“.

Today’s “Thoughts From The Beach” picks up on a couple of articles I read over the last few days. With the markets breaking out to new highs, the bull market commentary has been expanding quickly. As you know, I have increased equity allocations in models with the breakout, but this is a tactical position only. The fundamentals by no means support the rising risk levels in the market currently. Let’s take a look at a 3-Things worth considering.

Money In The Mattress?

Here is a myth that just won’t seem to die: “Cash On The Sidelines.”

This is the age old excuse why the current “bull market” rally is set to continue into the indefinite future. The ongoing belief is that at any moment investors are suddenly going to empty bank accounts and pour it into the markets. However, the reality is if they haven’t done it by now after 3-consecutive rounds of Q.E. in the U.S., a 200% advance in the markets, and now global Q.E., exactly what will that catalyst be?

However, Clifford Asness summed up the problem with this myth the best and is worth repeating:

“Every time someone says, ‘There is a lot of cash on the sidelines,’ a tiny part of my soul dies. There are no sidelines. Those saying this seem to envision a seller of stocks moving her money to cash and awaiting a chance to return. But they always ignore that this seller sold to somebody, who presumably moved a precisely equal amount of cash off the sidelines.

If you want to save those who say this, I can think of two ways. First, they really just mean that sentiment is negative but people are waiting to buy. If sentiment turns, it won’t move any cash off the sidelines because, again, that just can’t happen, but it can mean prices will rise because more people will be trying to get off the nonexistent sidelines than on. Second, over the long term, there really are sidelines in the sense that new shares can be created or destroyed (net issuance), and that may well be a function of investor sentiment.

But even though I’ve thrown people who use this phrase a lifeline, I believe that they really do think there are sidelines. There aren’t. Like any equilibrium concept (a powerful way of thinking that is amazingly underused), there can be a sideline for any subset of investors, but someone else has to be doing the opposite. Add us all up and there are no sidelines.”

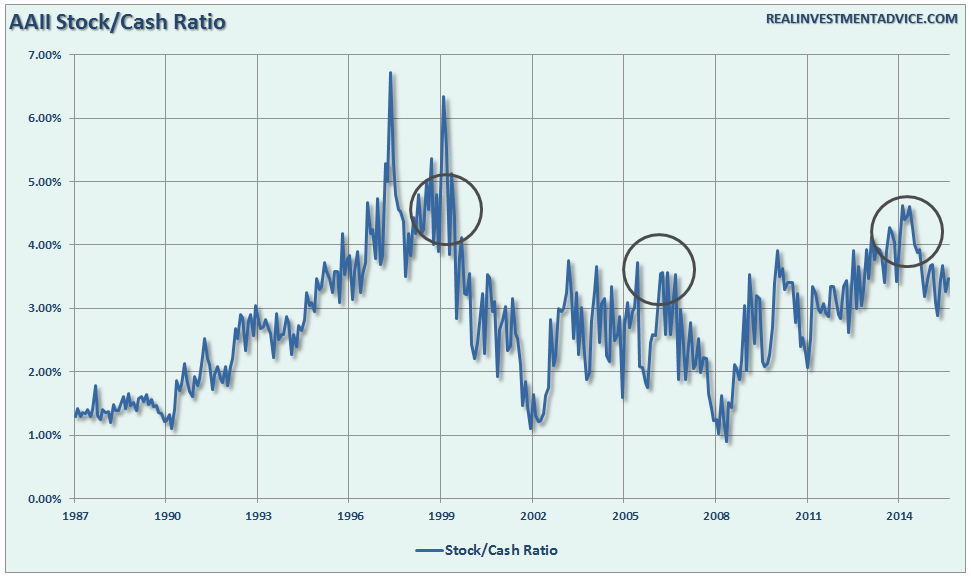

Furthermore, despite this very salient point, a look at the stock-to-cash ratios also suggest there is very little available buying power for investors current.

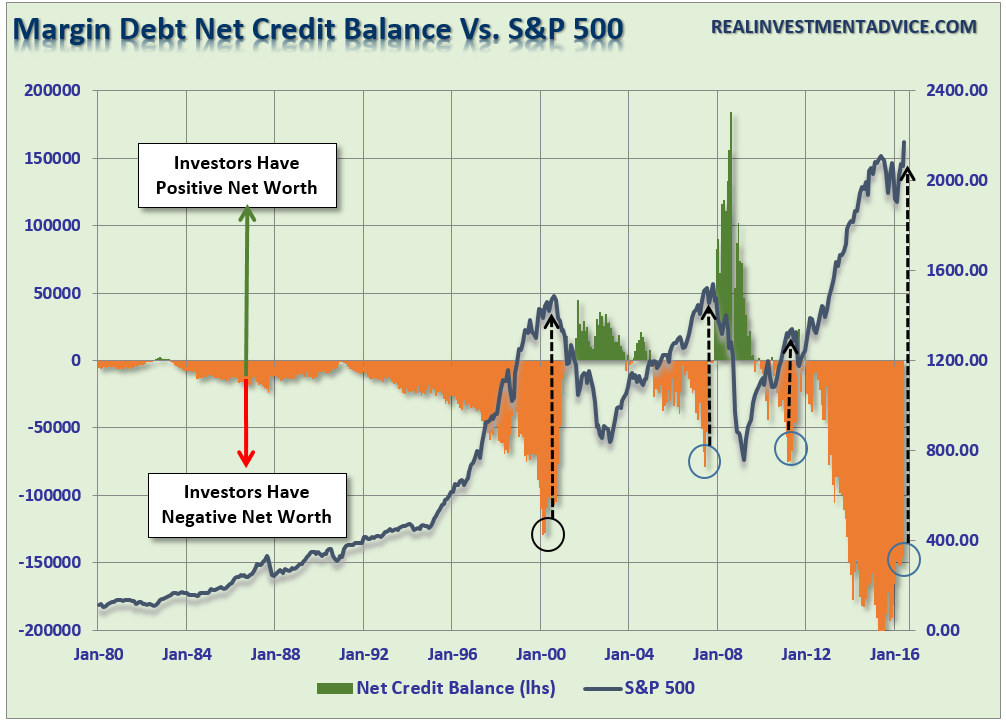

Margin debt levels, negative cash balances, also suggest the same.

Cash on the sidelines? Not really.

All About That Yield

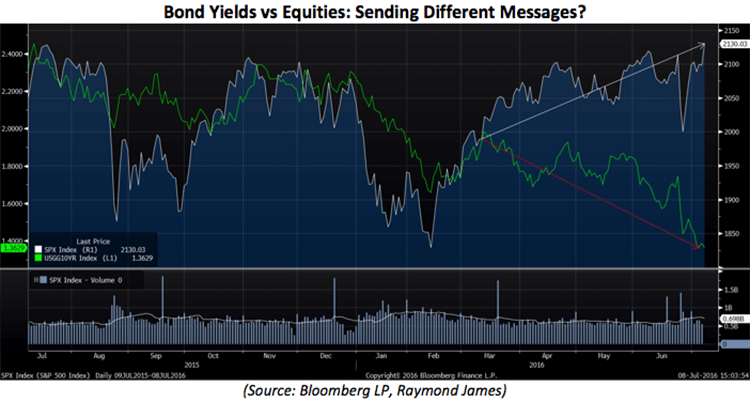

Despite the recent surge in the financial markets, the key to everything is found within the realms of the bond market. On both a global and domestic front, the bond market is telling a very different story about the economy and world we live in versus what is being assumed by the stock market.

A recent note by Benjamin Streed, via Raymond James, summed up this point well. To wit:

“However, the global bond markets appear to be singing a very different tune as increasing amounts of global sovereign debt is pushed into negative yields thanks in part to monetary policy in Europe and Japan. As we’ve noted in previous writings, domestic monetary policy is unclear/uncertain (at best) but the one thing that is becoming strikingly obvious is the undeniable influence overseas central banks are having on the US bond markets. For example, recent estimates have negative-yielding sovereign debt in the vicinity of $10 trillion leaving many ‘safe haven’ investors in dire need of not just safety and liquidity but a positive yield. If you’re an overseas investor, it’s almost a no-brainer that you’d seek out these high yielding instruments that also just happen to be the world’s largest and most liquid ‘risk-free’ asset. According to Citigroup, US Treasuries now account for nearly 60% of all positive-yielding sovereign debt and also represent ~90% of all positive yields with a short maturity of less than one year. If you want/need to stay short-term and risk-free, there is apparently only one place on the entire planet to go, here. Think about the potential ramifications of that last statement; how much will US monetary policy (the Fed) really influence the short-end of the yield curve if T-bills are the only game in town for short-term, high-quality debt? There are some indications that this demand is already having a meaningful impact on some of deepest parts of the Treasury market.”

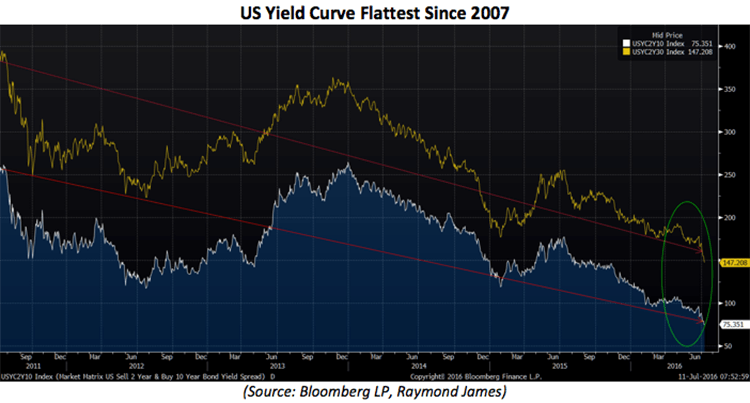

“According to US Treasury data, demand for US Treasuries is so high that ‘stripping’ bonds, i.e. separating a bond into its component principal and interest payments now stands at a record $223 billion, the highest level in more than seventeen years. Most of the stripping is focused on maturities in 2045 and 2046, utilizing the most long-term of all US securities available in the market. In many ways, who can blame them? Year-to-date, the benchmark 30-year bond has returned a staggering 22% and is up nearly 26% over the last twelve months. For those investors willing to maintain longer-term bonds in their portfolios, duration truly has been their friend. As a result of the ongoing ‘duration demand’, the Treasury curve has flattened to its lowest levels since 2007 (see the chart below). The difference in yield between the 2yr and 10yr Treasury notes sits at only 75 basis points (bp) while the 2yr to 30yr difference is a mere 147bp.”

“Meanwhile, with the recent equity rally the markets are at a clear inflection point with equities at/near record highs and yields at/near record lows. Equities at all-time highs would indicate that Brexit-related concerns have subsided and that the ‘all clear’ has been signaled. However, bond yields at record lows offer up a conflicting view of the world, or at least one that is much less convinced that the ‘all clear’ has been signaled at this juncture.”

As is always the case, somebody is going to be very wrong. What is important to remember is two things:

- All bond yields are relative and U.S. debt yields can’t remain positive in a global sea of negative rates indefinitely. Yields will fall eventually inverting the yield curve as the next recession begins.

- Money flowing into U.S. debt for a positive yield will also push the U.S. dollar higher. This will negatively impact oil prices and crush expectations for a “hockey stick” recovery in earnings which has been a primary “bullish support” of the current advance.

Saw This In 2007

Adam Koos, via MarketWatch, had a very interesting piece out this week:

“It’s happened before and it can happen again — deceived investors piling onto an all-time-high in the stock market only to find themselves victims of a ‘bull trap.’ For those new to the term, a bull trap is simply a humbling false market signal, and we’re living right in the middle of potentially one of the biggest ever.”

I have substituted charts for Adam’s only so I can make a couple of additional points. But for now, let’s get back to Adam:

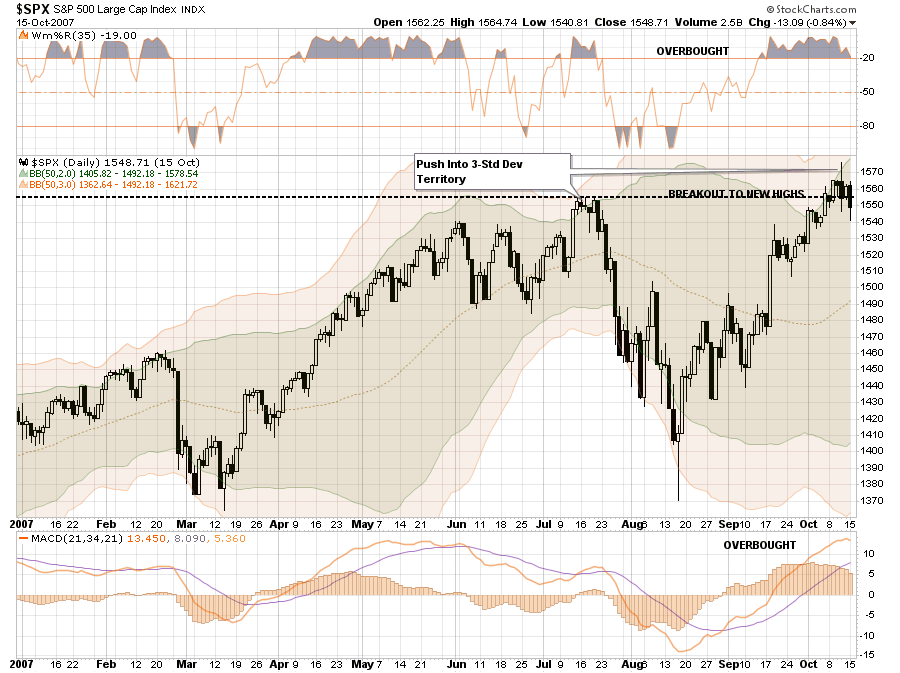

“In 2007, the market had become long in the tooth after rebounding from the pop of the tech bubble. The S&P 500 corrected mid-year and as the market began to show signs of fatigue, it managed to scrape higher, printing a new all-time high, which also brought excitement to investors and professionals everywhere. ‘The bull market was back!’ There was nothing to worry about … but they were wrong.”

Note in the chart above, at the time of the previous push to new all-time highs in July 2007 the markets were pushing 3-standard deviations of the intermediate term moving average with the all primary indicators in an extreme overbought territory. For the importance of a 3-standard deviation extension, see my previous post on pushing extremes.

I don’t need to remind you what happened following that short-lived bullish exuberance of new highs. The subsequent 53% loss wiped out years of previous gains and set investors back more than a decade from their retirement goals.

Back to Adam:

“Since the bottom of The Great Recession in March of 2009, the market has clawed its way to the title of ‘Second-Longest Bull Market in History.’

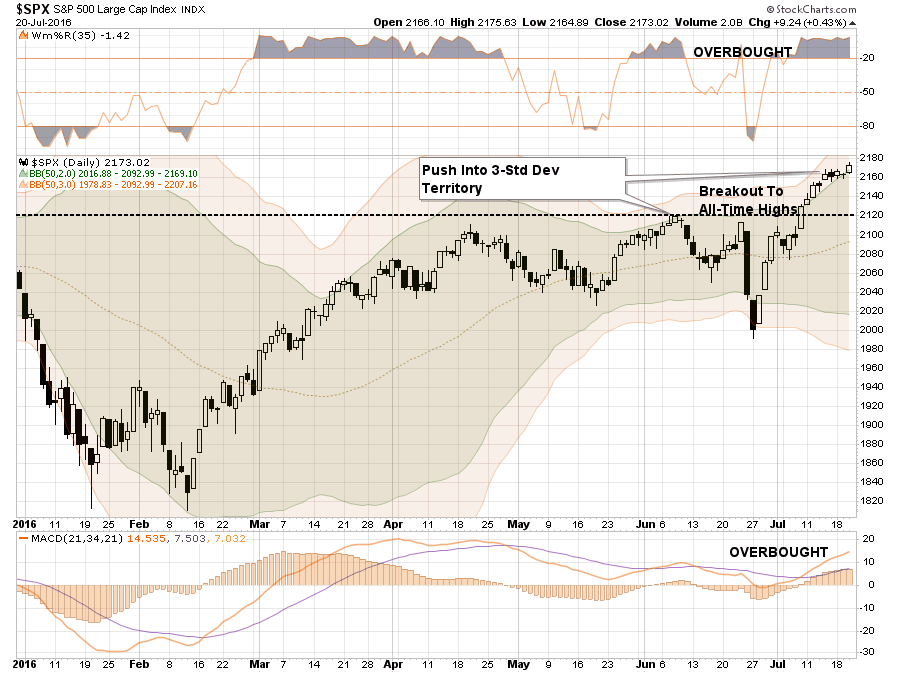

So, here we are today, squeaking by with new all-time highs, and all the news is about the next big leg of another healthy bull market”

As it was in 2007, we once again see a market breaking out to new highs with all of the bullish excitement and exuberance to accompany it. The problem is, just as we saw in 2007, the markets are pushing well into 3-standard deviation extremes with extreme overbought conditions.

Does this mean the market is about to collapse again? Not necessarily, but as a portfolio manager I must be prepared for all possible outcomes. Adam, picks up on some additional points of concern:

“The single biggest reason bull markets come to an end is because the price of stocks rise to a point at which investors no longer see value in owning them. What seems to accompany each bounce in the market is:

- A decline in volume, indicating that enthusiasm is following downside pressure and not the buying excitement

- An increase in the number of companies that have fallen more than -20% off their 52-week highs.

Regarding number one, typically, volume drops when a bull market is long in the tooth. Since the February lows when trading volume on the NYSE stood at around 4.9 billion, while the market has had a good run off those lows, Monday’s volume stood at less than three billion.

With regard to number two, between the last two market tops, the percentage of companies on the NYSE that are down more than 20% off their highs actually rose from 25% in May to over 33% in July.

When market crashes occur, it starts with the small caps, then bleeds into the mid caps, and eventually all the buying climbs the ladder toward safety, dividends, and yield in utilities, metals, materials, REITs and blue chips — exactly the stocks that have been exhibiting the most strength lately. Coincidence?“

As I have stated previously, the “yield chase” has led investors into some of the most dangerous territory seen at any time since the “Nifty Fifty” in the late 70’s. With complacency extremely high, a very crowded trade in “yieldy stuff,” and little liquidity in the markets, the potential for a very nasty mean reversion in the areas perceived to be “safe” could readily occur.

And, as in 2008, investors will once again start questioning the wisdom of putting their life savings at “risk” in the Wall Street casino.

Just some things I am thinking about.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In