By Ambrose Evans-Pritchard at The Telegraph

Credit stress in the European banking system has suddenly turned virulent and begun spreading to Italian, Spanish and Portuguese government debt, reviving fears of the sovereign “doom-loop” that ravaged the region four years ago.

“People are scared. This is very close to a potentially self-fulfilling credit crisis,” said Antonio Guglielmi, head of European banking research at Italy’s Mediobanca.

“We have a major dislocation in the credit markets. Liquidity is totally drained and it is very difficult to exit trades. You can’t find a buyer,” he said.

The perverse result is that investors are “shorting” the equity of bank stocks in order to hedge their positions, making matters worse.

Marc Ostwald, a credit expert at ADM, said the ominous new development is that bank stress has suddenly begun to drive up yields in the former crisis states of southern Europe.

“The doom-loop is rearing its ugly head again,” he said, referring to the vicious cycle in 2011 and 2012 when eurozone banks and states engulfed in each other in a destructive vortex.

It comes just as sovereign wealth funds from the commodity bloc and emerging markets are forced to liquidate foreign assets on a grand scale, either to defend their currencies or to cover spending crises at home.

Mr Ostwald said the Bank of Japan’s failure to gain any traction by cutting interest rates below zero last month was the trigger for the latest crisis, undermining faith in the magic of global central banks. “That was unquestionably the straw that broke the camel’s back. It has created havoc,” he said.

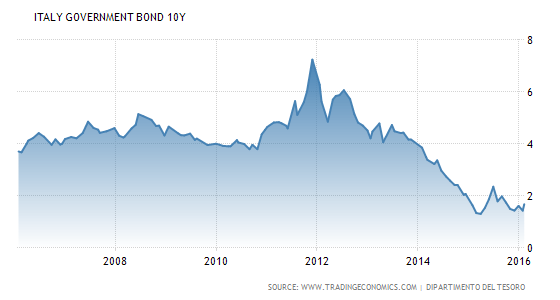

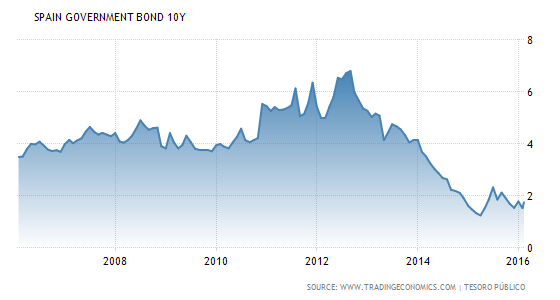

Yield spreads on Italian and Spanish 10-year bonds have jumped to almost 150 basis points over German Bunds, up from 90 last year. Portuguese spreads have surged to 235 as the country’s Left-wing government clashes with Brussels on austerity policies.

While these levels are low by crisis standards, they are rising even though the European Central Bank is buying the debt of these countries in large volumes under quantitative easing. The yield spike is a foretaste of what could happen if and when the ECB ever steps back.

Mr Guglielmi said a key cause of the latest credit seizure is the imposition of a tough new “bail-in” regime for eurozone bank bonds without the crucial elements of an EMU banking union needed make it viable.

“The markets are taking their revenge. They have been over-regulated and now are demanding a sacrificial lamb from the politicians,” he said.

Mr Guglielmi said there is a gnawing fear among global investors that these draconian “bail-ins” may be crystallised as European banks grapple with €1 trillion of non-performing loans. Declared bad debts make up 6.4pc of total loans, compared with 3pc in the US and 2.8pc in the UK.

The bail-in rules were first imposed in Cyprus after the island’s debt crisis, stripping European bank debt of its hallowed status as a pillar of financial stability, and of its implicit guarantee by states. The regime came into force for the whole currency bloc in January. Both senior and junior debt must now face wipeout before taxpayers have to contribute money.

While this makes sense on one level, the eurozone banking structure is now dangerously deformed. Individual eurozone states cannot easily recapitalize their own banking systems because that breaches EU state-aid rules, but there is no functioning European body to replace them.

“The root cause of this debacle is the way the eurozone is designed. We don’t have a mutualisation of the risks. That is why this is escalating,” said Mr Guglielmi.

Europe’s leaders agreed in June 2012 to break the “vicious circle between banks and sovereigns” but Germany, Holland, Austria and Finland later walked away from this crucial pledge. The chief cost of rescuing banks still falls on the shoulders of each sovereign state. The Sword of Damocles still hangs over the weakest countries.

Peter Schaffrik, from RBC Capital Markets, said there is a nagging concern among investors that the ECB is running low on ammunition.

It cannot usefully cut interest rates any deeper into negative territory since the current level of -0.3pc is already burning up the “net interest margin’ of lenders and eroding bank profits. “How much further can the ECB go before it becomes outright harmful?” he asked.

A string of dire results from banks have set off a firesale on “Cocos“, bonds that allow lenders to miss a coupon payment and switch the debt to equity. A Unicredit issue of €1bn of Coco bonds has crashed to 72 cents on the euro.

The iTraxx Senior Financial index measuring default risk for bank debt in Europe soared to 137 on Tuesday, from 68 as recently as early December.

Mr Guglielmi said the mood is starting to feel like the panic in the summer of 2012, just before Mario Draghi vowed to do “whatever it takes” to save the euro – a shift made possible when Berlin lifted its veto on emergency action to backstop Italian and Spanish bonds.

Mr Draghi is running out of tricks for an encore but there is still scope for “QE2” at the next ECB meeting in March, if he can secure German acquiescence.

He could legally purchase parastatal bonds such as those of Italy’s power group ENEL or Infraestucturas de Portugal, or purchase Italian bad debt packaged as asset-backed securities. “He can buy Italian subprime. That is the low-hanging fruit,” said Mr Guglielmi.

“We all know that QE2 is not really going to work but the feeling in the market is ‘I’m a smoker, I know it kills me, but so long as I can get cigarettes, I’m happy,’” he said.

Source: Europe’s ‘Doom Loop’ Returns as Credit Markets Seize Up – The Telegraph