In August 2014, Chinese industrial production was estimated to have slowed sharply from +9.0% that July to just 6.9%. Consensus at the time expected only a minor variation, an insignificant change to +8.8%. Chinese industrial statistics had suggested some minor (relatively speaking) weakness at the start of the year before rebounding throughout the spring in what is now, in the third consecutive year of it, a familiar pattern. The drop into the heat of August was a complete surprise for the more confident extrapolations that 2014 China would be right back on track, or at least moving appreciably close to it. As the Wall Street Journal reported at the time:

Economists said the sharp deceleration in industrial output, along with weaker fixed-asset investment, retail and real estate sales data, is likely to rattle regional stock markets Monday as Beijing struggles to reach its annual 7.5% economic-growth target in a nation where hitting benchmarks remains important.

“This figure is a bit shocking,” said ANZ economist Liu Li-Gang. “If we have another month of low IP growth, the third-quarter GDP figure could be at most 7%.”

Thus, the narrative of the “soft landing” in China was born over the next few months where economic statistics weren’t nearly as bad as August, but also didn’t indicate Chinese resurgence. Since the mainstream is programmed to view the Chinese economy as if it were almost totally command and control, the sudden and “shocking” slowdown must have been a communist directive.

There is, of course, some truth to the idea as the notion of reform had gained political acceptance in late 2013. Under new leadership, China was to stop prioritizing growth at all costs, returning more modestly toward its ideological roots. But even that intention can be misleading, as the nature of China’s slowdown is not truly Chinese; the purpose of reform is really about how the nation’s political and monetary authorities will manage what is really a global economic slowdown driven by monetary factors that China only knows too well and too personally.

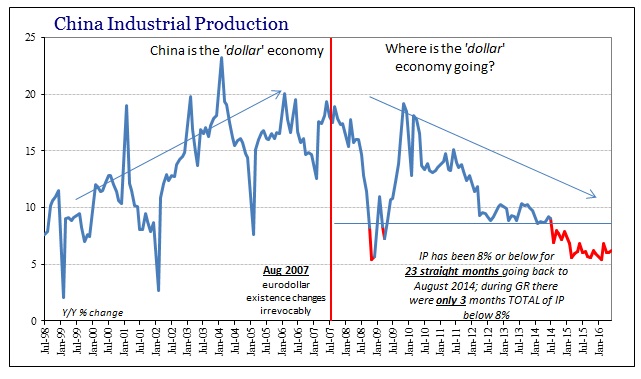

The eurodollar system in its outward (from the domestic dollar perspective) more global capacity is far more like actual money than our own experience of it. We know its inward effects via overwrought financialism of the housing bubble, but its related and parallel expansion into EM’s in particular was to finance trade and productive capacity. Its decay, then, is more readily consistent with expected money behavior; a fact that we can observe from none other than Chinese industrial production.

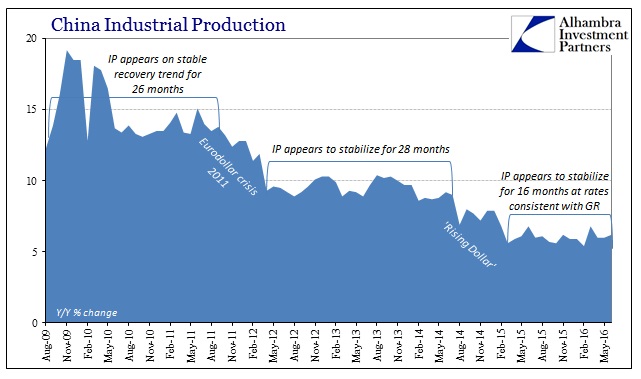

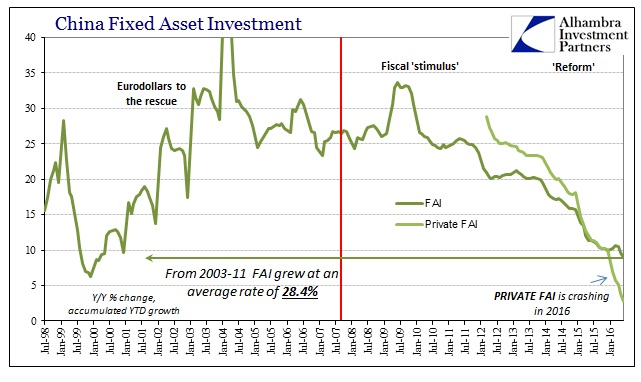

From the middle of 2009 until the middle of 2011, the last actual hope of eurodollar restoration, Chinese industrial production appeared to project a full recovery as if the Great Recession were an actual if severe recession. The interruption in eurodollar flow due to the events starting, of course, in the summer of 2011, downshifted IP as a reflection of China’s external economic orientation. China responded, as it had up to that point, with massive “stimulus” that increased its ghost capacity (in literal ghost malls and even cities) with the idea that the slowdown into 2012 would also be temporary. This was not just a Chinese view, it was uniformly shared by dominant orthodox expectations especially of global “stimulus” then underway or being further planned.

That defined the narrative over the next 28 months or so, as economists kept expecting the 2012 slowdown trend to at some point dissipate into once more full recovery like 2010 and early 2011. That was the mainstream baseline for commentary all the way into 2014; no talk of “soft landing” or China’s newfound preference for its “consumer economy”, only expectations for eventual full recovery of the pre-crisis, industrial/export status quo. After all, by 2014, the US economy was believed, wrongly, to be so close to achieving exactly that, along with the European economy under more aggressive explicitness to Mario Draghi’s promise.

Like the 2011 eurodollar crisis, however, the “rising dollar” strangulation of global trade “money” ended any such hopes. The result was another obvious downshift in Chinese industrial activity coincident to further slowing in the global economy. Giving up on the idea of full recovery, again “soft landing” has now taken its place as the most charitable and benign explanation that preserves at least the possibility of orthodox favor.

That is why even the smallest of monthly variation in economic accounts is cheered, as it represents the idea, the possibility that the “soft landing” isn’t just wishful thinking forced upon “shocked” economists and policymakers by events far beyond their control. Today’s update for June 2016 has been, in many places, received in exactly that fashion. Chinese industrial production was 6.2% in June, slightly better than the 6% recorded for the two months prior and still up from the 5.4% in February.

It is that last comparison that is being most asserted, though it once again misses the point; there is, in China especially, no difference between 5.4% IP and 6.2%; or 10.6% in retail sales for June 2016 compared to the multi-year low of 10% in May. They are all the same disaster that is elongated and uneven such that the mainstream either doesn’t notice or when they do are very confused by it; the proverbial boiling frog. This is not to say that the Chinese haven’t, however, as there is even more indication that China is both in deeper trouble economically as well as that Chinese authorities are panicking in response.

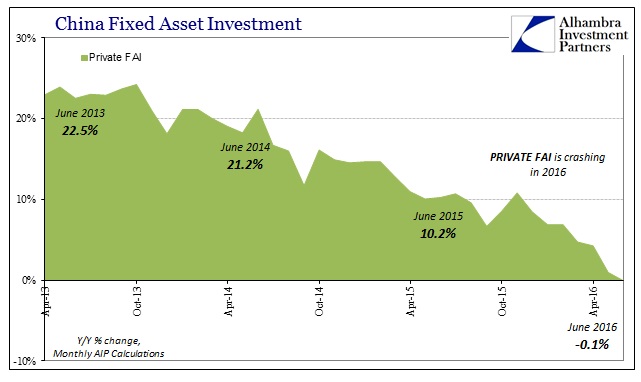

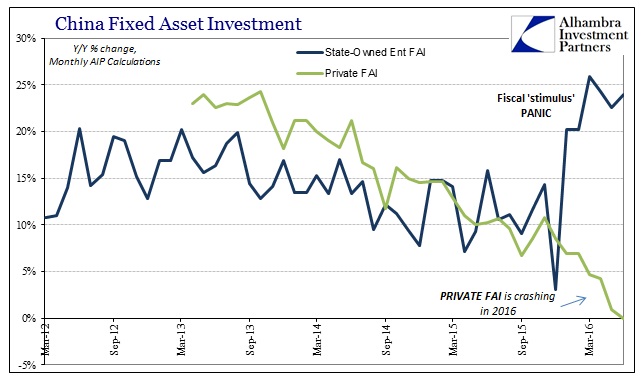

Setting aside the fantasy narrative of the “consumer economy”, the baseline for China’s actual economy is and has been determined by investment or capex. That is Fixed Asset Investment (FAI) but more importantly private fixed asset investment. As noted a few months ago, the whole urbanization trend and modernizing of the Chinese economy is predicated on private FAI; it is crashing in 2016.

The National Bureau of Statistics reports FAI on an accumulated year-to-date basis, but it doesn’t take much math to convert to monthly statistics. According to my calculations for June, private FAI actually contracted, though just barely. It is still, however, a shocking development where weakness in the Chinese economy rarely finds a negative number.

It further suggests what we have suspected all along, namely that the events starting last summer were in monetary terms a heightened period of disruption that caused significant economic damage particularly in places most susceptible to the eurodollar system as money supply – China being a primary example. The monetary suffocation would have permanent effects, including the forgoing of building new capacity as a reflection of being forced to deal with the reality of the global economy as it is, not as it is described by economists.

The second wave of disruption (which may really be just the second instance of the same that started last July) building in November and cresting into January and February clearly affected Chinese political thinking; at the start of 2016, the Chinese suddenly unleashed fiscal and monetary “stimulus” though being channeled almost exclusively through state-owned banks (via targeted PBOC liquidity) and into the big state-owned enterprises (SOE).

Economists, as usual, take this is a positive sign that Chinese authorities have broken out of their reluctance of the past few years; coming to their senses, as the orthodoxy would see it. That view misses the true comparison – that private FAI only gets worse despite the bump in “stimulus”, meaning that Chinese capacity is no longer correlated with policy efforts as it had been in the past. Further, despite the jump in fiscal “offsets”, they aren’t nearly enough to actually offset; private FAI is decelerating and actually falling now more than FAI through SOE’s is rising (private FAI is a little less than twice SOE FAI).

These are not the responses of top-down commands feeling full in control smoothly executing the preferred “soft landing”, they are the panicked reactions to global economic and monetary inputs that already demonstrated real and further danger. China’s economy, as a reflection of the global economy, is in real trouble especially as there is no end in sight to the continued slowdown whether or not it ever achieves a cyclical determination (which is, at this point, quite immaterial). In short, the Chinese are using the most inefficient and wasteful avenue possible, the very realization that brought about reform in the first place, to suddenly try to offset the true economic baseline as it screeches to a halt and threatens now to actually contract – an actual negative number in the one part of the economy China can least afford it.

From that perspective, industrial production, retail sales, or even GDP are not collective cause for relief, they are still further confirmation of the worst. In other words, unless “stimulus” can suddenly boost IP, retail sales or whatever to at least double if not triple their current rates and quickly, Chinese economic capacity will not be able to overcome monetary strangulation; nor might anyone even be willing to try. Soft landing was always nothing more than mutated(ing) fiction.