The Fed has created permanent housing crisis from which there is no escape.

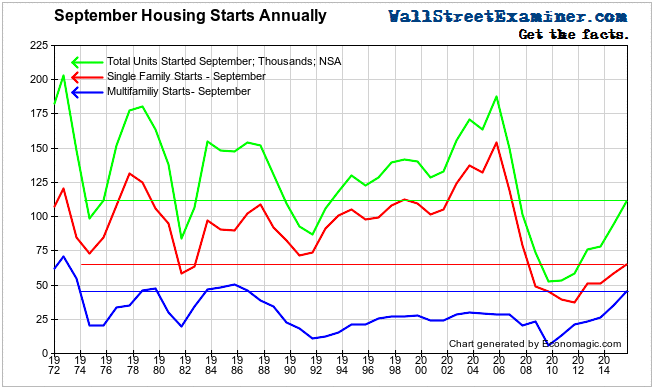

Total US housing starts peaked in 1972. This chart shows actual (not seasonally manipulated) total starts, multifamily starts, and single family starts for each September since then.

Click here to view chart if reading in email.

I have 3 observations.

- The recovery in total starts since 2010 has regained less than the post 1972 average.

- Multifamily starts are near the peak levels of the 1978-87 decade, which is to say, nearing “as good as it gets,” and unlikely to be additionally accretive for the US economy.

- There is no single family housing market. It has recovered only to 1982 recession levels. Prior to the 2008-2012 housing depression, that was the worst housing market in the US since single family starts reporting began in 1959. The single family housing industry in the US is still in a depression.

This can only leave us to wonder what would happen if mortgage rates were to actually materially rise. You can bet that the Fed is wondering the same thing.

If rates did start rising, the housing industry might be stimulated a little at first as buyers and multifamily developers who were on the fence jump into the market to beat rising rates. But once that reluctant pool of fence sitters is exhausted, there would be no more buyers. The next step would be collapse.

The Fed’s only option would then seem to be more QE. We know that economies develop a greater and greater tolerance that drug over time. Japan and Europe are perfect cases in point. They are the walking dead. By keeping rates at zero the Fed has left itself, and us, no way out.