISIS proper waged war in the streets of Paris killing 130 people. As if those two bombshells weren’t enough, Turkey decided to shoot down a Russian fighter jet this morning.

Finally, 12 month forwards for the Saudi riyal seem to indicate that the market believes the three decade-old dollar peg is about to fall under pressure from slumping crude and falling FX reserves. BofAML calls the possibility of a Saudi depeg the “number one black swan event for the global oil market in 2016.”

And those are just the black swans that have landed in the last 30 days.

In its latest quarterly Global Economic Outlook, SocGen takes a look at five political and economic black swans that could touch down in 2016 and also warns that “high levels of public sector debt, already overburdened monetary policy, still high debt stocks and on-going balance sheet clean ups in a number of economies leave the global economy will a low level of ammunition to deal with new shocks.”

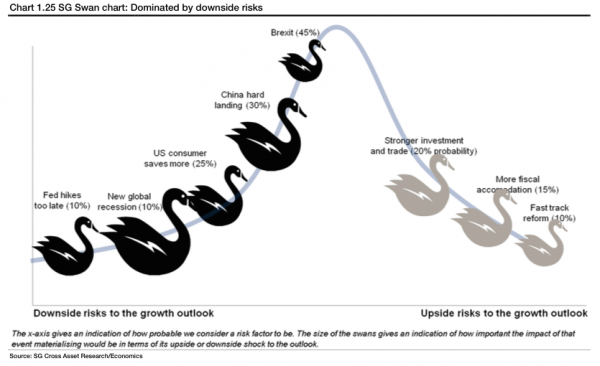

Here’s the latest SG “swan chart” which is “dominated by downside risks”:

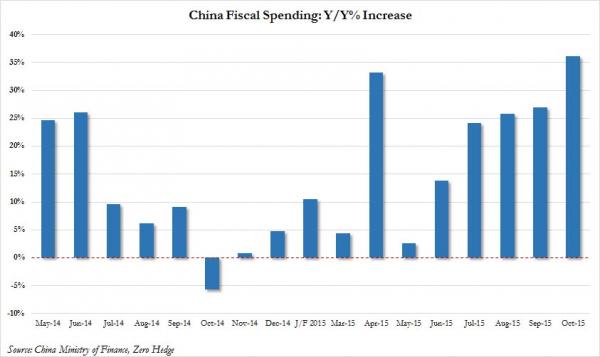

As we and a bevy of others have pointed out, QE is bumping up against the law of diminishing returns and it’s no longer clear that doubling and tripling down on monetization will do anything at all to boost aggregate demand, juice global trade, or raise inflation expectations (but what it surely will do is continue to inflate asset bubbles). In this environment, fiscal stimulus may be the only “solution.” As SocGen puts it, “in the event of a major new significant shock, our baseline scenario remains that both the US and Europe would opt first for further monetary policy stimulus. Later on, however, as this proves inefficient, we would expect fiscal stimulus to be considered.” China, of course, has already gone this route, boosting fiscal spending by 36% in Ocotber as the country’s credit impulse disappeared despite six rate cuts in less than a year.

If the Willem Buiters of the world have their way, governments will simply print debt for the sole purpose of providing central banks with something to monetize which means that in the final analysis, we could end up in the absolutely absurd perdicament of printing one liability (bonds) only to turn around and buy them from ourselves with another liability that we also print (fiat money).

In any event, below is SocGen’s rundown of the swans shown in the graphic.

* * *

From SocGen

Brexit at a probability of 45%, remains our highest probability risk. At this time, a date has yet to be set for the referendum but 3Q16 seems a likely timing, based on the idea that Prime Minister Cameron will want to hold the referendum within a reasonable timeframe on concluding an agreement with his EU partners (which could come as early as the December 2015 Summit, but more likely in March 2016).

China hard landing remains a significant risk at 30%. Medium-term, we set an even higher probability of 40% on a lost decade scenario. As opposed to a hard landing, however, such a risk scenario would manifest itself only gradually. The most likely trigger for a China hard- landing is policy error with miscalculation of how much financial risk management or structural reform the system can absorb. We identify three main triggers. In practice, a combination thereof seems the most likely cause of such a risk scenario.

- Credit crunch: An intensification of capital outflows, a growing number of non-performing loans and an insufficient response from the PBoC could result in a credit crunch. Such risks could be further exacerbated by pressure coming from Chinese corporations’ foreign exchange denominated debt and overall high level of leverage.

- Dry-up in housing demand: Should a new housing shock emerge, triggering a buyers strike, then real estate developers (also burdened with foreign currency loans) could suffer renewed stress, triggering a significant scaling back of investment.

- Capacity overhang: The still-large excess capacity in the manufacturing sector would be further exacerbated in such a scenario, weighing on corporate margins and profits. The risk is to see bankruptcies and unemployment increase in such a bleak scenario.

China hard landing and/or a renewed EM crisis are both potential triggers for a shock that could trigger global recession (10% probability).

Consumers hold the key to recovery in the advanced economies. We place a 25% probability on the risk that consumers in the advanced economies save more of the gains in real disposable income than we expect.

* * *

As for the risk that the “Fed hikes to late”, we encourage you to review “The Fed Has Made A “Policy Mistake” And The Inevtiable Result Will Be A Recession“, wherein we review BNP’s contention that the FOMC has missed its window to hike and has thereby set the US up for a recession once unemployment (which will likely undershoot) invariably snaps back.

So as you think about 2016, you can add China hard landing (of course that’s already happened, but we suppose it could always get harder-er-er), Brexit, a global recession, and lackluster consumer spending to your black swan list which should already include World War III.

Source: Presenting SoGen’s 5 Black Swans for 2016 – ZeroHedge