by Joshua M Brown at The Reformed Broker

Why were the inflation hawks so wrong about quantitative easing? Why didn’t all the “money printing” lead to commodity prices skyrocketing?

One answer is that, while bank reserves were boosted, lending didn’t take off and there was no uptick in the velocity of money – the speed at which capital zooms through the economy and turns over. Absent velocity of money, QE could be looked at as either ineffective or actually causing a deflationary environment, where capital is hoarded and everyone is too petrified to risk it on productive endeavors.

Christopher Wood (CLSA) explains further in his new GREED & fear note:

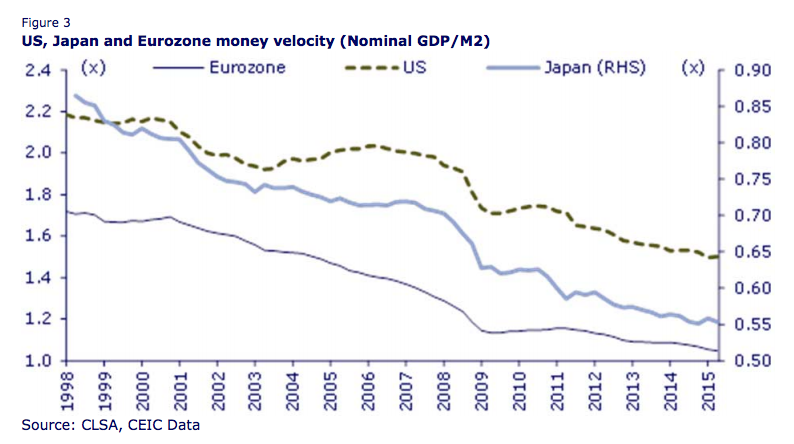

To GREED & fear the best way to illustrate that quantitative easing is not working is the continuing decline in velocity and the resulting lack of a credit multiplier since the unorthodox monetary regime was introduced. In America, Japan and the Eurozone velocity has continued to decline since the financial crisis in 2008. Thus, US, Japan and Eurozone money velocity, measured as the nominal GDP to M2 ratio, has declined from 1.94x, 0.7x and 1.29x respectively in 1Q98 to 1.5x, 0.55x and 1.05x in 2Q15 (see Figure 3). Indeed, US money velocity is now at a six-decade low. This is why those who have predicted a surge in inflation in recent years caused by the Fed “printing money” have so far been proven wrong. For inflation, as defined by conventional economists like Bernanke in the narrow sense of consumer prices and the like, will not pick up unless the turnover of money increases. This is the problem with the narrow form of mechanical monetarism associated with the likes of American economist Milton Friedman.

Wood goes on to make the point that QE is deflationary because it shrinks net interest margins for banks via depressing treasury bond yields. It also enriches the already wealthy via asset price inflation but they do not raise their consumption in response, because how much more shit can they possibly buy? Finally, it leads to a preference of share buybacks vs investment spending because the payback from financial engineering is so much easier and more immediate.

Source:

False Courage

CLSA – October 8th 2015