The Fed’s weekly H8 statement covers a wealth of esoterica on the state of the US commercial banking system. We covered the broad data on loans and leases on Friday.

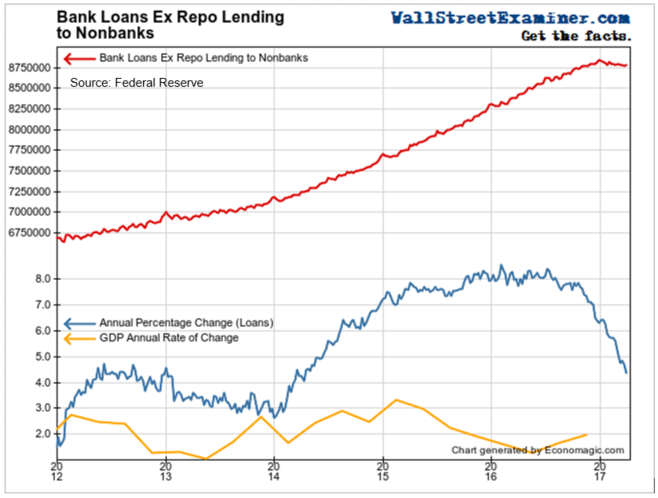

Excluding repo lending and loans for securities holding, aka margin, here’s how the total growth of lending for personal and commercial purposes looked. We have had a bubble and it has slammed on the brakes. How do we know it has been a bubble. When loans are growing at 7-8% per year, and the economy grows at 2%, what else would you call it. Borrowing grew at 4 times the rate the economy was expanding. The rest of it was a chase for speculative profits. Its fun for the profiteers while it lasts, but we know how such frenzies end.

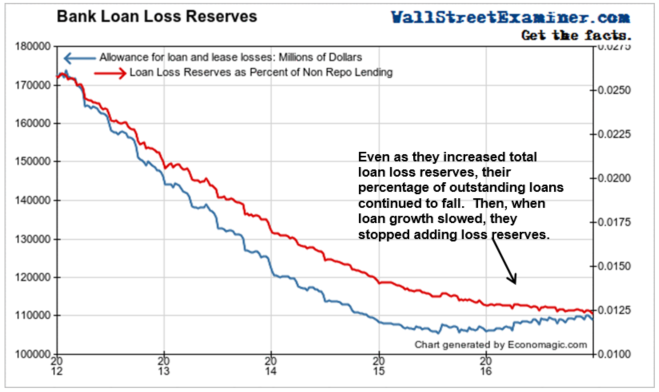

Loan Loss Reserves It’s clear from the collapse of the growth rate that this one is ending. But as the risks grow, bankers bury their heads in the sand. Banks’ loan loss reserves reached a post crisis record low as a percentage of loans outstanding in March. This is just another symptom of the steadily building systemic risk inherent in bubble behavior. Such imprudent behavior is a hallmark of the cycle of confidence increasing to the point of irrationality.

Bankers are counting on a growing economy to keep the loans they have issued for the past few years from going sour. A growing bubble can hide a multitude of sins. Once that growth stops, those sins are uncovered in the form of non performing loans and they can wreak havoc.

As loans outstanding have soared and GDP growth has slowed, you would think that bankers might recognize the increasing risk and set aside a bit more in reserves. But they haven’t seen it that way. They cut loss reserves from $170 billion to $106 billion between 2012 and mid 2015. Since then they rebuilt reserves at far below the rate that their lending grew. As a result their loan loss reserves fell to 1.25% of non-repo loans outstanding. That’s hardly a safety cushion. What happens when the economy weakens and loan losses soar?

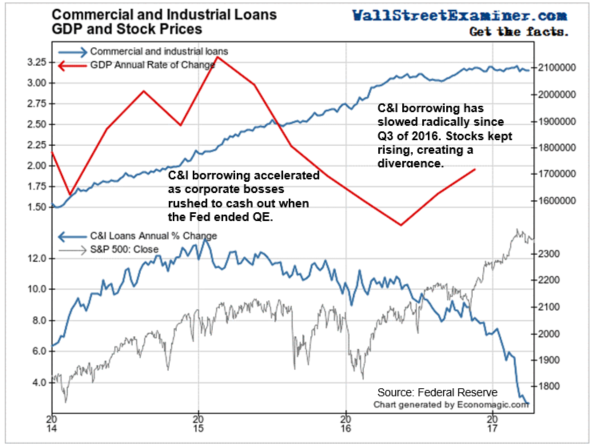

Commercial and Industrial Loans have not grown at all since October 2016. The annual growth rate is collapsing, now down to just over 3%, from 6% in January. That’s down from more than 13% in early 2015.

The sharp slowdown in C&I loans now also signals that corporations have all but stopped doing financial engineering deals. That told us that the stock market rally was running on fumes over the past 5 months since the election.

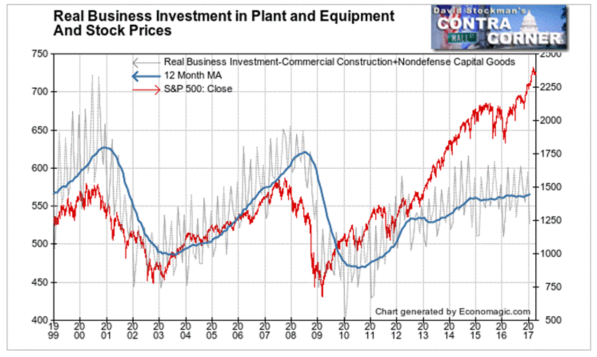

Real Business Investment

Meanwhile, as the stock market barreled higher, real business investment in plant and equipment stalled (chart below). Bankers may have been confident in their future prospects, but the biggest customers of the banks apparently were not. Businesses essentially stopped growing their investments in tangible assets late in 2015.

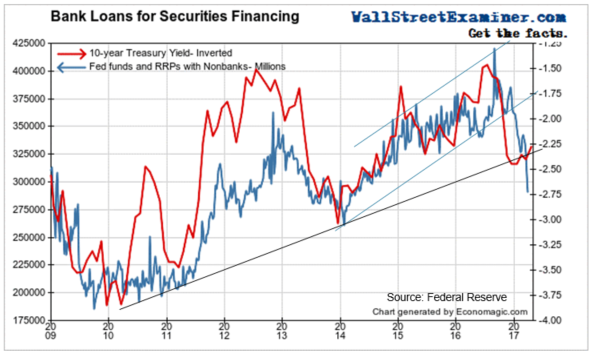

Margin and Repo Lending Repo loans to nonbanks to finance carry trades and other securities holdings are crashing. In February they broke a 3 year uptrend channel. The decline picked up steam in March. They have now also broken a 7 year trendline.

The rally in bonds is defying this. It is a temporary artifact of the artificial reduction in supply because of the debt ceiling. When there’s no new paper on the market and demand is constant, prices rise and yields fall.

This is a temporary condition. It is a gift for holders of long term paper. It’s time to get out, or at least dramatically shorten maturities. The market is giving bond traders every opportunity to do so. In fact, the collapse in repo lending to nonbanks is as clear an indicator there is that professional traders are getting out.

These carry trade loans have been declining since they spiked to an all time high in mid September at top of the channel. They have now decisively broken a 7 year trendline. It almost certainly means the end of the speculative bubble, and the beginning of a bear market in bonds and stocks. The traders clearly believe the Fed’s signals that it will soon start shedding assets, which will put downward pressure on prices. The pros are now beating an exit, ahead of the crowd, before it’s too late.

Fed Funds Outstanding The Fed pretends to control the Fed Funds rate, but it’s a shell game. There is no Fed Funds market. The whole thing is rigged for show. In the old days the Fed deliberately kept reserves tight. Banks would borrow or lend to one another depending on their reserve positions to meet required levels of reserves. The Fed could influence the rate by adding or subtracting small amounts of reserves to or from the funds market. The did so with daily Temporary Open Market Operations using overnight or very short term repurchase agreements (repo).

Today, with $2.7 trillion in excess reserves in the system, Fed Funds outstanding are a shadow of what they once were. Banks simply don’t need to borrow reserves at all. The only banks that do are the sickest ones, kept on life support with smoke, mirrors, and the self interest of the big boys in the system. So here’s how the Fed Funds market looks now.

Every day the Fed conducts a sham market, where Primary Dealers carry out a few billion in Fed Funds transactions in sham trades in the Fed’s target range to make it appear that the Fed controls rates. In a sense, they do at the short end of the market. But $50 billion outstanding in Fed Funds borrowing and current daily volume around $75 billion aren’t even a pimple on a rounding error’s backside in a market with $9 trillion in bank loans and countless trillions in other kinds of debt outstanding.

But the Fed must maintain the appearance of control at all costs. Otherwise, it has nothing. Loan growth is collapsing, in particular margin and repo lending for carry trades. The Fed has done its job of convincing the market all too well. Now it is talking about shrinking its balance sheet. As it peels off assets, that will constitute a real strengthening. Even if it’s done in ultra slow motion as the Fed’s trial balloons are signaling, the illusion that the Fed is in control will melt away. What comes next we don’t know. But it surely won’t be pretty.

Parts of this report are excerpted from Lee Adler’s Wall Street Examiner Pro Trader Monthly US Banking Report.

Lee first reported in 2002 that Fed actions were driving US stock prices. The US Treasury has also played a role in directly moving markets. Lee has tracked and reported on those relationships for his subscribers for the last 15 years, helping to identify major turning points in the markets in their earliest stages. Try Lee’s groundbreaking reports on the Fed and the Monetary forces that drive market trends for 3 months risk free, with a full money back guarantee. Be in the know. Subscribe now, risk free!