The stock and bond rallies went flat in August and bonds sold off in September as heavy Treasury supply and foreign sovereign liquidation of Treasury holdings created friction in the markets. Liquidity is still growing slowly but the market response to rising liquidity has been diminishing as friction builds.

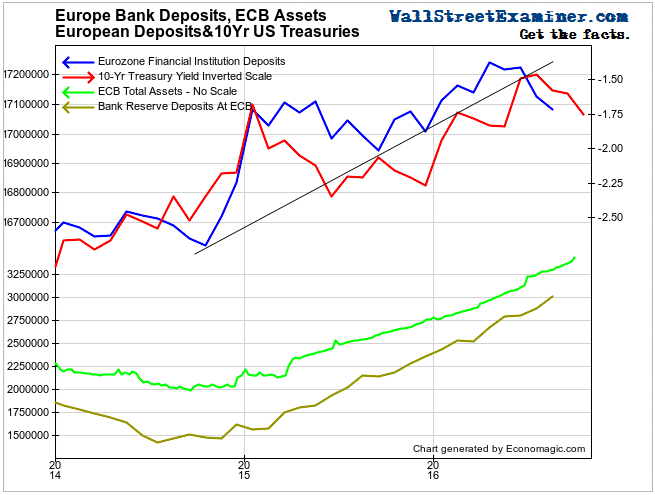

Liquidity growth in Europe has stalled as deposits there shrunk again. In spite of massive ECB money printing, European bank deposits have fallen for two straight months. That indicates not just capital flight, but cash extinguishment via loan repayments and writedowns. The culprit is NIRP, which discourages account holders from keeping large balances or buying negative yielding sovereign paper. It also puts downward pressure on US rates. That is only offset this month by the fact that the Treasury is unleashing massive new T-bill supply on the market in October. This will absorb excess cash, and bring this pressure to bear on US stocks and bonds for the remainder of the month. That could reverse in November.

Meanwhile, US banks have been buyers, but not enough to offset big increases in Treasury supply and foreign central bank liquidation of their Treasury holdings at the Fed. This negative trend isn’t likely to reverse any time soon. It has been sufficient to stop the stock market rally and cause a correction in bond prices. Unless financial pressures ease around the world, and there’s no sign of that, this will likely continue to be a negative factor for the longer run. This trend began a couple of years ago, and could get worse.

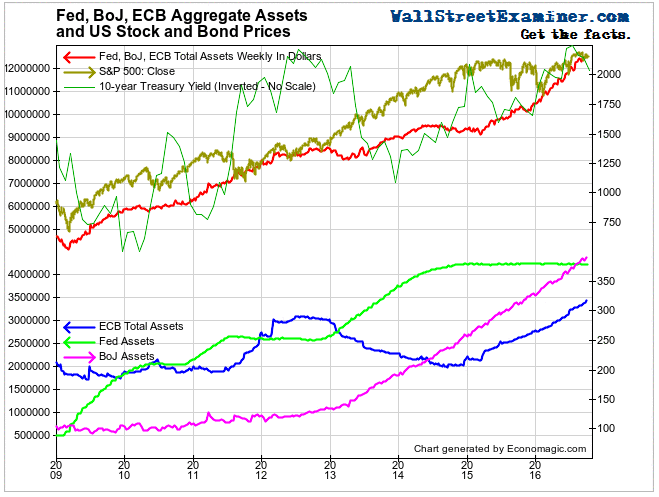

In a world of instant interconnection, liquidity anywhere is liquidity everywhere, flowing especially to the US. As goes the money printing in the US, Europe and Japan, so go the US markets. The Fed need not print because some of the money from ECB and BoJ printing always flows into the US. So stocks and bonds move in the same direction as ECB and BoJ QE.

Where bears may have a toehold is in the fact that while the direction of QE and the markets are the same, the proportions are not. ECB and BoJ QE are running into more and more friction as account holders in those markets slowly but surely find ways to deleverage and extinguish deposits. Eventually, the markets could take over that function via margin calls. We’re not there yet, but QE no longer has the same market moving power that it once did.

The Details

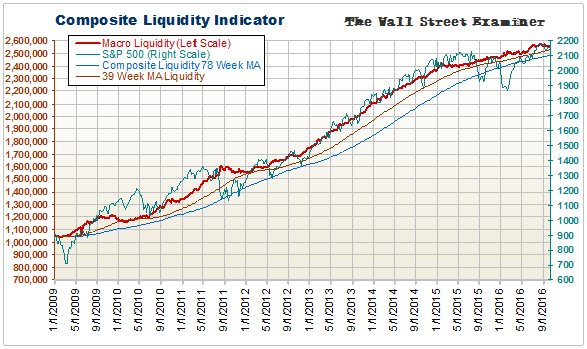

The Composite Liquidity Indicator (CLI) US macro liquidity was virtually unchanged in September but it remains above a slightly rising 39 week moving average. The market has shown a propensity to trade below the CLI trend for the past year. If liquidity stays flat we could see bigger selloffs ahead. Conversely any upside surge in the SPX should not exceed roughly 2275. 9/7/16 Flat liquidity growth from January to June led to a rangebound performance for stock prices. Stocks broke out in July following the June liquidity surge. Liquidity should grow slightly again in September after the Fed has its monthly MBS settlements at mid month.

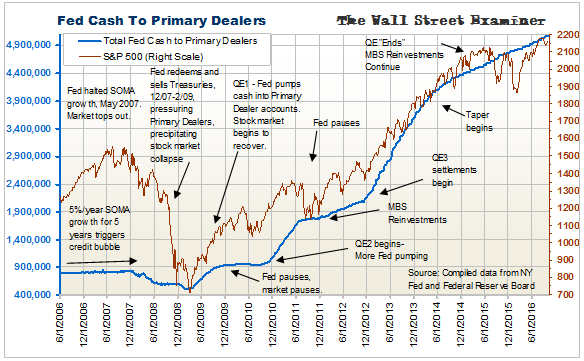

Fed Cash to Primary Dealers This indicator upticked with the Fed’s regular mid month MBS purchase settlements. The mid September settlement totaled $37.5 billion. The October settlement should be similar. That cash helps to put a bid under stock and bond prices during the settlement periods which are in the third week of the month.

We foresaw that these numbers would increase from earlier this year as a result of the decline in mortgage rates. These larger settlements should last for another month or two, then drop back again to the $25-30 billion range because of the recent uptick in 1o year Treasury yields. 30 year mortgage rates are typically indexed to that rate plus a fixed margin.

Increasing Treasury supply will absorb much of the increase in MBS.

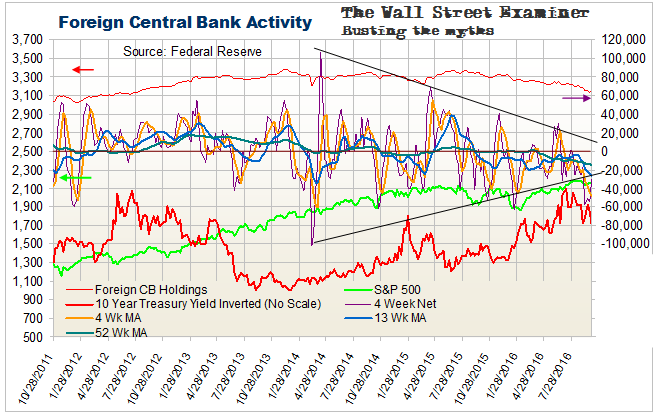

Foreign Central Bank (FCB) Purchases The Fed’s custodial holdings of Treasuries and Agencies for FCBs fell by $30 billion for the 4 weeks ended October 5. As weak as that is, it’s actually a bounce from an oversold low.

Both the intermediate and longer term trends remain down because financially stressed foreign governments have been liquidating their reserves of Treasuries to raise cash. Treasuries have weakened in recent weeks as the FCB liquidation picks up steam. If FCBs don’t start buying more, this could be the death knell for the Treasury bull market, especially considering that Treasury supply should rise as the US economy continues to barely grow. Weak growth means weak Federal tax revenue, which then requires more borrowing.

In spite of weak FCB buying, Treasuries and US stocks have held up as capital flees Europe and Asia to the Last Ponzi Game Standing in the US.

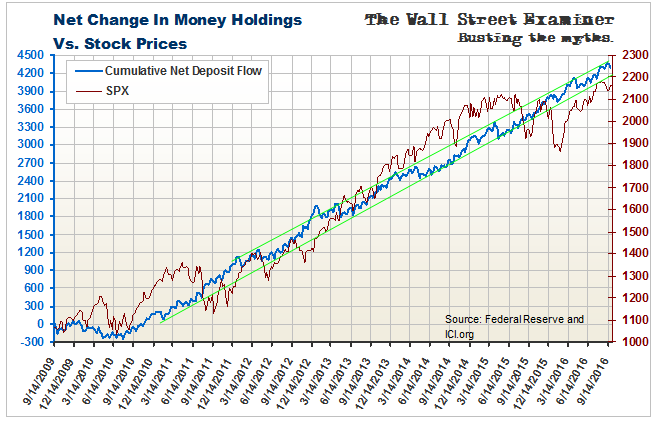

US commercial bank deposit flows, not to and from money market funds, rose by only $10 billion in the 4 weeks ended September 26. That was a just off a new high set 2 weeks before. The current level is mid channel in a well defined trend going back to 2010.

Pending a clear break of that channel, this trend will continue to represent a bullish influence, but no longer one that always underpins an extended upleg. We saw a massive failure in Q3 2015 and Q1 2016. Since then, the market and bank deposits have been moving in tandem again but stocks are now persistently below the money trend. Prior to 2015 stocks had fluctuated around the trend, both above and below.

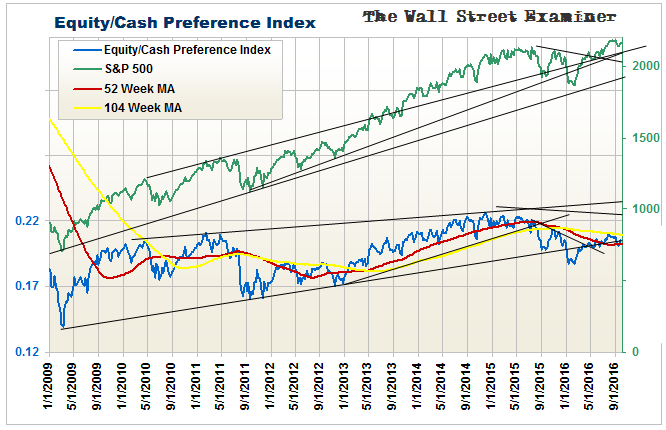

The Equity/Cash Preference Index has not followed through on a breakout above the 52 week moving average and a year long downtrend line. This isn’t necessarily bearish. There was similar action around the 2012 liftoff. That market took a year before this indicator finally cleared the 104 week moving average. The current market is weaker with only an 8% gain versus a 17% gain at a similar point in time after the 2012 low. This situation bears watching. It could be a sign that the bull move has run into increased friction from selling, which could lead to a reversal.

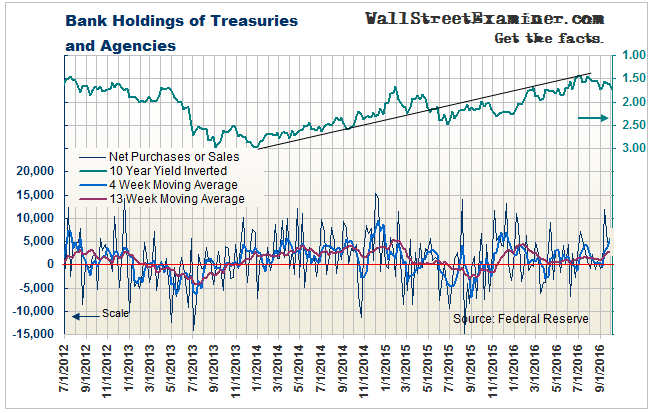

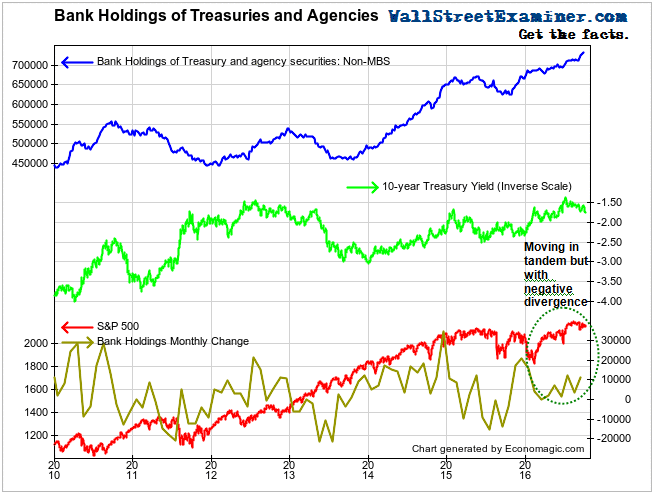

US Commercial bank holdings of Treasuries and Agencies rose by $20 billion in the 4 weeks ended September 28. The 4 week and 13 week moving averages turned back up from near the zero line. This indicator had been in a neutral pattern since April. It is currently a bullish pattern. However, FCB liquidation and increasing Treasury supply are running the other way, and blunting any bullish impact of bank buying.

My thinking had been that as long as these lines remain at least minimally positive the rally was likely to go on. Any increase in buying could push the stock and bond rallies, or one of the two, to accelerate. For example, if bonds begin to sell off, stocks should move up faster on rotation. But this may no longer be sufficient to drive prices up, given the increasing friction from FCBs and Treasury supply. If bank buying ever stops and reverses while FCBs are still selling and Treasury supply still rising, it could be the bearish long term signal we’ve been waiting for.

US Commercial Bank Treasury Purchases

US Commercial bank holdings of Treasuries and Agencies rose by $20 billion in the 4 weeks ended September 28. The 4 week and 13 week moving averages turned back up from near the zero line. This indicator had been in a neutral pattern since April. It is currently a bullish pattern. However, FCB liquidation and increasing Treasury supply are running the other way, and blunting any bullish impact of bank buying.

My thinking had been that as long as these lines remain at least minimally positive the rally was likely to go on. Any increase in buying could push the stock and bond rallies, or one of the two, to accelerate. For example, if bonds begin to sell off, stocks should move up faster on rotation. But this may no longer be sufficient to drive prices up, given the increasing friction from FCBs and Treasury supply. If bank buying ever stops and reverses while FCBs are still selling and Treasury supply still rising, it could be the bearish long term signal we’ve been waiting for.

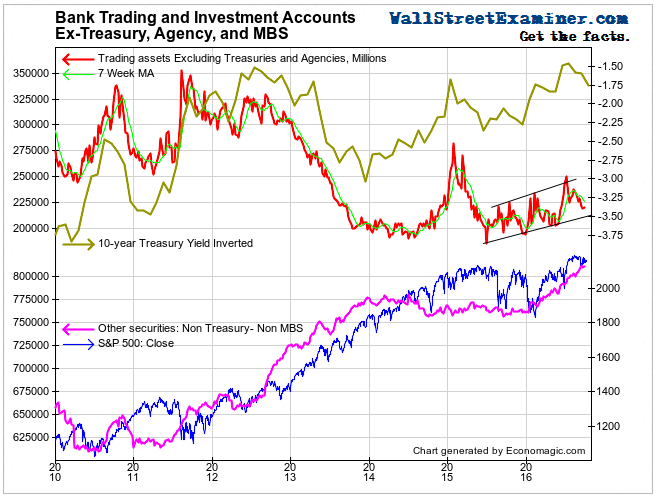

Bank Non Treasury Trading and Investment Accounts

Trading assets fell slightly in the 4 weeks ended September 28. They remain within the 2015-16 uptrend channel. However, they are also still below the 7 week MA. Breaking that correctly forecast that bonds would sell off. This signal will remain in force until buying turns up.

The long term Non-Treasury, non MBS investments have been uptrending for a year. They broke out above the 2014 highs in mid year. Because these accounts are carried at cost it means that the banks have been adding long term assets, both leading and mirroring the rally in stocks. The breakout implied that stock prices would follow and they did. Turns in this series typically lead stock prices by weeks or months.

Effects of Other Central Banks on US Markets

Total assets on the ECB balance sheet increased by €80 billion over the 4 weeks ended September 30. These funds flow into the European banking system.

In a world of instant interconnection, liquidity anywhere is liquidity everywhere, flowing especially to the US. As goes the money printing in the US, Europe and Japan, so go the US markets. The Fed need not print because some of the money from ECB and BoJ printing always flows into the US. So stocks and bonds move in the same direction as ECB and BoJ QE.

Where bears may have a toehold is in the fact that while the direction is the same, the proportion is not. ECB and BoJ QE are running into more and more friction as account holders in those markets slowly but surely find ways to deleverage and extinguish deposits. Eventually, the markets could take over that function via margin calls. We’re not there yet, but QE no longer has the same market moving power that it once did.

Bank deposits in Europe fell in August for the second straight month in spite of the ECB’s massive QE. This reflects the perverse incentives inherent in NIRP. If this gains traction, it will mean big trouble for not only Europe but the US as well as the incentives toward deposit contraction will turn into outright liquidation of assets.

It is too soon to call the downturn in European bank deposits a major trend change, but it’s a yellow flag. A persistent decline could be bad news for Treasuries and for stocks. Slow growth means that money is being siphoned off to the US and elsewhere. No growth, however, suggests outright money destruction via loan repayments and write-offs. It’s a fine line. The European banking system may be transitioning from slow growth to no growth, and maybe even to contraction (covered in more detail earlier this month).

Open Market Operations (OMO), Monetary Policy Actions, and Interest Rates

The size of the Fed’s balance sheet fluctuates between $4.4 and $4.5 trillion each month as MBS are paid down and then more are purchased to replace the paper that was paid down.

The Fed is currently between its regular mid month settlements of forward MBS purchases.

The MBS settlements take place around the third week of every month. July settlements totaled $33.2 billion. August’s totaled $36.2 billion. September’s rose to $37.5 billion. October should be around the same.

The increase has been due to increased refinancing because of falling mortgage rates. Borrowers refinance and pay off existing mortgages when rates fall. These payoffs result in paydowns of MBS held by the Fed. The Fed then replaces those in the following month. This cash keeps the Fed’s balance sheet level while cashing out the Primary Dealers who sell the paper to the Fed. They then have more cash to play with.

However, mortgage rates reversed in September, heading higher. This will result in fewer refis, fewer MBS paydowns, and a month later, a lower volume of Fed purchases. We should start to see that effect in November. Reduced Fed purchases would mean less support for the markets.

Heavy new Treasury supply in August and September (see Treasury update) was greater than the amount of Fed cash injected into dealer accounts. The markets were dependant on external liquidity flows for lift. They got it in August, but something went wrong in September. Significant foreign sovereign fund liquidation appears to have played a role. There’s no sign, nor no reason to think, that this will turn positive any time soon.

New Treasury supply in October is now expected to total around $86 billion based on the TBAC estimate issued in August. Virtually all of that will be in T-bills, which would suck cash out of the accounts of investors, traders, and dealers put upward pressure on short term rates. Under the circumstances the markets will face as much or more supply friction this month than in September, which should make it tough for stocks and bonds to post significant gains, and would create the conditions for more of a correction.

After a year long pause in the disappearance of the Fed Funds market, it appears to be on the verge of further shrinkage, leaving just a shell of a market, reinforcing the fact that the Fed Funds rate is a completely phony measure of interest rates. The money market already shows signs of trading lower. Only the massive influx of new T-bill supply over the rest of October could hold the market at these levels. Otherwise, rates would head toward negative territory as foreign cash continues to flood into the US, driven by the NIRP penalty at home.

This report is excerpted from the Wall Street Examiner Pro Trader Macroliquidity report on the major international and domestic liquidity flows driving the markets for US stocks and bonds. Try the service for 90 days risk free.