By Tyler Durden at ZeroHedge

Overnight, Credit Suisse – which itself has been a casualty of the global slowdown which has hit European banks hard in recent months – became the latest bank to join Goldman, JPM and increasingly more banks in predicting that 2016 will be a year in which investors will want to rotate out of equities. Specifically, the second largest Swiss bank said that it is “we reduce our equity weightings to our most cautious strategic stance since 2008 and take our mid-2016 S&P 500 target down to 2,150, the same as our end-2016 target.”

Here are the five reasons why CS just looked at the mounting wall of worry… and began to worry.

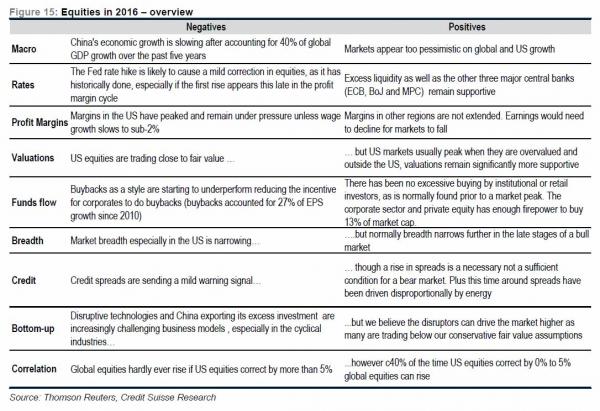

- US valuations are now in line with fair value: For the first time in five years, US equities are trading in line with their fair value on our two preferred valuation models. The equity risk premium is 5.4% (in line with our below-consensus EPS estimates), which is in line with our warranted ERP (which is based on credit spreads and ISM). Our fair value P/E model for the S&P 500 suggests a target multiple of 16.9x compared to 16.6x now, suggesting only 2% upside.

- Increasing macro headwinds: Global equities are facing two key headwinds in 2016: i) China’s economic growth has never slowed to such a degree when it has been such a major component of the global economy (with China having been responsible for c.40% of global GDP growth over the past five years); ii) The Fed is set to increase interest rates for the first time in 9.5 years. Historically, the drawdown in equities has averaged 7% after the first Fed rate hike but the first rate hike has not marked the end of a bull market, however, with equities, on average, rising 2.2% in the six months after the first rate hike. The risk on this occasion is that the first rate hike has not occurred this late into the profit margin cycle.

- Earnings momentum, credit spreads and buybacks: Earnings momentum is close to a 4 year low with US margins peaking; credit spreads have risen by more and for a longer period than they have prior to bear markets (and close to the amount seen prior to a recession); and buyback as a style is now underperforming, which may undermine what has been an important source of equity demand, and push corporates into increasing capex (a positive for GDP growth, but not for funds flows or profit margin) and Credit Suisse HOLT® analysis indicates that buybacks have accounted for 27% of EPS growth since 2012. M&A has also hit the bottom end of the range at which it, and equities, peak, though M&A lags behind equities by c.six months. We also worry that near-record corporate buying has not had a positive impact on US equities during the past year.

- The shift from capital to labour: A shift from capital to labour is clearly underway. Wage growth is accelerating (particularly in the US and the UK) and, as a result, the profit share of GDP is now falling, albeit from historical peaks. This shift is being aided by government moves to increase minimum wages, as seen in the UK, US and Japan. Other challenges for corporate profitability include attempts to close corporate tax loopholes (such as the OECD BEPS tax initiative).

- Bottom-up concerns: We struggle to recall another time when so many sectors have faced threats from disruption, regulation or emerging markets (relating to both endmarket weakness and the competitive threat). Moreover, we believe that the competitive threat posed by Chinese corporates continues to be under-estimated as China continues to over-invest, driving down the gap between the RoE and the cost of debt, as well as moving up the valued added curve.

For the “we prefer tables” crowd, here are the negative and positive factors that influence CS’ outlook.

Just to cover its hedges in a manipulated, centrally-planned global market in which global central banks have been the marginal price setter fo years, Credit Suisse notes that while it is the least bullish on US equities since 2008, it is “still overweight” on global stocks: “We revise down our equity weightings to a small overweight, being the

most cautious on equities in our annual outlook since December 2008 (we

turned tactically cautious in January 2013 and June 2011).”

That said, its stance on US equities is rather clear: “In some ways, our view on US equities is the opposite of our view on European, Japanese and GEM equities. This is why we leave our comments on 43% of market cap to the end.”

- Why do we remain underweight? (1) The US market has the lowest operational leverage, and thus it tends to underperform against a backdrop of rising global PMIs (currently, the relative performance of US equities appears consistent with global PMI new orders falling back to 50); (2) the Federal Reserve is, in our view, the most hawkish central bank globally as a function of its dual mandate in a country approaching full employment, focus on core inflation (with the BoE and ECB focusing on depressed headline measures) and relatively closed economy (which limits the impact of China’s exporting of deflationary pressures); (3) in the aftermath of the first rate rise in every tightening cycle, US equities have underperformed over the following six months; (4) many of our concerns on equities globally (labour gaining pricing power, margins at peak, the level of spare capacity in the labour market, M&A at high levels, poor breadth) are somewhat US centric; and (5) finally conventional, HOLT and Shiller P/E ratios are all at the top end of their historic range versus global markets.

- What are the risks to our underweight? The US has the lowest Chinese/GEM exposure of any region and corporates cut costs quicker than elsewhere when nominal GDP disappoints. These have been very supportive attributes in 2015 but, given that we see the prospect of GEM stabilising and global GDP picking up, could underpin US equity underperformance in 2016. The most supportive factors for US equities are fund flows, with US equity funds having experienced outflows relative to global equity funds, and the fact that the US dominates the potential of the internet plays, which remains a key theme for us.

Surely all of this is just more ammo for the Fed’s “rate hike at all costs” argument.

Source: The Five Reasons Why Credit Suisse Just Turned The Most Bearish On Stocks Since 2008 – ZeroHedge