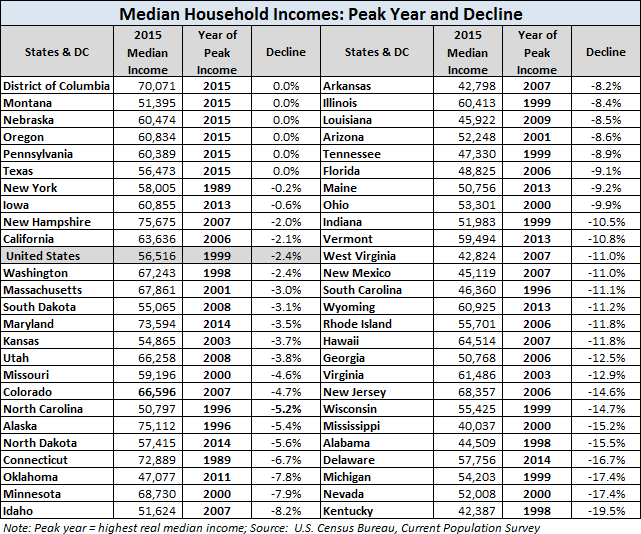

Sometimes a chart is worth a thousand words, and this is one. Real Median household income peaked way back in 1999 at $56,000 and by 2012 it was down 9%—an unprecedented decline. It goes without saying that Washington’s Keynesian ministrations on the money printing and national debt front didn’t much help.

In fact, the Fed’s balance sheet has expanded from $450 billion to $4.4 trillion during that period or by nearly 10X. Likewise, the national debt has nearly quadrupled to $17 trillion during the same period.

Well, all this monetary and fiscal profligacy did apparently help in one precinct: Namely, the Washington beltway where median household income reached its all-time high in 2012 (the last year available) of $65,200 and undoubtedly continues to rise. By contrast, 30 states reached their peak real household incomes more than a decade ago, and some reached that point more than two decades back.

The provinces have thus not kept pace with the imperial capital. Not by a long shot.

As also shown in the table below, 30 states have experienced a 10% or more decline since their peak year, and in 10 states the decline has ranged from 19% to 27%. Those figures do not represent merely a dip or even an extended setback. They amount to a devastating shrinkage in the standard of living being experienced by tens of millions of households.

Yet the mainstream narrative blathers on that the business cycle expansion is back on track and that last month’s numbers were a tad better than the month before. The table below says that’s all Keynesian bread and circuses—-the fleeting uptick interval between the serial bubbles and busts that our Washington overlords have condemned the people to endure.