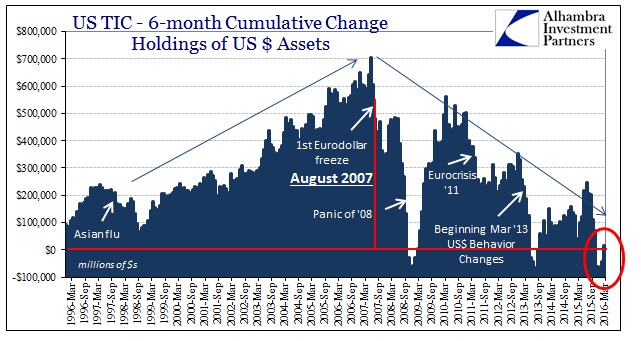

The Treasury Department’s updated official custody figures show us nothing unexpected. As usual, the TIC numbers are useful more so in corroboration of what contemporary analysis had already described. In the case of March 2016, we find just the sort of apparent reduction in “dollar” pressure that matches observation of general global conditions after February. Total net “flow” was +$64.7 billion, up from +$28.9 billion in February and -$33.4 billion in January. That is consistent with an end to general global liquidation via the eurodollar system at and around February 11.

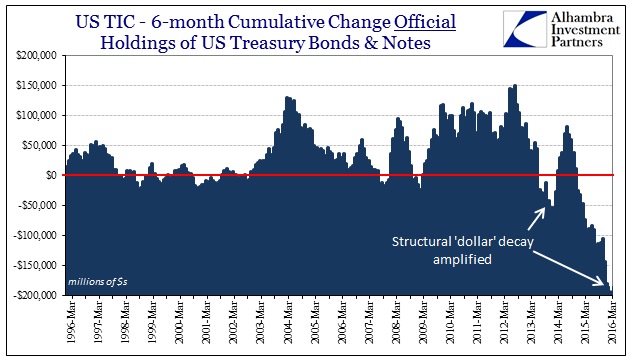

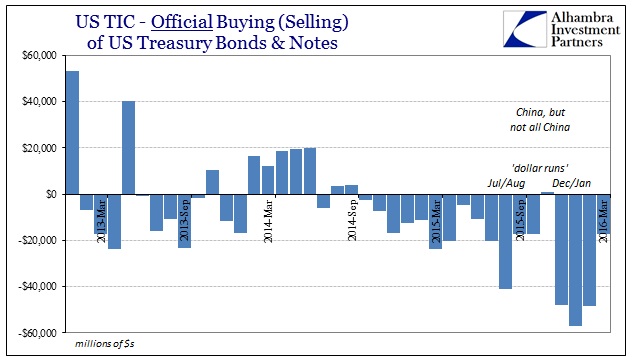

Improvement is, of course, a relative description which in this context only suggests absence of further liquidity pressure rather than an actual rebound. On the official side, despite a seemingly much more placid funding environment, “selling UST’s” continued in March if at a reduced pace. The net change in official holdings of treasury securities was -$18.3 billion, better than the -$40.2 billion in February and -$56.3 billion in January but not fundamentally different. The official sector has been net negative in UST’s for ten consecutive months and 15 out of the past 16 under the “rising dollar.”

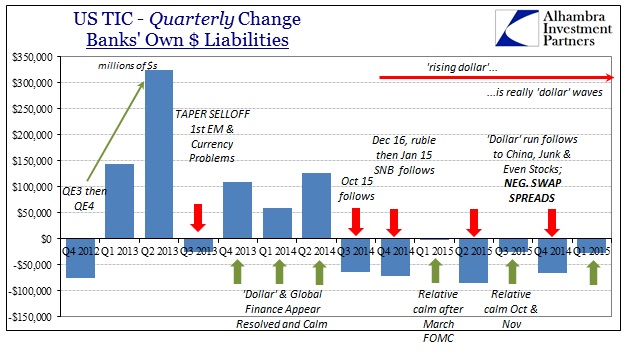

Collectively it suggests that though the liquidations ended, the “rising dollar”, really the manifestation of the heightened decay in the global eurodollar system, did not. We can further observe that process throughout the rest of the TIC data. Starting with reported bank dollar liabilities, for Q1 as a whole the decline was only $26.8 billion as compared to -$66.1 billion in Q4. As usual, the relevant figure for global funding disorder is the quarter before, meaning the lower pace of reduction in Q1 suggests the general calmness of Q2 so far (whereas the much heavier retreat in Q4 2015 prefigured what we observed in January and early February).

While that gives us an indication of the immediate changes and relative conditions quarter-to-quarter, the longer-term view again remains undisturbed. Banks have been consistently shrinking their dollar liabilities even if the exact timing of it is lumpy and uneven enough to create these discrete and intense “dollar” drains.

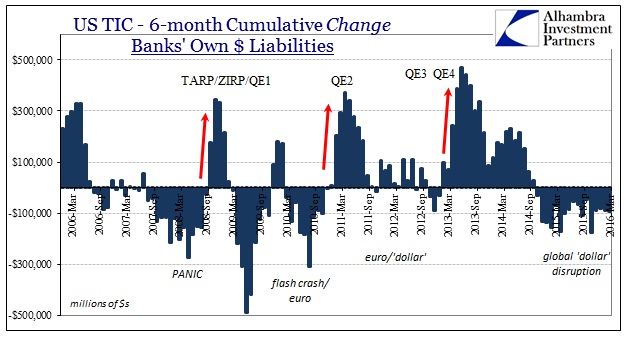

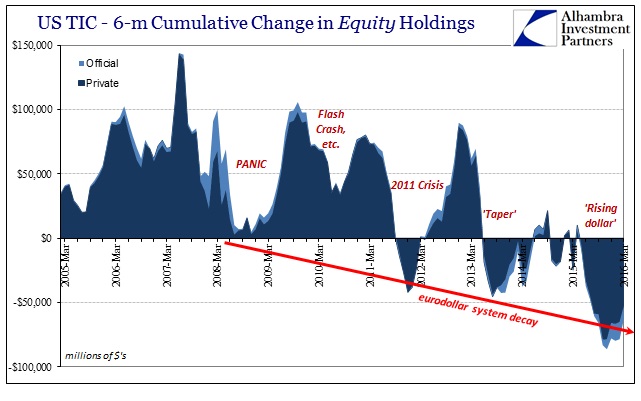

I believe that is also the case for the long-term eurdollar trajectory itself. Going back to 2007 and 2008, the systemic decay has not been at all a straight line but rather a series of variably intense episodes that string together into an overall downward arc. While the focus is usually on UST’s as the primary class of eurodollar proxy, it is by no means limited to them. “Selling equities” follows almost exactly the same crisis/re-crisis trajectory with its familiar increasing intensity with time.

The panic in 2008 was marked not by outright net selling of stocks by foreign holders but instead a much smaller increase in their holdings. The “rising dollar” event by contrast has seen an enormous amount of net selling in sustained fashion. Even in March 2016, with sentiment so favorably shifted positive, both private (-$13.9 billion) and official (-$2.6 billion) sectors were still net sellers of US equities. Tracing back to March 2015, over those thirteen months the private sector of foreign registered accounts disposed of $137 billion in equities in addition to net selling of $18 billion via the official segment. It does seem to offer one part as to why US stocks haven’t seen new highs since.

It suggests that either foreign holders have a very small capacity for volatility (especially in funding) at this end of the eurodollar’s chronology or that they have undergone a paradigm shift in fundamental views on US equity markets (it’s not as if US stocks are cheap). It is also possible that the dramatic selling is a combination where “dollar” funding disruption is being met more consistently via equities than in the past because of a change in outlook for them (and the US economy more generally).

While there wasn’t anything new in the update for March, TIC performs as it usually does with more confirmation of what we had suspected – the continuation of the “rising dollar” as eurodollar flight broken in time only by relative changes in the level of that retreat.