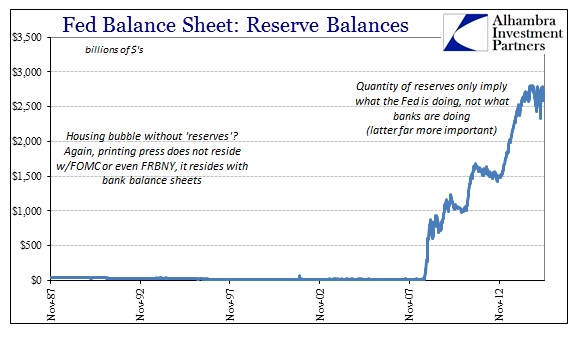

The Federal Reserve under Alan Greenspan and then Ben Bernanke has escaped, largely, responsibility for the panic in 2008 mostly because there is no direct link between monetary policy and the housing bubble. The most stinging criticism that comes out of the era is Greenspan’s “ultra-low” interest rate setting for federal funds, but there is no smoking gun in the form of the “printing press” or bank “reserves.” In fact, bank reserves remain, somehow, the central focus of monetary policy even today when they should be taken for how big a mess the Fed created of the prior bubbles.

There is no printing press in the basement of the Marriner Eccles building or even at the Open Market Desk of FRBNY in NYC. That does not mean, however, that monetary policy is absolved from the center of the biblical expansion of “dollar” reach and debasement (in both definition and scale). When you look at bank reserves, the immediate reaction, often more visceral than cerebral, is that there should be an enormous bout of inflation by now; that was, in fact, the first public and expressed criticisms of the QE’s.

That view of “reserves” conflates what they actually represent. In the operational format alone, reserves are only what the Open Market Desk is doing of monetary policy at that time. In terms of the serial asset bubbles, they represent the onboarding of immense “money dealing” that took place in the latter 1990’s and early and middle 2000’s under the implicit but never-tested promises of monetary policy. In other words, the rise in reserves now was only to make explicit, in arrears, what was expected from bank balance sheets during the bubbles themselves.

In that respect, the increase in reserves post-crisis was not to unleash new inflation, consumer or asset, but rather to enumerate, and only partially, what it took to get past inflation going and maintaining. The Fed was only, through the QE’s, taking belated ownership of that which it implicitly aided of past “dollar” existence. Linking monetary policy to that inflation was not just the federal funds rate, but how that “communication” (as Janet Yellen tells it) was used in actual “money supply” circumstances.

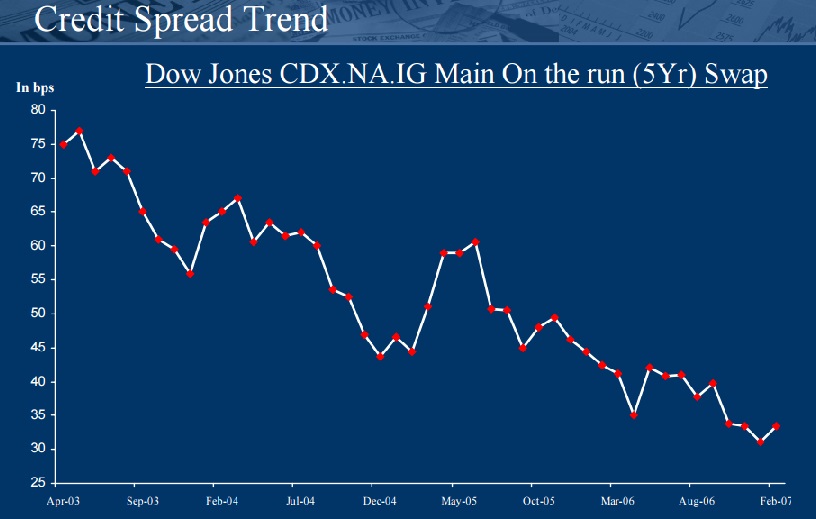

In March 2007, Richard Claiden, CFO of Primus Guaranty, delivered a presentation at the Richmond Fed’s Credit Markets Symposium that showed this monetary linkage in unequivocal detail. Credit spreads on the Dow Jones OTR 5-year CDX had fallen from near 80 bps in early 2003, at the bottom of the dot-com “cycle”, to almost 30 bps by early 2007.

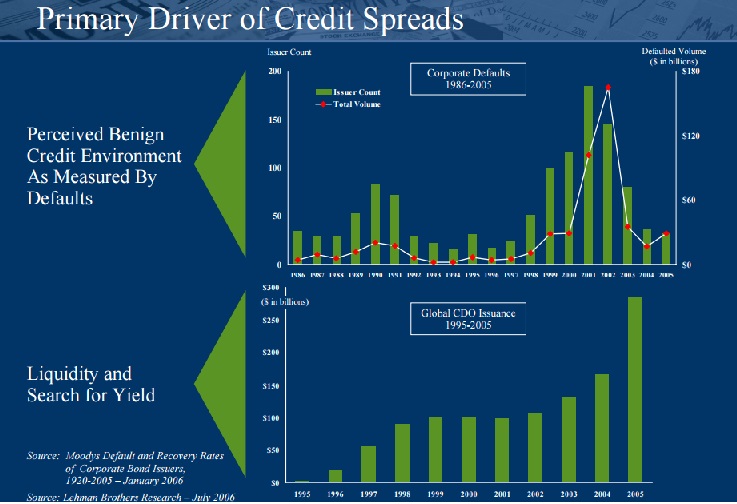

The reason for that massive compression was what is familiar to any financial observer of the post-QE3 environment. Not only did Mr. Claiden refer to a “reach for yield” in March 2007 he also quantified what is perhaps the least appreciated aspect of wholesale monetary influence: clustering defaults.

In the attempt to diminish the influence of the business cycle, the Fed uses monetary policy to influence bank and bond investors with regard to liquidity and risk. One of the major expressions of that is to artificially induce default clusters; there was a massive default wave in the nascent wholesale finance industry out of the dot-coms but then a serious absence of persisting defaults despite a relatively weak recovery thereafter. That disparity is covered by monetary policy influence which, in addition to “reach for yield” via rate repression, keeps many weaker businesses afloat long past the point at which they “should” fail. That isn’t, however, a permanent reduction of what orthodox economics perceives of a negative factor (when in fact it might rather be recognized, rightfully, as necessary creative destruction) only a temporary assuagement of defaults that instead cluster into the next cycle – which happened to be, not by coincidence, much, much bigger.

Mr. Claiden and Primus were no outside observers to this problem, and his firm was expecting an uptick in spreads as mortgage problems grew somewhat more acute. The founder of Primus was the man who practically invented the swap, or at least the standardized version of it that became the bedrock of the entire derivatives industry. In May 2007, Tom Jasper, the CEO who in 1985 launched and became the first co-chairman of ISDA, was “toasting” to wider credit spreads and a much fatter return for Primus. The mortgage problems, he figured, would be grand for Primus’ main business which was writing credit protection.

Because spreads were so thin and had grown thinner throughout Greenspan’s “conundrum”, Primus was forced (in their profit models) to lever up significantly. At the end of 2005, the company, which was a publicly-traded and listed stock, reported a total swaps portfolio of single name entities of $13.4 billion, a 28% increase over the end of 2004. That $13.4 billion came upon a base of just $69 million in cash and $560 million in available-for-sale securities. That was 21x leverage.

By the time Bear Stearns had failed, Primus had $24.3 billion in swaps and just $774 million in cash and assets; or 31x leverage. Since Primus only sold protection on “high quality” companies, in other words those with the highest ratings, there was little perceived risk even with spreads thought to be rising in 2007. In fact, a good proportion of the protection was written against financial firms, meaning the largest banks including Lehman. As you would expect, the firm nearly went bankrupt by October 2008 and the panic, but survived long enough to be finally and fully unwound last year (again, models and math that were no match for reality). Mr. Jasper left the firm in 2010.

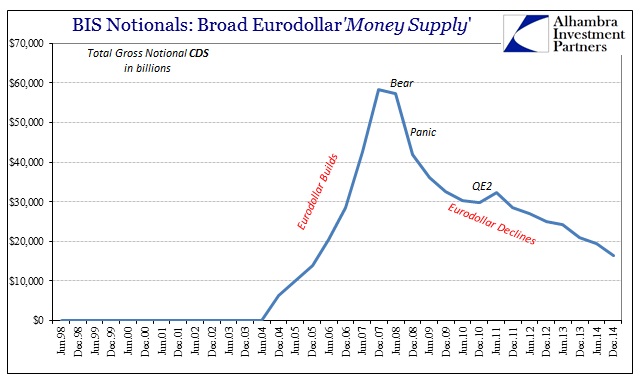

While the current state of Primus’ liquidation gives us another anecdote about the eurodollar decay post-crisis, it was its buildup that turned monetary policy into actual money supply as it is/was understood and used in the eurodollar/wholesale model. Those credit default swaps that Primus was supplying at dirt cheap spreads allowed, artificially and mistakenly, other financial firms and banks to reduce risk in their credit portfolios – at least that was the way it was calculated in their models which translated directly into real financial power or what passes for money these days. That meant those firms, through the “supply” of risk absorption provided by Primus and others, could invest, warehouse and hold much more in terms of par and notional credit for a given “capital” base – the math became the means by which credit expanded so precipitously, traded as exchanged liabilities often in the form of derivative contracts.

Without that supply, including and especially during the panic, the Fed has been forced to take over money dealing more directly, turning out numerical bank reserves in place of what was before just unspecified and held off-balance sheet, but very real, balance sheet capacity. The more the Fed suppressed via its interest rate measure, the more leverage firms like Primus had to supply to be profitable (or as profitable as their models demanded) – at the end of 2005, that 28% increase in the swap portfolio was how the firm increased ROE to 15%. If spreads had been more in line with actual economic reality, Primus may not have “needed” to use as much leverage and the “supply” of risk absorption capacity may have instead been itself reduced, halting even somewhat the massive expansion of subprime and others (since Primus was offering a great deal of swaps on financial firms, especially the bigger banks, those CDS were likely used as hedges against credit structures, including subprime, that were offered/sponsored by those very same firms; in other words, there is a great likelihood that Primus risk capacity was directly related to the subprime mortgage blowout, both up and then down).

Nobody apparently learned much from the whole bubble-bust affair as banks and financial firms are at it again, this time in corporate debt. The artificial suppression of default, in no small part to perceptions of those bank reserves under QE (just like perceptions of balance sheet capacity pre-crisis), has turned junk debt into the vehicle of choice for yet another cycle of “reach for yield.” The supply, this time, is far less of the eurodollar variety and more through mutual funds – less banking, more personal sector. That may sound somewhat more comforting except that it is the weakened, perhaps fatally, eurodollar state that is, in the end, expected to support the whole corporate morass when the default cycle inevitably runs its course and the artificial cluster reappears. As retail investors might likely flee against expectations they never apparently conceived but should have given recent history, there won’t be much, if any, balance sheet capacity to boost appetites toward an orderly transition.

In the past two bubble cycles, we see how monetary policy creates the conditions for them but also in parallel for their disorderly closure. It isn’t money that the FOMC directs but rather unrealistic, to the extreme, expectations and extrapolations. Once those become encoded in financial equations, the illusion becomes real supply. In that way, it appears as if central banks hold great power but little responsibility. The pathology, however, is there and apparent to any and all inquiry. All that is required is a contemporary frame of reference, including what and where the printing press is and resides.