The world cheered this morning’s trade estimates from China, as both exports and imports rebounded from a dismal start to the year. Exports rose 11.5% in March after falling 25% in February; imports fell “only” 7.6% after declining 13.8% the month before. Despite the difficulties with data calculations around the Lunar New Year, economists were quick with their usual glowing reviews any time a plus sign appears:

“China’s trade data for March point to healthy growth in import volumes and add to growing evidence that the extreme gloom of a few weeks ago about the domestic economy was misplaced,” said Marcel Thieliant and Mark Williams at Capital Economics.

And:

“In a way, it [the data] isn’t surprising given the base effect. But also, the authorities have been stimulating the economy quite significantly—all the interest rate and reserve ratio requirement (RRR) cuts—so we are seeing improvement and some stabilization,” said Jonathan Pain, author of investment newsletter The Pain Report.

Only the Wall Street Journal (surprisingly again) had a more balanced take, describing more restraint than optimism.

Economists cautioned that the export boost, after months of decreases, in part reflects a seasonal upturn after the Lunar New Year holiday in February and isn’t likely to be sustained given tepid global demand. Exports last month also benefited from a weak year-earlier performance that made comparative results look stronger.

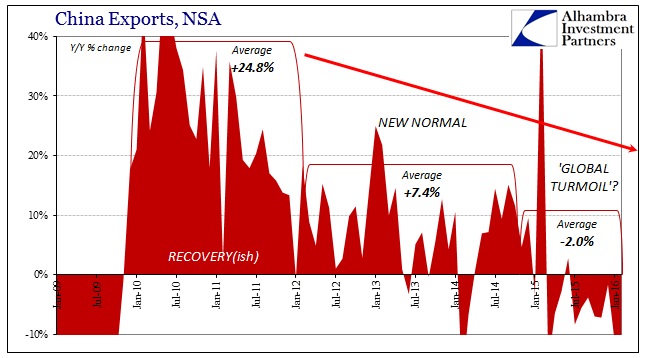

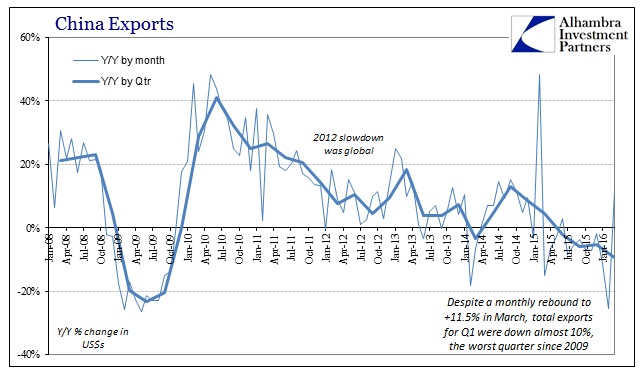

Despite the return in export growth, which isn’t actually unusual, total exports for the whole first quarter were down almost 10%. That is the worst quarterly performance for the extremely important export sector since 2009 and the global Great Recession. That contraction was nearly twice the rate of Q4 and Q3 2015, indicating that the global economy really is getting worse (maybe something more strongly negative than “tepid” in terms of “global demand”).

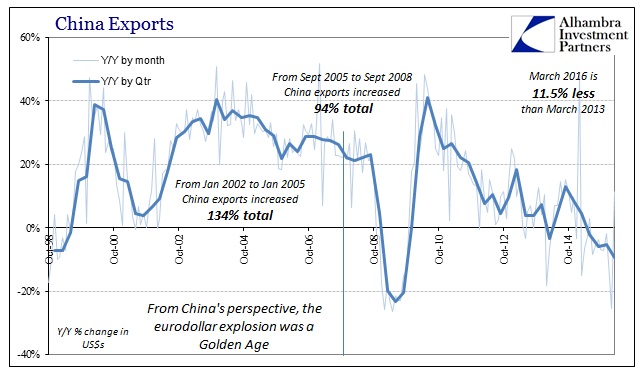

Even if there was improvement in March 2016, that is only in a small and largely irrelevant comparison. As I write month after month, China’s industrial economy was built to service rapid growth not variable shrinking. Despite that 11.5% gain over March 2015, the export total was still an enormous 11.5% below total exports of March 2013. It is a matter of volume (especially dollar volume) as well as time. The Chinese economic baseline and capacity (including capex and investment) is predicated on 20-30% expansion consistently, not 11.5% above last year which was 15% below the year before that. That trend isn’t growth but uneven, durable contraction.

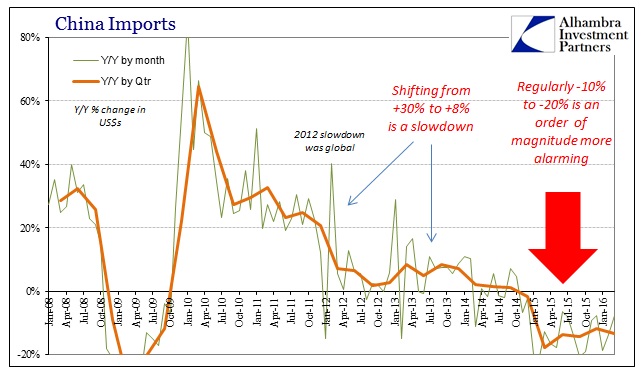

On the import side, the “improvement” was not just less spectacular for mainstream narratives it may not have been real at all. As has occurred before, total imports were boosted by a suspicious surge in “trade” reported from Hong Kong. Calculated trade coming from the city surged 116% in March after rising 89% in January/February combined. It does not suggest actual activity but rather some high degree of further fake invoicing to avoid capital controls.

Setting aside objections to Hong Kong irregularity, imports for Q1 as a whole fell 13.3%, a further decline from Q4’s -11.8% and right within the sustained contraction that started with Q1 last year. Again, monthly variation misses the real trend and relevant interpretation. The slowdown remains as consistent as ever in terms of the big picture.

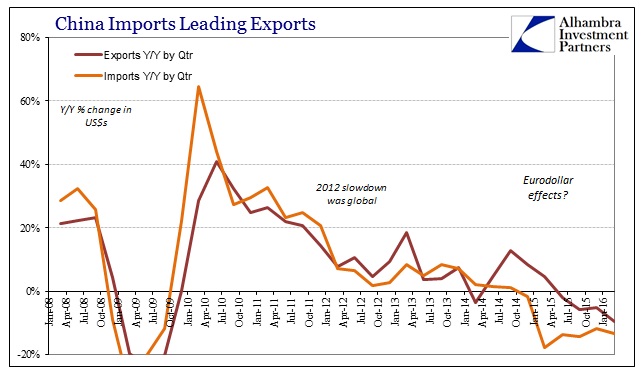

Removing the monthly numbers displays the uniformity on both sides of the Chinese trade function. Imports remain steadily contracting while exports seem intent on joining them. In other words, the global economy is still grappling with the next stage (“global turmoil”) of the ongoing slowdown.