If there seems to be more safe haven demand of late, the increasing odds of British exit from the EU is being blamed. According to Yahoo!Finance, Goldman Sachs sees “kinks” in the option structure, an agglomeration of hedging demand that points to maturities around the UK referendum. The absence of any heavy hedging this week suggests that markets have no concerns about FOMC policy communications, instead looking ahead to any predictable events that might trigger unusual selling.

But this relative calm doesn’t just have to do with this week’s Fed event. Implied volatility for options that expire after the Federal Reserve’s July meeting are subdued compared to those that encompass the immediate aftermath of the U.K.’s referendum. Even the U.S. election in November isn’t inspiring as much fear as a possible Brexit — yet…

While the last few months have been relatively tame in the market, Goldman doesn’t see this continuing. “Even if the Fed turns more dovish, soft fundamental data and uncertainty surrounding ‘Brexit’ seem to be capturing the market’s attention.”

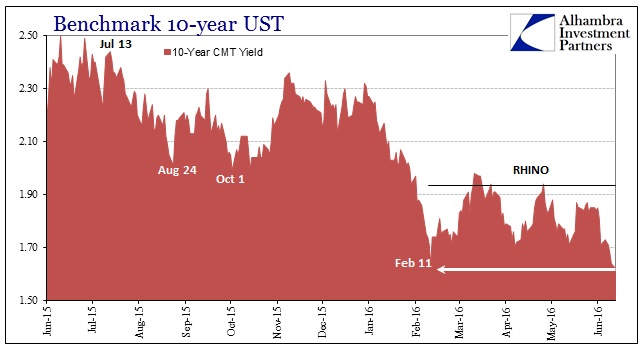

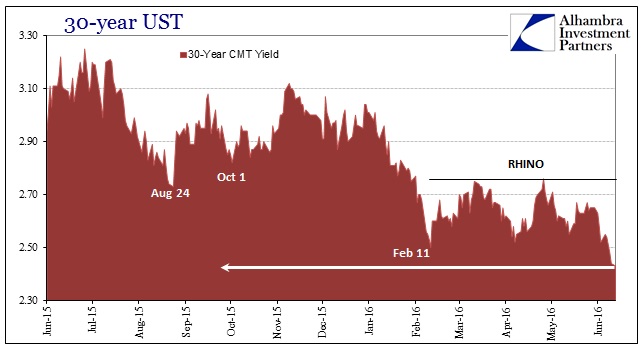

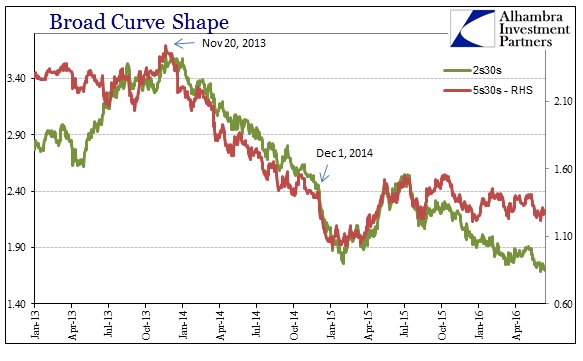

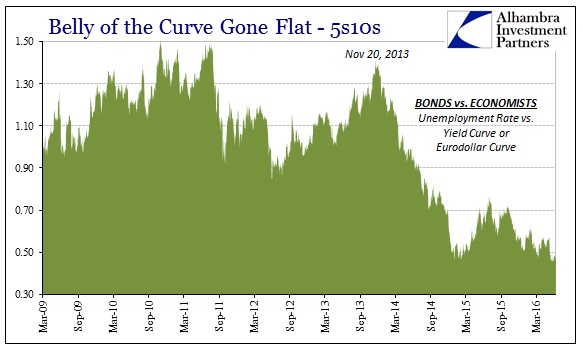

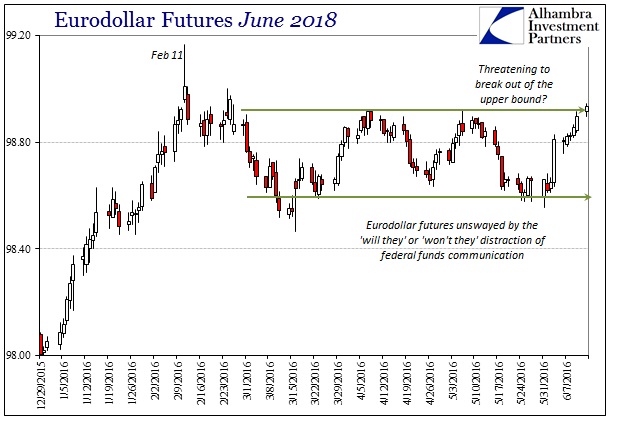

A scan across credit and funding confirms the unease. Eurodollar futures continue to be bid, flattening the “curve” that hasn’t been one in almost a year. The same is true of the UST curve, also shriveled to new lows in far too many parts.

From nominal rates to calendar spreads (to gold and maybe francs, subscription required), surpassing February 11 and the endpoint comparison for the last liquidation is an important development. There is a fundamental level to all this that seemingly escapes risk markets that are in many ways continuing to grope for the optimistic side even if momentum has faded. In other words, reality is setting in that the “rebound” from the start to the year never was anything more than an end to the liquidation disruption. Having lost the fundamental boost of that believed rebound, stock markets aren’t quite ready to accept the full weight of what that might mean.

From a financial standpoint, the view of global “dollar” liquidity has in many ways rarely been worse. The systemic baseline is atrocious, which suggests why hedging activity in risk markets is so attracted to knowable events. Liquidation is more than illiquidity; it is the combination of that with an uptick in selling. Thus, low liquidity increases the chances of a minor selling episode getting out of hand, careening toward self-reinforcing.

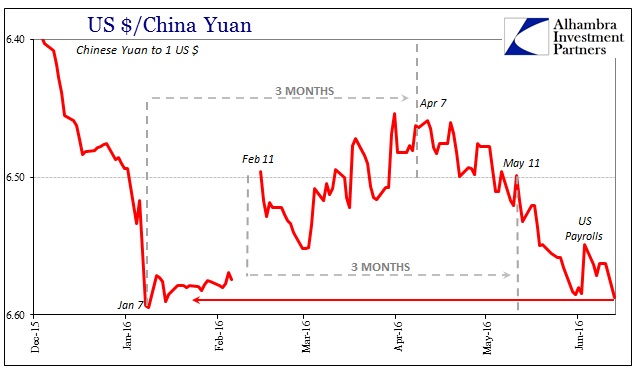

Behind it all is the global financial environment running at only further reduced capacity. As expected, CNY traded down sharply today after China reopened from last week’s holiday. At nearly 6.59, that was the lowest level since early January when the PBOC started its “dollar” interventions. That means the central bank added enormous effective cost to its unending string of intermediation for no net gain except 3 months of artificial calm. It may be a little while longer but it seems very likely we will find out just how much that fleeting moment actually cost.

With the 6-month forward CNY trading near or above 6.61 in six out of the past nine trading days (not including holidays), the one-day “dollar” euphoria of US payrolls is an increasingly distant memory. In short, liquidity is brutal, safe havens are bid in only anticipation of all that seems to remain: the selling trigger. Unpredictability (chaos theory) suggests an unknown “butterfly”, but you can’t blame market agents for sticking to the known unknowns. What is really unknown is how global markets react at something less than 6.60; it hasn’t happened yet in this (“devaluation”) direction.

It means for the time being there will be far too much attention on Brexit when the real story is in the other direction on the other side of the world. If we only knew whether that means Hong Kong or Tokyo we would be making real progress.