“3 Things” is a weekly post of thoughts I am pondering, usually contrarian, with respect to the markets, economy or portfolio management. Comments and thoughts are always welcome via email, Twitter, and/or Facebook.

El-Erian – The Value Of Cash

My friend, Anora Mahmudova, recently wrote for MarketWatch about Mohamed El-Erian’s discussion on the importance of “cash” for investors.

“At a breakfast meeting with reporters on Monday, the former Pacific Investment Management Company chief executive said central bank asset purchases have successfully decoupled asset prices from fundamentals and distorted traditional correlations.

‘Investors cannot rely on correlations as a risk mitigator, making cash a very valuable thing to have.

It can give your portfolio resilience during stressful times, optionality—whether you use it for tactical or strategic purposes and flexibility to deploy it when necessary.’

Central banks are finding it harder and harder to repress volatility in financial markets, and any jolts, such as currency devaluation in China or political events, such as Brexit, result in wild swings in the markets.’

El-Erian also said years of unconventional monetary policy, including asset purchases, and a lack of fiscal stimulus are making developed economies less stable.”

Whenever El-Erian makes comments about the value of holding cash, there is generally a good bit of media lash-back about relating to the impacts of inflation and the inability to successfully navigate market cycles.

El-Erian’s comments are a valuation call, driven to excess by monetary interventions, on the financial markets suggesting that having capital invested will likely yield substantially lower or negative returns in the future. This is an extremely important concept in understanding the “real value of cash.”

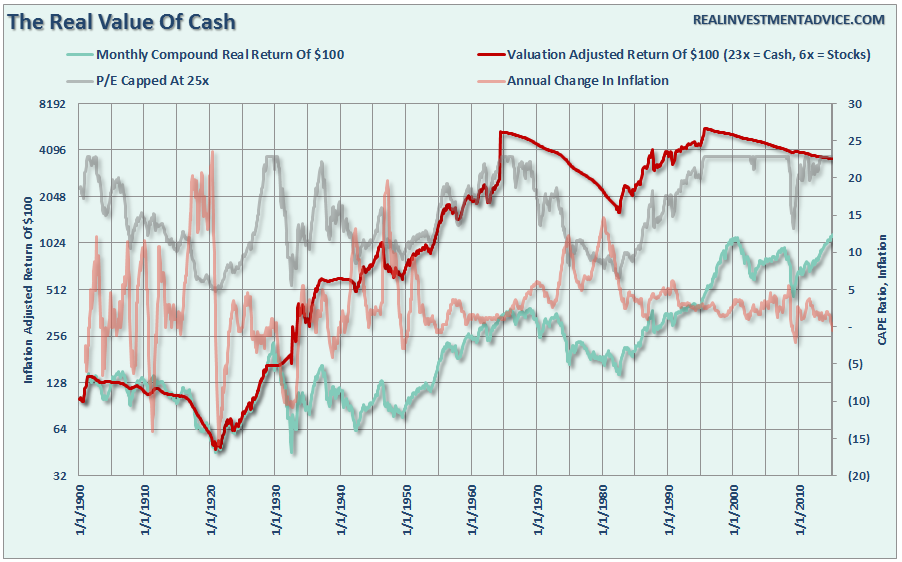

The chart below shows the inflation-adjusted return of $100 invested in the S&P 500 (using data provided by Dr. Robert Shiller). The chart also shows Dr. Shiller’s CAPE ratio. However, I have capped the CAPE ratio at 23x earnings which has historically been the peak of secular bull markets in the past. Lastly, I calculated a simple cash/stock switching model which buys stocks at a CAPE ratio of 6x or less and moves to cash at a ratio of 23x.

I have adjusted the value of holding cash for the annual inflation rate which is why during the sharp rise in inflation in the 1970’s there is a downward slope in the value of cash. However, while the value of cash is adjusted for purchasing power in terms of acquiring goods or services in the future, the impact of inflation on cash as an asset with respect to reinvestment may be different since asset prices are negatively impacted by spiking inflation. In such an event, cash gains purchasing power parity in the future if assets prices fall more than inflation rises.

While no individual could effectively manage money this way, the importance of “cash” as an asset class is revealed. While the cash did lose relative purchasing power, due to inflation, the benefits of having capital to invest at low valuations produced substantial outperformance over waiting for previously destroyed investment capital to recover.

While we can debate over methodologies, allocations, etc., the point here is that “time frames” are crucial in the discussion of cash as an asset class. If an individual is “literally” burying cash in their backyard, then the discussion of the loss of purchasing power is appropriate. However, if the holding of cash is a “tactical” holding to avoid short-term destruction of capital, then the protection afforded outweighs the loss of purchasing power in the distant future.

Of course, since Wall Street does not make fees on investors holding cash, maybe there is another reason they are so adamant that you remain invested all the time.

Fed’s 3rd Mandate

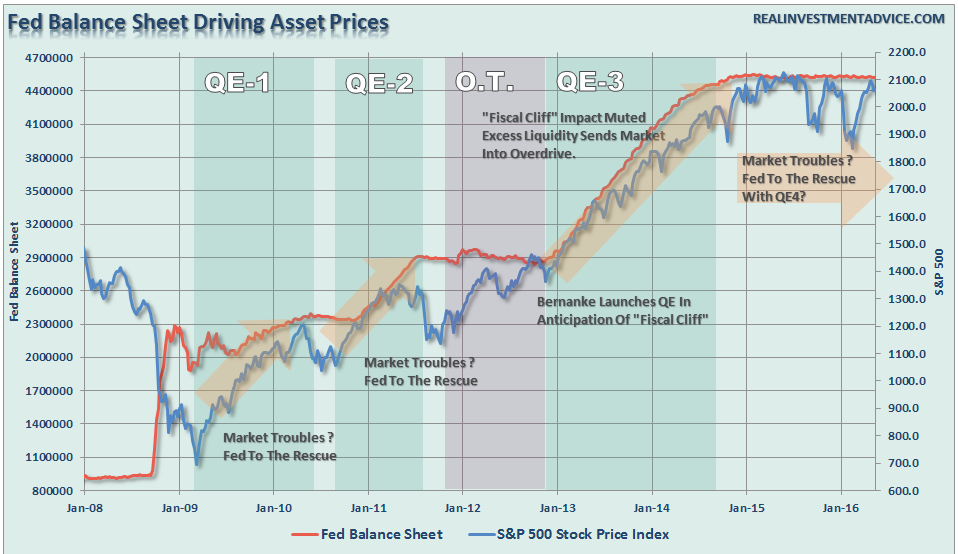

It was in 2010 when Bernanke clearly stated a third mandate for the Fed by targeting asset prices:

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

I remind you of this because this past week, during Janet Yellen’s semi-annual Humphrey-Hawkins testimony, she was asked by California Rep. Edward Royce the following:

“ROYCE: I’m worried that the Federal Reserve has created a third pillar of monetary policy, that of a stable and rising stock market. And I say that because then-Chairman Bernanke, when he appeared here, stated repeatedly that, ‘the goal of QE was to increase asset prices like the stock market to create a wealth effect.’

That seems as though that was goal. It would stand to reason then that in deciding to raise rates and reduce the Fed’s QE balance sheet standing at a still record $4.5 trillion, one would have to be prepared to accept the opposite result, a declining stock market and a slight deflation of the asset bubble that QE created. Yet, every time in the past three years when there has been a hint of raising rates and the stock market has declined accordingly, the Fed has cited stock market volatility as one of the reasons to stay the course and hold rates at zero.

YELLEN: It is not a third pillar of monetary policy. We do not target the level of stock prices. That is not an appropriate thing for us to do.”

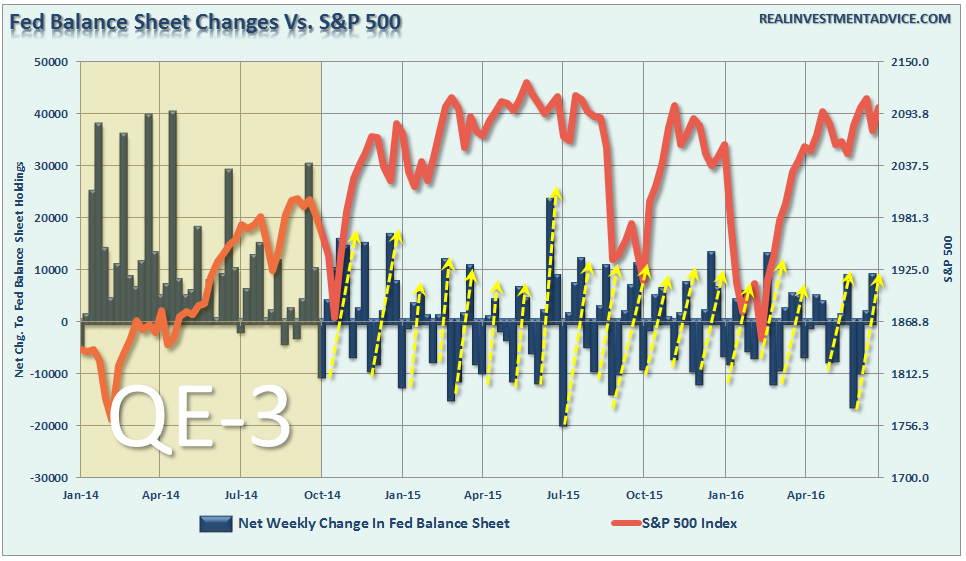

Yellen’s response is most interesting given the weight of evidence to the contrary.

While Yellen stated that it is “not appropriate” for the Federal Reserve to target asset prices, she DID SAY they would continue to reinvest the proceeds derived from their asset base.

It is the timing of those reinvestments that is most suspicious.

Yellen Channels Bernanke

Jon Hilsenrath penned yesterday:

“Federal Reserve Chairwoman Janet Yellen said the chances of recession this year are ‘quite low’ despite mounting worries that the U.S. could be heading toward a downturn after seven years of tepid economic expansion.

‘The U.S. economy is doing well. My expectation is that the U.S. economy will continue to grow.’”

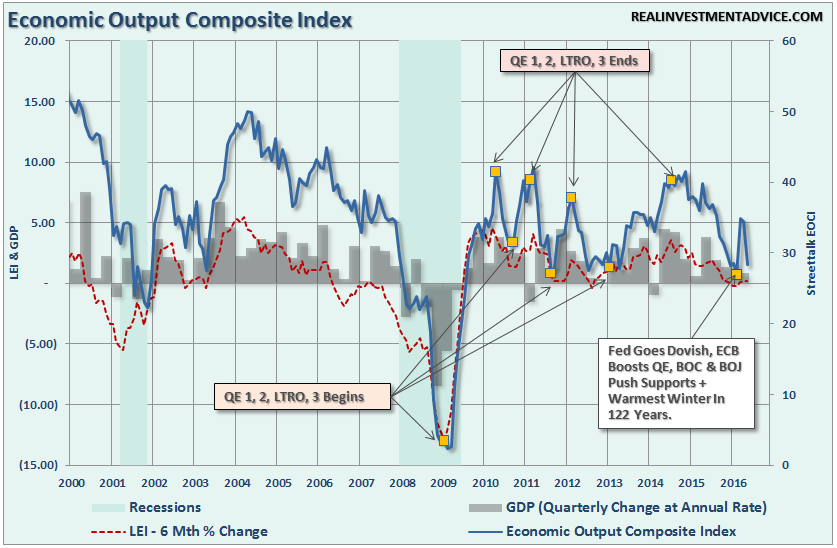

The problem is that a bulk of the economic and fundamental data suggests the opposite is likely true as witnessed by the recent decline in the Economic Output Composite Indicator which measures both the service and manufacturing side of the economy.

The problem, as I have stated many times in the past, is the Federal Reserve can not “speak the truth.” If Yellen stated that despite all efforts, there is little that can be done to forestall an impending recession; consumers would contract, markets would fall and a recessionary onset would be accelerated.

Of course, this was the same problem that Ben Bernanke faced in 2008 when he stated on January 10th of that year:

“The Federal Reserve is not currently forecasting a recession.”

Or on the following 9th of June:

“The risk that the economy has entered a substantial downturn appears to have diminished over the past month or so.“

Well, we all know what happened next.

For investors, the fact Janet Yellen has started to channel Bernanke could well be a clear warning sign that something is about to break.

Just some things to think about.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In