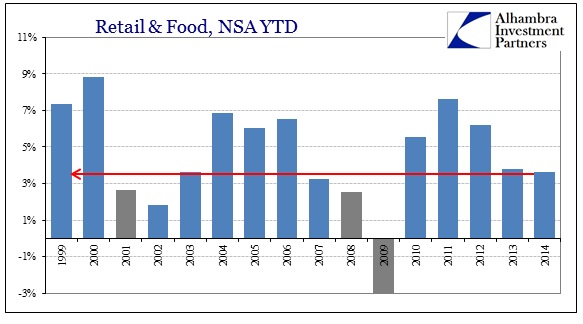

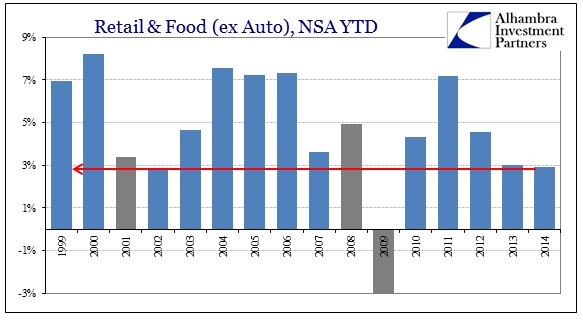

The orthodox notion of monetary policy, following its Keynesian root, is that spending for the sake of spending will lead to a healthy economy. It does not matter, to this philosophy, how or why that spending takes place; only that it does. If, for example, the Federal Reserve can “stimulate” the interest rate sensitive sectors of the economy, like automobiles, they would fully expect that doing so will create a virtuous circle by which the economy is “pushed” thereby to bigger and better things (to its potential and even above, in the orthodox vernacular). The funny thing about analyzing the economy in the past few years is that auto sales are indeed about the only place where monetarism is actually stamping its intended imprint. In September, according to this morning’s retail sales figures, auto sales were an astounding 13.8% above September 2013, continuing a pattern of sales that extends back for quite some time (whether or not these actual vehicles are being sold or leased). There are, of course, a few factors included in that sales growth but there can be no doubt about the monetary effect of financialism. If economic theory is then correct, and auto sales are not some small and unimportant facet of the economy, then that robust spending should be creating widespread downstream benefits. If the Fed has been “successful” at triggering the spending impulse, particularly with credit at the center of it, then such “pump priming” will be inarguably visible in more than just that one sector. Of course, that is not the case as we are still talking about a “recovery” almost five and a half years into one. Clearly orthodox theory about spending for the sake of spending is deficient in a great many ways, but none so clear as in retail sales.  Even with autos forming an increasing proportion of spending, overall retail sales have failed to return to anything resembling “potential”; in fact retail sales are actually moving in the “wrong” direction despite the credit injection of monetarism through that channel. This becomes very clear once you remove autos from the historical track of retail sales.

Even with autos forming an increasing proportion of spending, overall retail sales have failed to return to anything resembling “potential”; in fact retail sales are actually moving in the “wrong” direction despite the credit injection of monetarism through that channel. This becomes very clear once you remove autos from the historical track of retail sales.  Year-to-date in 2014, despite all the promises of a rebound, overall activity is pacing less than last year, putting the economy on track for the second worst year of this millennium (a rather dubious distinction). That YTD sales are quite far behind even 2008 shows both that auto sales were actually a primary catalyst in the Great Recession and that prices also play a significant part. That leaves the economy in 2014 as being recessionary in everything but autos, totally upending the idea that spending for the sake of spending leads to anything like a full recovery and sustainable growth. Rather, such redistribution typically comes at the expense of something else, which is worse than it sounds (a zero sum game would be an improvement). Some of the highest growth areas, such as online shopping, have suddenly become far less so.

Year-to-date in 2014, despite all the promises of a rebound, overall activity is pacing less than last year, putting the economy on track for the second worst year of this millennium (a rather dubious distinction). That YTD sales are quite far behind even 2008 shows both that auto sales were actually a primary catalyst in the Great Recession and that prices also play a significant part. That leaves the economy in 2014 as being recessionary in everything but autos, totally upending the idea that spending for the sake of spending leads to anything like a full recovery and sustainable growth. Rather, such redistribution typically comes at the expense of something else, which is worse than it sounds (a zero sum game would be an improvement). Some of the highest growth areas, such as online shopping, have suddenly become far less so.

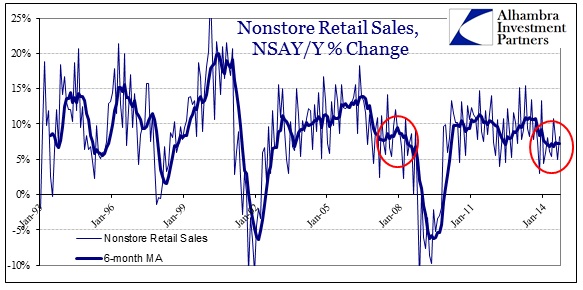

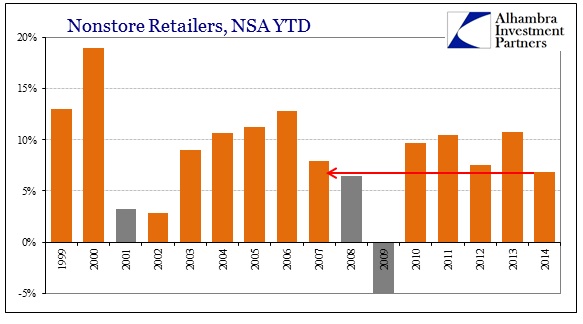

With no ready weather explanation to impact shopping from home, there isn’t any good excuse for seeing nonstore retail growth at about the same pace as 2008, far less than 2013. In truth, however, that is actually quite typical as the pace of spending and activity, as I said above, continues to be deficient in everything but autos.

With no ready weather explanation to impact shopping from home, there isn’t any good excuse for seeing nonstore retail growth at about the same pace as 2008, far less than 2013. In truth, however, that is actually quite typical as the pace of spending and activity, as I said above, continues to be deficient in everything but autos.  That spending has not picked up through the entire “back to school” season is once again alarming. Recall last year that such “unexpected” weakness led to the worst retail shopping season since 2009, and then the disaster in Q1. Apart from whatever anyone ultimately thinks about last winter, the last six months of this year are pretty similar to the same six months in 2013 heading into that holiday period.

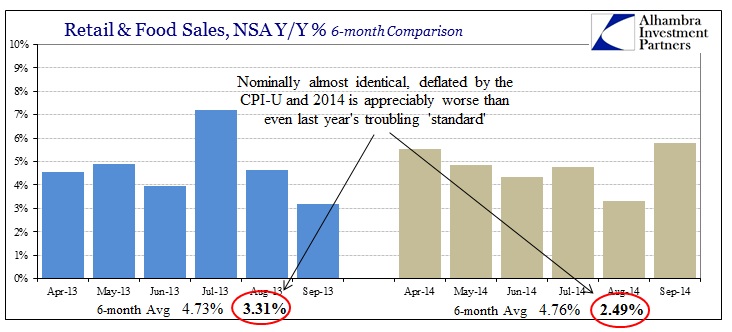

That spending has not picked up through the entire “back to school” season is once again alarming. Recall last year that such “unexpected” weakness led to the worst retail shopping season since 2009, and then the disaster in Q1. Apart from whatever anyone ultimately thinks about last winter, the last six months of this year are pretty similar to the same six months in 2013 heading into that holiday period.  On a nominal basis, the growth rates are almost identical but the price environment is not (this is not to say that the orthodox idea of “inflation” is present, only that price changes are likely more stinging this year than last). So where this economy in this year is supposed to be in a rebound, it isn’t even doing so at a rate that would match last year’s setup to begin with. And since the figures above include auto sales, it would be more than fair to say that both orthodox ideas about prices and generic spending holding some sort of beneficial driver in them is flat out false.

On a nominal basis, the growth rates are almost identical but the price environment is not (this is not to say that the orthodox idea of “inflation” is present, only that price changes are likely more stinging this year than last). So where this economy in this year is supposed to be in a rebound, it isn’t even doing so at a rate that would match last year’s setup to begin with. And since the figures above include auto sales, it would be more than fair to say that both orthodox ideas about prices and generic spending holding some sort of beneficial driver in them is flat out false.  Ex autos, retail sales are barely growing at all taking into account at least some measure of price increases. In that respect, the precipitous decline in oil and energy might provide some actual relief, as such “deflation” would be very welcome if it didn’t presage worse economic conditions. To that end, it is wages and earned income, the building blocks of actual wealth, that is conspicuously absent from all of this. Given that the mainstream view on jobs and labor, which colors almost all commentary about the economy, does not align with what we see here, that presents a bit of a problem. It was only yesterday where San Francisco Fed President John Williams asserted a need for both more inflation and wages in order to prevent (my words) still more QE deterioration (my words), only to see oil prices tumble significantly and now retail sales generally disappoint. That means the economy is already failing his “standards” on both accounts, as we can assume that spending and wages are closely related – deficiency in spending would reasonably suggest continued, ongoing and unsolved deficiency in wages.

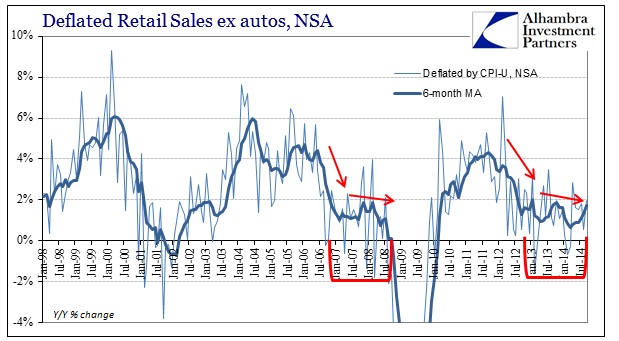

Ex autos, retail sales are barely growing at all taking into account at least some measure of price increases. In that respect, the precipitous decline in oil and energy might provide some actual relief, as such “deflation” would be very welcome if it didn’t presage worse economic conditions. To that end, it is wages and earned income, the building blocks of actual wealth, that is conspicuously absent from all of this. Given that the mainstream view on jobs and labor, which colors almost all commentary about the economy, does not align with what we see here, that presents a bit of a problem. It was only yesterday where San Francisco Fed President John Williams asserted a need for both more inflation and wages in order to prevent (my words) still more QE deterioration (my words), only to see oil prices tumble significantly and now retail sales generally disappoint. That means the economy is already failing his “standards” on both accounts, as we can assume that spending and wages are closely related – deficiency in spending would reasonably suggest continued, ongoing and unsolved deficiency in wages.  Some of the reason for that is, again, the effect of redistribution which covers and misdirects a lot of economic function. What looks like growth is actually not, instead offering erosion that is not always immediately recognized. Simply deflating retail sales by the CPI (an ill-suited measurement, so make of it what you will, but there isn’t anything better) shows this in better regard.

Some of the reason for that is, again, the effect of redistribution which covers and misdirects a lot of economic function. What looks like growth is actually not, instead offering erosion that is not always immediately recognized. Simply deflating retail sales by the CPI (an ill-suited measurement, so make of it what you will, but there isn’t anything better) shows this in better regard.  And it is here where the trend is most concerning, particularly as it relates to the prior “cycle” peak. Despite all the monetary efforts toward “inflation” and spending via auto debt accumulation, consumer activity continues to move in the wrong direction. Maybe the middle of 2014 was better than its initial months, but that says nothing about where this is all headed; just another minor gyration on a trajectory eroded by constant appeals to redistribution.

And it is here where the trend is most concerning, particularly as it relates to the prior “cycle” peak. Despite all the monetary efforts toward “inflation” and spending via auto debt accumulation, consumer activity continues to move in the wrong direction. Maybe the middle of 2014 was better than its initial months, but that says nothing about where this is all headed; just another minor gyration on a trajectory eroded by constant appeals to redistribution.

Inside Retail Ex-Debt Fueled Autos—-2nd Weakest Year This Century