If payrolls were indeed expanding at a robust clip, then we should be able to look forward to a Christmas retail season more like pre-crisis than anything of the past few years (especially last year). Of course, most initial indications of expectations for spending actually seemed favorable to such an outcome, which may not have been surprising either way since initial indications are always set toward optimism.

Even in Gallup’s October results for Christmas seemed to be finally relenting to the “narrative” despite obvious resistance in the Daily Spending polls. There has been no growth in the Daily Spending going back to early 2013 and the after-effects of the 2012 slowdown. So such Christmas optimism seemed to generate retailer optimism that the shackles of the slowdown had indeed been cast off by the jobs market.

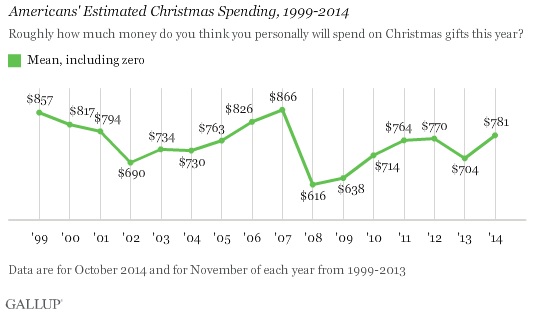

October’s estimate for the 2014 season made 2013 look like the anomaly economists have been talking about. At $781, that would be significantly better than last year’s horrible result, and even besting 2011 and 2012. As such, there was much toward straight extrapolation to the long-lost recovery finally appearing, though Gallup’s analysts might have been better served paying close attention to their own caveats:

If Americans’ Christmas spending intentions hold at the current level into November — which hasn’t always been the case — Gallup’s model suggests that 2014 holiday spending could grow by 3.8% or better over last year’s level. That is above the average 2.8% increase in holiday GAFO sales since 2000. It is also similar to the 4.1% 2014 holiday spending growth estimate issued by the National Retail Federation earlier this month.

U.S. consumers remain less extravagant in their Christmas shopping intentions than they were immediately prior to the recession, when expecting to spend $800 or more on average on gifts was the norm. But they are approaching that level today. If consumers’ higher estimates persist into November, this points to a strong holiday shopping season. However, it is worth noting that the current estimate is nearly identical to what Gallup found in October 2013, and that estimate fell significantly in November, accurately foretelling that last year’s increase in consumer spending would be rather anemic. [emphasis added]

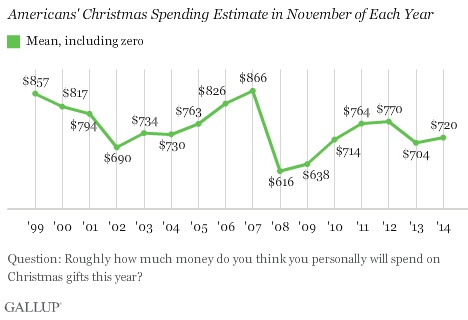

The current release from Gallup shows exactly that, another collapse in spending plans, this year from $781 all the way down to just $720; an 8% drop. That wasn’t all that much better than 2013, which saw an October/November drop from $786 down to that $704.

The $61 decline in Americans’ forecasted spending over the past month is similar to the $82 decline that occurred last year, and might be seen as something of a “cold feet” syndrome.

So the 2012 slowdown seems, after all, to be stubbornly intact. The cold water of Gallup’s results is actually already working its way through the retail industry as estimates for the coming quarter (as well as the just-concluded quarter) are not very re-assuring (and more than a few are downright pessimistic). This was from Thomson Reuters on November 12:

To date, we have received negative guidance for Q3 from 38 retailers and only six positive. In addition, retailers that already reported Q3 results are warning us about Q4 — to date we have received 17 negative guidance and only four positive.

Of 95 restaurants and retailers that had reported results by then, 44% of them missed on revenue (and a third missed on earnings).

Looking at earnings, companies are already warning us not to expect too much from them in the fourth quarter. In our retail universe, there have been 21 negative EPS pre-announcements for Q4 2014 compared to two in-line and four positive EPS pre-announcements.

The reason for the continued weakness, nothing other than weather this time too warm:

Warm temperatures and pretty fall colors in October may have drawn people outdoors but didn’t push them towards the shopping malls. Traffic slowed down and the nice weather actually worked against sales of fall merchandise since consumers didn’t feel an immediate need for sweaters and coats.

Given the abundance of cautionary data so far, I would expect Q4 sales to be consistent with everything we have seen during 2014’s heavily narrated “rebound.” In other words, expect major downward revisions at the “worst” possible time. That would suggest that if it “snows at all” another possible “surprise” hit to GDP and all the other mainstream numbers (except the Establishment Survey that only moves conspicuously in a straight line).

Even Gallup’s Daily Spending poll suggests as much, as the level of spending remains stuck, as mentioned above, for what is nearing 2 years without nominal increases. Factoring in price changes, the pace of consumption is falling further behind; not even growing at a steady pace.

And Gallup’s Daily tracking seems to suggest why Q3 has been so underwhelming in the retailer industry, completely setting aside the dubious yet still-used weather catch-all. This actually matches quite closely the data from overall retail sales that also peaked (far short of an actual rebound) around June.

Since this is the second year to repeat this pattern, I think we can make a fairly reasonable judgment about what is taking place. The constant talk about the recovery and purported strength in the jobs market as well as the bombardment of the “narrative” from the credentialed economic elite produces actual optimism (especially in tandem with record stock prices), especially as it is surrounding (for two years too) the latest end of QE.

But as with anything in the real world, you can’t take optimism to the bank and expect much beyond bewilderment. In short, optimism isn’t enough but to generate some ultimately foolish behavior that cannot possibly gain follow-through. No matter how it is spun, which way the weather blows, there is no income growth to sustain any of that sunshine. Orthodox theory on such “pump priming” is useless, as it is true wealth (and thus earned income as the primary “byproduct”) that directs true economic advancement rather than these artificial and unsatisfying “bursts” and “rebounds” that fail almost as quickly as they appear.

Instead, that optimism is cast directly against the sinking tide of the post-2012 slowdown that is not an anomaly but a global trend that does exist even inside the US. The fact that Brazil and China are in such desperate positions is not independent of a US recovery, but very much related, as shown by this persistent and persisting drag of consumption, to faltering US growth. That is unfortunately sharpened by price changes in 2014 which are more severe than both 2013 and what is being measured by official metrics. When revenue is expanding solely on price changes (or more dependent on prices), volume is thus axiomatically shrinking. To some that looks like recovery, but in the real global economy that is growing trouble.