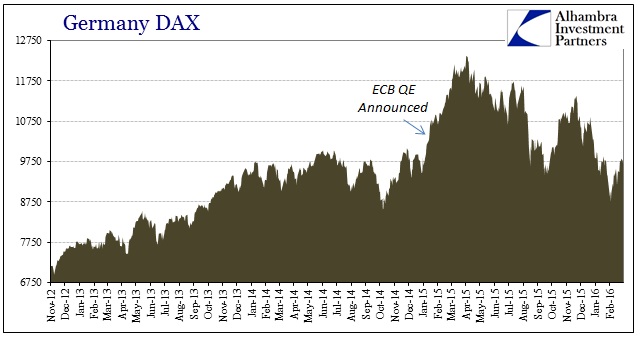

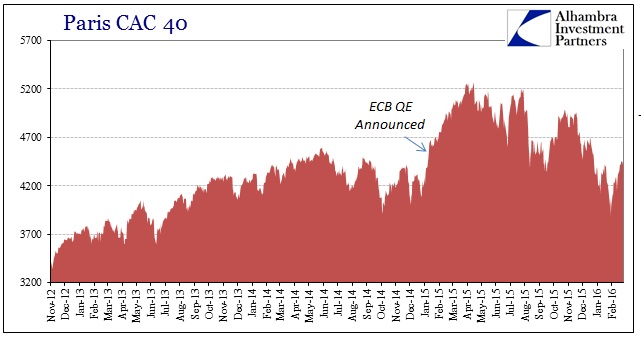

The prevailing view is that the ECB will add to QE tomorrow in accompaniment of a further negative deposit rate floor. Whether or not Draghi and his orthodox economists have the gall to shunt the MRO midpoint below zero remains an open question, but what is less uncertain is that despite just about a full year of actual QE there is nothing to show for it. Even stocks, which were once so easily captured by the illusion, no longer react to the show.

Mario Draghi is having no success convincing stock investors that the European Central Bank has the firepower to reignite growth.

While all economists in a Bloomberg survey expect the central bank to cut interest rates when policy makers meet Thursday, and 73 percent project them to boost the amount of money put into the financial system through bond purchases, fund managers aren’t optimistic about a post-decision equity rally. In the first year of quantitative easing, the Euro Stoxx 50 Index fell 17 percent, and volatility reached levels not seen since 2008. The gauge has dropped in each month but one following an ECB meeting since April.

“It won’t be easy for Draghi to bring back confidence in the recovery,” said Andreas Nigg, head of equity and commodity strategy at Vontobel Asset Management in Zurich. “Growth and inflation in Europe remain stuck at low levels and earnings revisions continue to fall. The market needs better earnings revisions and better economic surprises. ”

In other words, QE is all show just as it always has been. Stock investors are catching up to the vacancy, leaving just economists and their models left to figure this all out. The whole reason again revolves around “money printing” which is nothing of the sort. The sentiment and perception still survives in the media and in general economic commentary, but markets are figuring out QE’s effects on bank reserves count for little more than rhetoric (which is what Andreas Nigg quoted above was getting at; “better earnings” not just more promises for that at some unspecified, distant date).

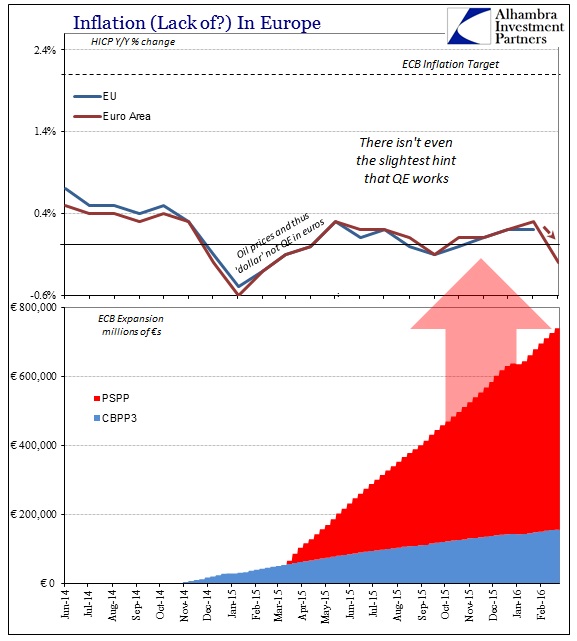

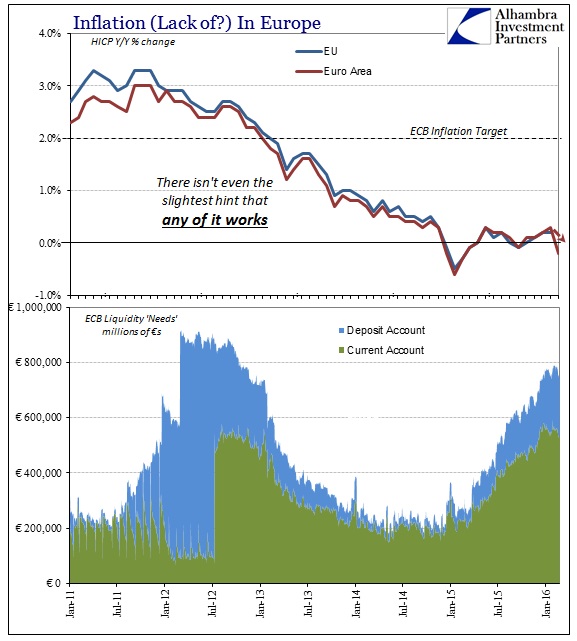

For the mainstream, that leaves this general contradiction which was perfectly stated by the article, “Even after the central bank pumped about 720 billion euros ($794 billion) into the region, manufacturing dropped to its lowest level since 2013, the inflation rate turned negative, and consumer confidence worsened.” The problem is as much conceptual as semantic, as the “region” referred to above was supposed to be the European economy when in true fact the only “region” that saw QE’s direct influence was again useless bank “reserves.” Thus, we arrive at the mainstream confusion as to how three quarters of a trillion euros could possibly go so conspicuously missing, leaving almost no imprint (just the negative distortions in “money” markets) on the financial world – even stocks.

Earlier this month, Markit reported inside their Eurozone PMI’s continued and widespread deterioration including the notion that European factories might have cut prices at the fastest pace since 2013. That would potentially indicate a sudden burst of anti-inflationary discounting reflecting a broad dropoff in overall “demand.” This follows calculated inflation in February across the Eurozone once more dropping below zero. Germany, France and Italy were all included in that “deflationary” track, which again suggests QE just isn’t there.

Chris Williamson said the report suggests that “deflationary pressures have intensified.”

“With all indicators — from output and demand to employment and prices — turning down, the survey will add pressure on the ECB to act quickly and aggressively to avert another economic downturn,” he said.

This is the other contradiction that comes out of QE being so ineffective; in other words, because it had no influence at all economists and mainstream commentary carry on as if it were, in fact, never there. Mr. Williamson suggests that the ECB needs “to act quickly and aggressively” as if they hadn’t already done so. There has now been a year of “quickly and aggressively” and still the potential downturn shows up as a serious possibility, so why on earth would that equate to more? QE was designed and delivered to avert economic downturns through inflation, but there has been absolutely no inflation only the threat of yet another economic downturn, therefore more QE?

It becomes the circular logic of monetarism, as if QE works because QE works. When it doesn’t work, more QE is the answer because it works. This is not science and certainly not logic, nor is it even really about economics per se; this is pure politics where policymakers don’t want a real recovery, they want their recovery, the one that preserves their own central role above all else. If it were a slam dunk guarantee that dismantling the ECB and allowing free markets to suggest allocations and prices would lead to full and complete recovery, the ECB would reject the opportunity (as they have been doing); bureaucracies don’t dismantle themselves, they only (ONLY) spend their resources on justifying their existence even when it comes down to just these sorts of absurdities.

When even the stock market gets it, you know we have reached an extreme.