What happens at the quarterly window dressing periods for the domestic banking system (which includes foreign subsidiaries chartered for US business) is essentially a gaming of the leverage ratios. As with everything inside the Basel paradigm, banks make themselves look less risky for their reporting periods. In terms of funding markets, that means massaging short-term liabilities, particularly repo. To do so in repo liabilities means to bolster actual inventory of collateral, which, inversely, necessitates reigning in the rate of rehypothecation.

Unfortunately, increasing visible inventory of collateral, and thus less rehypothecation, creates market strains. As securities lending pares back to make it all “look good” for the investor reports and even regulators that is where anomalies seem to cluster.

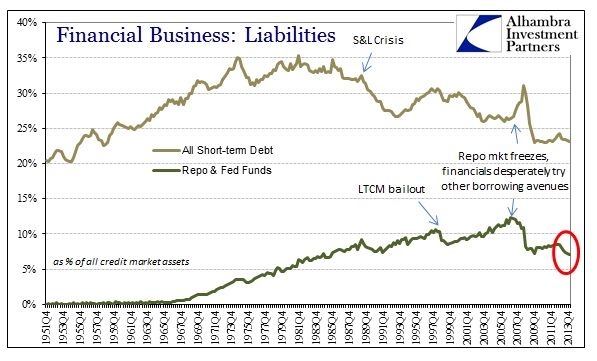

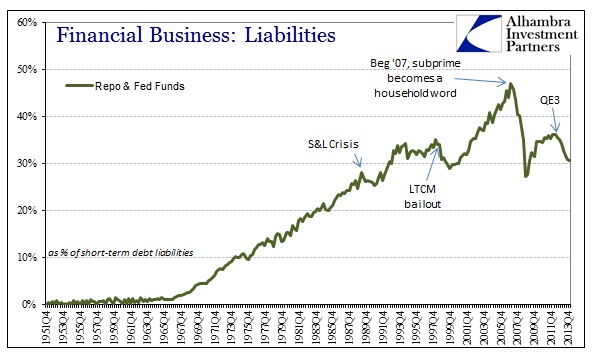

Was it coincidence that the deep panic in 2008 took place right toward the end of that third quarter, with Lehman going down September 15, 2008, just as LTCM had to be bailed out on September 23, 1998? We shouldn’t overlook Northern Rock and the first “emergency” Fed action in September 2007 either.

There has always been a seasonal flow of “money” in the US system, which is why panics so often congregated toward autumn, but that was in a more “primitive” state which was supposed to have been left in the past with the new interest rate scheme. In other words, in the rush to make the system “look” less risky, the system actually becomes more risky as it creates what amount to regulatory-driven bottlenecks. It’s not quite a paradox, but it highlights the depravity built into the framework.

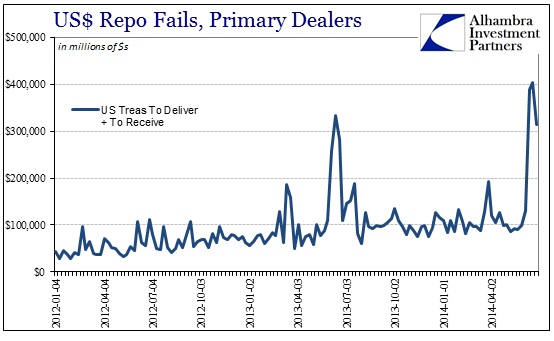

The recent state of repo is becoming more widely scrutinized as outlier events have become more noticeable. In this case, repo fails spiked to a level not seen since those dark days of panic. The pressure of UST issuance (lower) and QE silo mismatch has left the window-dressing state of rehypothecation with fewer options. There is only so much SOMA inventory that will satisfy what the market actually demands at any given moment (contrary to the theory that led to the reverse repo program).

What this means is that banks are engaging hidden risks, a stretching of their fractioning of resources (liabilities), for most of their existence in the shadows of unreported activity. Here too we see somewhat of a paradox in that it has only been QE’s degradation of collateral streams that is revealing this character trait. The large spike last year, during the taper talk selloff in credit markets, again occurred right before a quarter’s end.

Collateral strains of this nature, as I alluded to above, are coincident to some of the worst financial events of the modern shadow/investment banking system. I should clarify that a good proportion of repo is being conducted by securities dealers rather than simple depository institutions (though they are often one and the same, though supposedly separated by subsidiary status to some holding company registration), but that is not a diminishment in the downside possibilities. If anything, that means the potential for liquidity problems is heightened.

The rise of the repo market coincides with the evolution of shadow banking and its attainment of mainstream status. What the securities dealer function of the system allows, funded largely by repo outside of panic and dysfunction, is an orderly pricing function in credit (and by extension almost everything else). Impairment in dealer function is a precarious proposition as it reduces the system’s ability to maintain order in a state of growing disarray. We want financial institutions (short of scrapping this shadow system entirely; a detailed and lengthy, but very much worthy, topic all its own) to be able to “rent out” balance sheet capacity when strain appears. To do so requires “easy” funding via repo, which is why 2008 turned into such a widespread breakout of disorder.

With this quarterly risk “dance” in full view we now see the confluence of two negative forces under these terms. The Fed and UST issuance has recently strained the collateral stream further which has never really recovered from the loss of MBS’ as a main repo tool. Add to that now the window dressing component and liquidity suffers noticeably from this odd behavior (though it is only odd because that is what the regulatory system is set up to do, to allow banks to hide their risky behavior most of the time).

The question for financial participants is whether or not a less solid and shrinking repo market is unrelated to continuous and orderly function. History suggests, decidedly, it is not. For central banks, it seems to follow that they are content, at least outwardly, to simply manage expectations with the idea that will be enough to create and maintain “resiliency.” By persisting with the PR campaign that the world is fixed and close to attaining near-perfection that is supposed to be enough to offset very real weakness in liquidity and emergency balance sheet capacity? Then again, if you actually believe that of the economy and markets then the chances for a financial “shock” are probably trivial in your estimation. But it pays to remember that last year’s bond selloff was also “unexpected” as well.

It’s not exactly the idea of currency elasticity imagined when the Fed was first dreamed up, but then again that function was also mostly PR.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@alhambrapartners.com