The European recovery narrative continues without abate despite the lack of validation by something so basic as employment. In tandem with unemployment, inflation has failed to materialize as promised, more than suggesting far more nuance to the recovery failure than simply a return of positive numbers (including PMI’s). While the disinflation has to be a welcome respite among far too few of this ECB era, it does create all manner of monetary contradictions.

In more recent days, Eonia has grabbed attention. In some places, particularly mainstream media, the rise of Eonia to its “rightful” positive spread with the MRO midpoint has brought out the word “normalcy” once again. Since Eonia functions much like the European equivalent of federal funds, it tells us something of interbank unsecured overnight lending. The MRO is a repo-like rate for collateralized arrangements, so it would only be natural to have a positive spread of Eonia to the MRO given the additional risk in unsecured transactions.

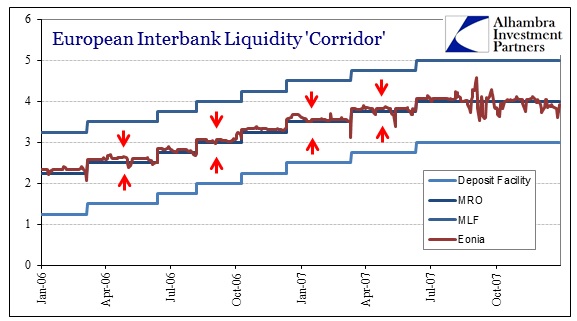

That was certainly the history up to the financial crisis period that first broke in the summer of 2007, nearly six years ago.

The three main ECB rates set a corridor for European money markets, with Eonia defining big bank excess reserve trading. In August 2007, just as eurodollars suddenly exhibited geographic and size fragmentation, so too European money markets took on abnormal dysfunction.

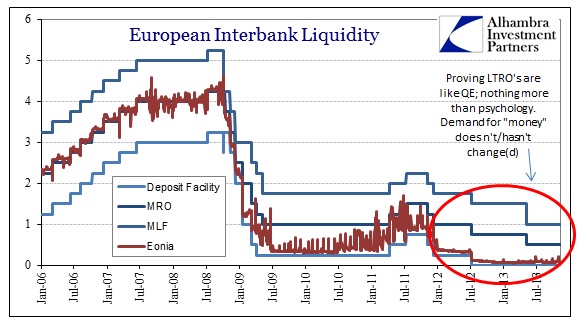

After prematurely withdrawing market support and raising rates in 2011, based on comical levels of over-optimism about a full recovery then, the ECB nearly destroyed the entire European banking edifice (taking the global financial system with it). That led to a flood of reserves through the LTRO’s. However, the LTRO’s did not solve the fragmentation issue which had grown into a more or less geographic divide north to south (PIIGS). The importunately negative Eonia spread to the MRO was unassailable evidence that megabanks with “excess” funds would not lend but to each other – certainly not outside the northern “bloc.”

With the passage of two years, European banks have begun to return their LTRO funding (penalty rates will encourage as much) in a steady withdrawal of “support.” The result has been a rise in Eonia, including more recent days where the positive Eonia/MRO spread has re-emerged. They want it to mean normalcy, but there are clear problems with that interpretation.

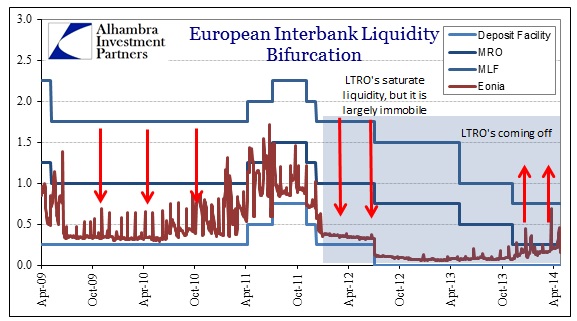

In the first place, normalcy is not just a positive spread but low volatility. Eonia volatility has risen dramatically since November, which would indicate, strongly, that the withdrawal of the flood of reserves is leaving some parties to bid up funds – and to do so irregularly with more than a tinge of desperation. This is also something that we saw in European money markets recently, in 2011.

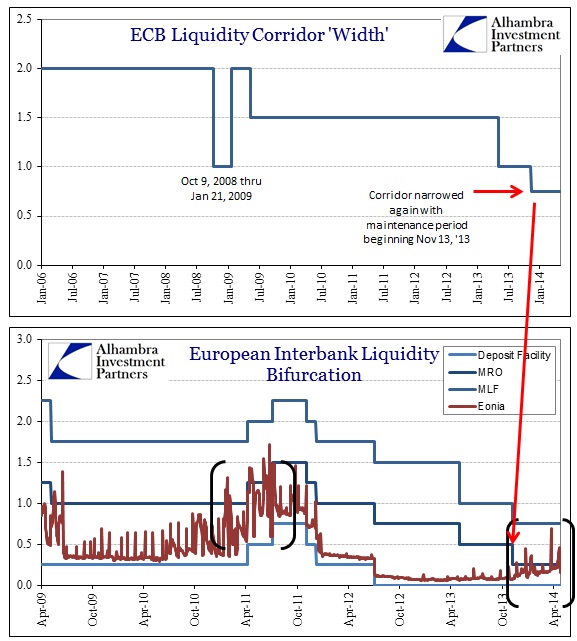

Some of that was to be expected given the timing of the ECB’s November decision to narrow the rate corridor once more to a record low. However, even with that decided abnormal rate setting, the volatility is clearly maligning interpretations of financial regularity. Go back to the first chart in this post; it looks nothing like what we have seen since November 2013. That either means the European money markets have redefined their own natural operation or dysfunction remains and is being slowly revealed by the liquidity tide reversal.

There is no mystery as to why the latter may be the case. Clearly a geographical divide remains. And it certainly relates further to the inability of the EU economy as a whole to move forward into anything even remotely resembling a true recovery.

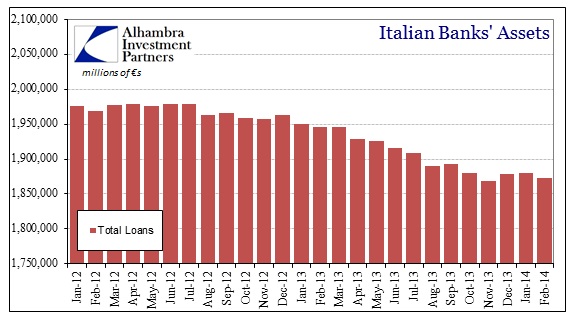

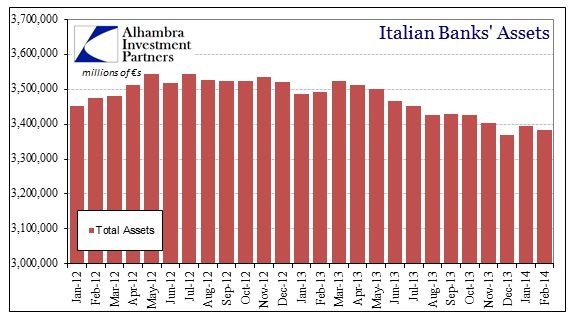

The prime example is Italy. The Italian economy is not Greece, as that and the Italian debt markets are immense. The banking system there should be showing positive signs dating back to November if Eonia was at all meaningful of wider “normalcy.”

Italian banks continue to shrink, particularly loan activity. Even deposit levels are falling once again, but nobody cares as long as the PBOC and Bank of Japan continue to “diversify reserves” of those respective nations. The current disaster in Italian banks would have been a major crisis had these circumstances taken place in 2011 instead of 2013-14. Such is psychology of “markets”, marking the appeal of such monetary measures toward that end.

But in direct contradiction to the health of Italian banks, and by extension their potential and unseen participation in money markets, the deterioration of Italian bank books is more than alarming. I highly doubt it has gone unnoticed by Eonia participants.

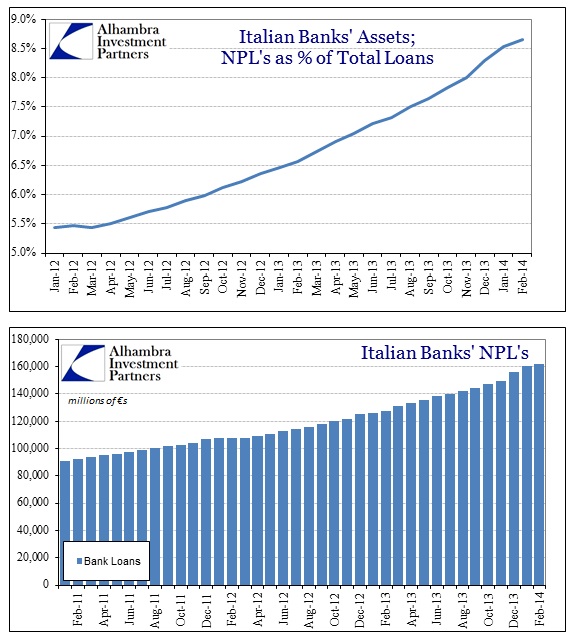

The scale of NPL’s is immense, amounting to nearly 9% of all Italian loans. But rather than conforming to the recovery narrative, which was supposed to have arrived last year, the problem has accelerated. If it isn’t apparent enough in the two charts immediately above, it certainly is below.

S&P in January (FWIW) published its own expectation for NPL’s to rise to 18%, amounting to more than €300 billion by the end of 2014. The rating agency also noted that total accumulated loan loss reserves for Italian banks were just €111 billion. With loan loss estimates rising once more, that screams for additional bank losses (running new loss provisions through the balance sheet) and far more capital (though S&P bravely proclaims current profitability more than enough to generate new loss provisions). Does it scream for a rerun of 2011? Probably not; but it is nothing close to normalcy.

If Eonia rates were rising smoothly, it would be far more convincing toward positive broad function of European “money.” But volatility coinciding with the LTRO’s winding down makes plain there is still a lot of financial disrepair in Europe. The failure of the ECB to sterilize the SMP for four weeks running confirms that (as that would mean banks are increasingly tight about liquidity and in more than short, one-time bursts). Draghi’s invitation to PIIGS and other sovereign debt merely masks the ongoing and deep pain of most of the continent. That extends to the real economy as well, inherent in the stubbornness of “disinflation.” Pump and dump set up on an immense scale, but at least a large proportion of the money markets seems intent on not buying it.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@alhambrapartners.com