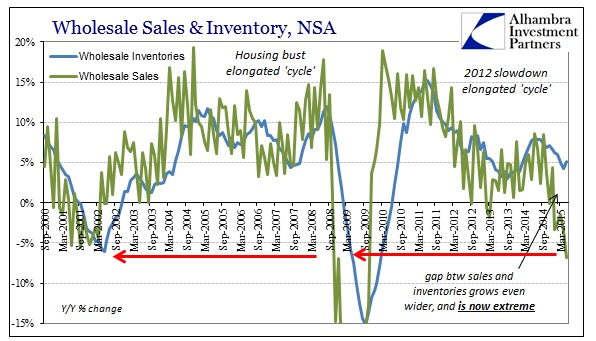

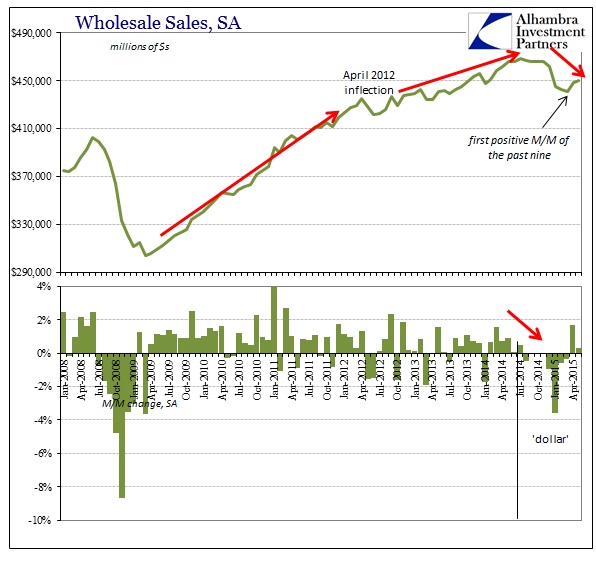

May must have been the month of sevens. First, exports declined by 7% year-over-year, as did imports. Now the Commerce Department reports wholesale sales within the US fell by 6.8%, which is good enough in close rounding to be yet another seven percent contraction. In the case of wholesale sales, while those estimates are likely coincidence at all around -7%, there actually is a very close relationship between them, inventory, and imports. If inventories had followed the others to contract at 7% then we might be optimistic about the awaited re-alignment of inventory and thus possibly foresee an end to the production slump here and overseas. Instead, inventories grew yet again, this time by nearly 6%!

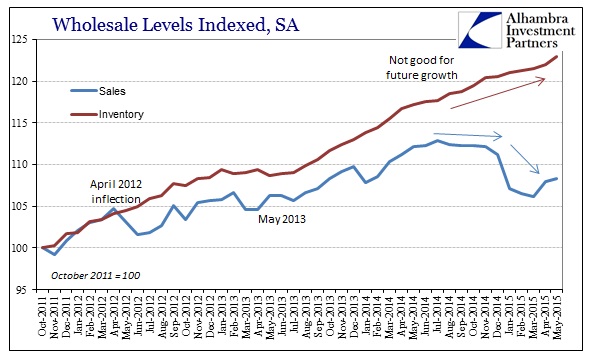

The gap now between sales and inventory has not been this wide since the Great Recession, and only the worst parts of it. A discrepancy of this magnitude cannot last, and the direction of sales will be (has already been) the determinant. In short, what was very ugly so far in 2015 just became a dangerous imbalance.

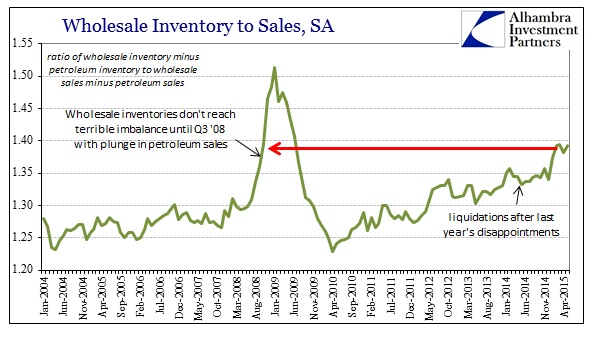

The overall inventory/sales ratio, without petroleum, remains at a seriously elevated level. That more than suggests that this imbalance between somehow continued business optimism and actual “demand” is not just extreme but widespread beyond the energy sector.

Even the seasonally-adjusted sales figures were barely positive in May, coming nowhere close (despite April’s statistical surge) to closing the gap after nine consecutive months of declines.

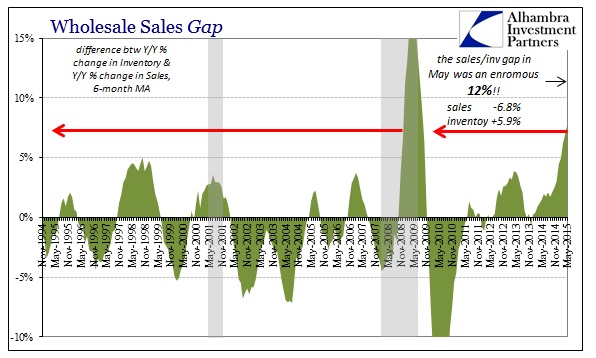

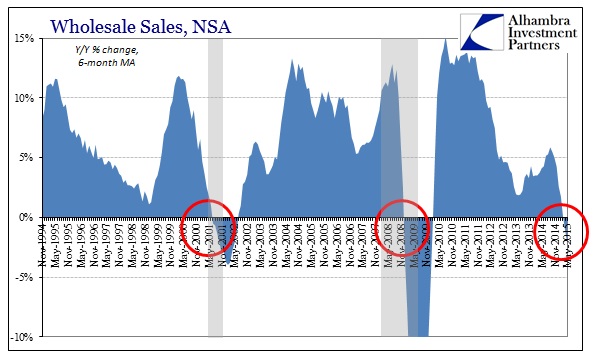

The 6-month average in wholesale sales is now -2.2%, which means not only is the contraction widespread but also far more than a temporary bump or anomaly. To put that protracted decline into perspective, that was about the same average drop as January 2009 right at the start of the implosion phase of the Great Recession; or October 2001 at the end of the dot-com recession. The sales gap is equivalent to December 2008, when sales then fell a similar 7.0% against an inventory gain of 4.3%.

Inventory imbalance this large can only be contractionary, and heavily so, on future production levels. From this central view, really the pivot, between “demand” and supply the US has run into great recessionary pressure. From the production side, we already see serious and unusual weakness which altogether means economic imbalances are far, far beyond the usual “this year was supposed to be great but isn’t.” That means there isn’t yet a bottom in sight for where production may have to fall to equalize against equally declining retail and end demand activity. In fact, that is the problem, as production, given this disparity between sales and inventory, eventually has to drop faster than sales by more than a little.

In short, if the US is not close to recession right now then it has performed an amazing feat of replication and illusion. We are now five months (in terms of data) into 2015 and the numbers keep getting worse, where now the absolute levels (negative) across these “demand” components can no longer be conflated and dismissed or ignored. There is no weather or seasonality here, just unadulterated, broad contraction; one that appears far from over.