It was another very heavy intervention in yuan last night for the PBOC, making that twice in just one week. The activity is so fierce as to be of similar proportions to the very tight Chinese New Year period, meaning that it is an understatement to say that the PBOC is under great strain. What is less defined, especially in mainstream commentary that flies all over the place, is how there are links between a “dollar” run and onshore yuan financial conditions. From one we can infer the other and that starts with China as being far less monolithic than is assumed.

First, the action recently:

The PBOC auctioned 120 billion yuan of seven-day reverse-repurchase agreements on Thursday, the same as Tuesday, as 90 billion yuan of the contracts matured this week. It will auction another 60 billion yuan of three-month deposits on behalf of the Ministry of Finance on Aug. 25, according to a statement on the ministry’s website. The authority provided 110 billion yuan of six-month loans to 14 financial institutions Wednesday via its Medium-term Lending Facility with an interest rate of 3.35 percent.

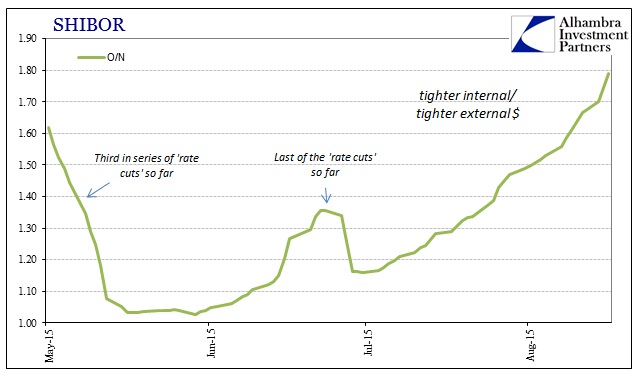

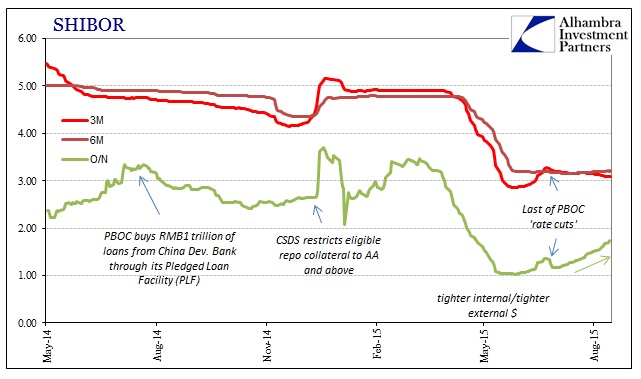

Indeed, the strain in yuan fixing internally is really starting to show. Going back to June, SHIBOR rates (which are only one measure of yuan liquidity) have been rising only at the shortest maturities since early June. The overnight (O/N) rate had jumped from a low of about 1.02% on June 1 before surging from 1.151% on June 16 to 1.35% nine days later. The PBOC issued the last (so far) of its rate cuts at that point, but O/N SHIBOR only retraced for a couple of days before reverting back tighter.

Despite that fourth rate maneuver, O/N SHIBOR has surged from 1.167% on July 6 to now just shy of 1.80%. That date, July 6, matches the change in many other “dollar” proxies, including the crush of oil prices. In addition, later maturities of SHIBOR have been mostly unperturbed regardless of what had been taking place, which adds up to this internal/external “dollar” nexus. Given that the yuan had, at that moment, ceased almost all volatility it is quite reasonable to assume that the PBOC was directly intervening in “dollars” alone in order to at least project a sense of stability that was, as usual for central banks, unearned and ultimately inappropriate.

As I wrote in March last year, when the first “devaluation” eruption occurred, this internal/external, yuan/”dollar” format is often perplexing as rough commentary on China seems to view the place as a singular entity devoid of the kind of nuance reserved for our more “developed” markets. That understates the nature of the Chinese system while over-credits Western “markets” that are in many ways more manipulated than what the PBOC does.

Chinese companies that export to the US (Foxconn) are not the same companies that import resources for all that manufacturing and assembling. The exporters gain a surplus of dollars, but have to turn them over (through Chinese banks) in large part to the PBOC (China’s central bank) to maintain that peg. Importers in turn have to obtain dollars to purchase materials on the global markets because there is, as yet, no depth in yuan trading outside narrow, bespoke bilateral arrangements. Brazil, for example, does not want yuan because it will also need dollars for its own global trade importations. Thus is the world of one reserve currency.

That means that the Chinese corporate sector is “short” dollars to conduct global trade. Exporters had a surplus but gave it up to the PBOC, and importers have to borrow dollars from either foreign banks onshore or native Chinese banks that themselves have to borrow dollars. Somewhere in that dollar chain lays eurodollar market rollovers.

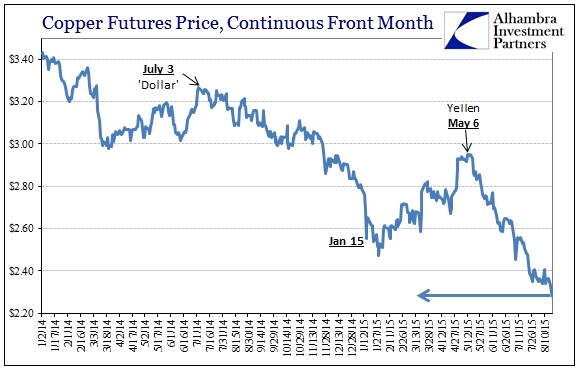

That links US dollar “tightening” to Chinese liquidity. In that corporate sector, dollar lending is often collateralized by copper and iron raw material located in London.

Indeed, that seems to have become the paramount predicate in both financial sets while the yuan fell silent. But, like a coiled spring, it could only remain in that state so long as either the internal strain was manageable or the external pull of the “dollar” did not extend too far in time or depth. We know with reasonable assurance that the latter was the likely catalyst, as the “dollar” run in so many proxies in August simply turned punishing. The PBOC, caught between trying to project calm as “dollar” liquidity turned only worse and thus entangling yuan liquidity has now been pushed into drastic measures where neither end of the conduit are responding with much favor; despite the break in the yuan, not really “devaluation”, the internal dynamic continues to grow worse suggesting that last week’s break wasn’t nearly enough of a game changer.

This has always been the worst case scenario, as the idea of reform as a general concept was quite simply to avoid Japan’s fate entering the 1990’s. I believe quite strongly that the PBOC recognized the similarities some time ago, and that, in my view, the idea of reform was to try to “correct” the financial condition before it became too late. In other words, Japan after the Plaza Accord in 1985 refused internally the adjustment; the Bank of Japan just went nuts and asset bubbles were apparent almost everywhere, and not just stocks but real estate. For China, the Great Recession was their “Plaza Accord” and the PBOC didn’t just go insane but historically so.

The idea in both situations was to use internal monetary mechanics (bubbles, as the Yellen Doctrine now asserts as useful) as a bridge over or around heavy adjustments. In Japan’s case, the believed restoration of a more favorable external balance did not arrive before the monetary expiration. I think that is where the PBOC was in 2013, namely that it took the 2012 global slowdown as the final say in the matter of “the other side”; there was only to be an ugly economic fate.

At that point, I think they made a conscious effort to try to avoid Japan’s disaster by actively engaging to manage a bubble decline regardless of how much growth had to be “sacrificed” to do so. All that has happened since March 2014 seems to conform to that effort:

What we can take away from all this is that China is one massive mess of dollar entanglements, cornered by an export focus that won’t recycle to the previous peak, further wrapped inside a credit bubble beginning to show signs of cracking. The “usual” remedy for such a system is to try to “export your way out of it.” And that may be the forward intent if it doesn’t get too complicated by eurodollar mechanisms ahead, but it also may signal a far darker worst case (that may be more probable than anyone admits now) – China in 2014 is Japan in 1989. There are enormous similarities that make such a comparison compelling, enough to further study how that analogy might work out alongside their differences.

With “further study” largely in hand, especially lately, I think the conclusion is setting against the Chinese intentions as perhaps inevitability. It was always a low probability of success, in my view, that tremendous financial imbalance could be wound down in an orderly fashion without simply breaking out into the typical crash reset. That the Chinese would attempt such a “hail mary” to me cemented the Japanese analogy – they had to try because not doing so, the Japanese path, was far, far worse than the dangers of managed decline getting out of hand. A small probability of success was far better than what surely awaited doing nothing.

I don’t quite think China is at that point yet, but recent events more than suggest it is, as within a probability distribution, becoming more the base case than an outlier as hoped. These financial entanglements are the reasons that it was all a low probability to begin with and their activations in harmful succession (including the stock bubble on the way up and now down) reinforce maybe what should be the object lesson in all of this; history repeats because every generation thinks it has solved the “mystery” when in fact bubbles are not tools but only (ONLY) seeds of eventual destruction.

Like the 1983 movie WarGames about nuclear war, the only takeaway is not to play this game in the first place.