The federal funds rate holds no relevance to anything actually useful and meaningful. That has been the case for some time, though pinning down exactly when federal funds became irrelevant is a bit of chore (I personally view it when altering Regulation M in 1990 created a regulatory par with eurodollars). Even the FOMC admits how actual finance has passed by the federal funds rate, an interbank market that traces itself to 1920 when money was money.

Back in 2011, two Federal Reserve economists presented a paper at an ECB conference that suggested, rather strongly, the Fed at least consider shifting away from a federal funds target to targeting instead the general collateral repo rate (though in the years since, the paper seems to have been scrubbed from all official channels, including the ECB where it began). Titled, A target Treasury general collateral repo rate: Is a target repo rate a viable alternative to the target federal funds rate?, authors Elizabeth Klee and Viktors Stebunovs put forth several quite convincing arguments for a change, starting from, of course, the relevant premise that there was nobody left in federal funds. It was actually a significant topic for discussion in Yellen’s first few months as Chair, including some wandering references in her first Humphrey-Hawkins testimony in February 2014 and pointed comments from other FOMC members.

“It’s my opinion that the fed funds rate is not the right tool going forward,” Dallas Fed President Richard Fisher told reporters. “I’d like to keep it in the toolkit,” he added. “But we’ve been working with several other tools” such as term repurchase programs, overnight reverse repos, and interest on excess reserves.

At the July 2014 FOMC meeting, the minutes indicated more than a little reservation about acting on federal funds as the face of monetary policy.

Almost all participants agreed that it would be appropriate to retain the federal funds rate as the key policy rate, and they supported continuing to target a range of 25 basis points for this rate at the time of liftoff and for some time thereafter. However, one participant preferred to use the range for the federal funds rate as a communication tool rather than as a hard target, and another preferred that policy communications during the normalization period focus on the rate of interest on excess reserves (IOER) and the ON RRP rate in addition to the federal funds rate. Participants agreed that adjustments in the IOER rate would be the primary tool used to move the federal funds rate into its target range and influence other money market rates. In addition, most thought that temporary use of a limited-scale ON RRP facility would help set a firmer floor under money market interest rates during normalization. Most participants anticipated that, at least initially, the IOER rate would be set at the top of the target range for the federal funds rate, and the ON RRP rate would be set at the bottom of the federal funds target range. Alternatively, some participants suggested the ON RRP rate could be set below the bottom of the federal funds target range, judging that it might be possible to begin the normalization process with minimal or no reliance on an ON RRP facility and increase its role only if necessary. However, many other participants thought that such a strategy might result in insufficient control of money market rates at liftoff, which could cause confusion about the likely path of monetary policy or raise questions about the Committee’s ability to implement policy effectively.

As last year wore on, the Fed did test various methods of “controlling” short-term rates in money markets with little actual success. The reverse repo program (RRP) noted above with such confidence turned out to be a massive and proven disappointment. Instead, the FOMC has ramped testing of something called the Term Deposit Facility (TDF) which, since it was conspicuously absent from that July 2014 discussion, tells you all you need to know about the ad hoc nature of the assumed eventual exit from ZIRP. There isn’t much said about the TDF anymore, either. One month the RRP will take care of much, the next they slip in a TDF, downplay all further references to and expectations for them and call it good.

Given that they don’t know what they are doing, a furthered position by all that testing, that the federal funds rate remains the focus is unsurprising – what else is left? After all, monetary policy holds nothing for money, having been shorn and devolved into the financial equivalent for pop psychology. I wrote just about a year ago:

The FOMC well knows that if they just ignored this evolved complication and simply raised the federal funds rate alone that precisely nothing would happen – at least nothing that looked like a rate increase. So they have developed, in theory, some tools by which to augment the main policy “lever.” If you read their current thoughts and literature on the subject, policymakers understand (a loose term here) this complication but do not want to totally remove themselves from the federal funds rate because it conforms best to widespread understanding about what the committee wants to convey. If that doesn’t prove how much monetary policy has devolved to nothing but psychology and rational expectations theory, then nothing will.

In other words, the federal funds rate will remain as the primary target mechanism for “signaling” policy intent, but the other programs will be taken in conjunction for actual liquidity and “reserve” variance. You can see why they run into problems right from the start.

From that point alone, you can appreciate why the FOMC so panicked immediately after their September inaction; not raising the meaningless federal funds rate had no impact on money markets but on more basic perceptions of the recovery and economy; or at least perceived confirmation that even the economists at the FOMC finally get the discrepancy between the economy they have been suggesting for a long time and the growing unnerve and disavowal in credit and actual (as opposed to pretend where the FOMC wants to remain) funding markets.

On cue, FRBNY’s Bill Dudley essentially admitted their so intention:

“If we begin to raise interest rates, that’s a good thing. That’s not a bad thing,” he said during a question and answer session after his opening remarks, which were on financial regulation. “That’s a sign that the economy is actually returning to health, the Federal Reserve is getting closer to achieving our dual mandate objectives of maximum sustainable employment and price stability.”

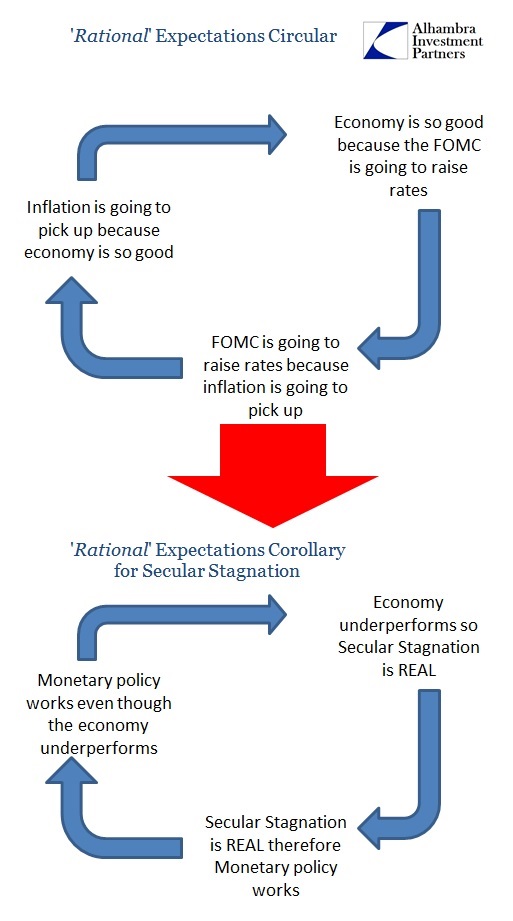

All of which brings us back to the very heart of modern monetarism; the circular logic behind it all that “somehow” is defeated, every time, by “unexpected” reality. You can understand why Janet Yellen’s Doctrine is so shifted toward investors and market agents acting, by her stated preference, almost unconsciously; if everyone just followed Yellen’s direction without reservation the world would be a perfect place.

And so it is in that context that all this makes perfect sense; the Federal Reserve will target a money rate that nobody uses in order to project a story in which nobody believes so that economists can call this stunted, decrepit recovery a full one. If only I were making this all up.