To an economist, the economy can bear no recession. In times of heavy central bank activity, an economy can never be in recession. Those appear to be the only dynamic factors that drive economic interpretation in the mainstream. And they become circular in the trap of just these kinds of circumstances – the economy looks like it might fall into recession, therefore a central bank acts, meaning the economy will avoid recession; thus there will never be recession. It requires that both the central bank will identify the recession correctly and then invent and apply the requisite “acts.”

It was never really that simple to begin with, but what happens, like now, when central banks remain in the act (monetary policy, we are told, remains “highly accommodative”) but the economy appears more and more like recession? The result is increasing nonsense and absurdity. Such as:

But Deutsche Bank AG Chief International Economist Torsten Slok has some counterintuitive advice for his most pessimistic clients: Buy.

“I frequently hear clients express very negative comments about the U.S. economic outlook, including the statement that that economy is already in a recession,” he wrote. “The irony is that if you have the view that things are really bad at the moment and we are currently in a recession, then it is actually a good idea to buy risky assets today.”

If there is “blood in the streets”, etc. The problem with that saying is that nobody ever tells you how much blood must be in the streets to actualize those sentiments; even if there appears a lot of carnage there might still be room for a lot more. In fact, this happens far more than you think. For economists, they will first tell you that such blood-letting is impossible before being forced to admit it’s there only to suggest there will be no more.

That makes past denial relevant as if in court admissibility of prior bad acts. In Mr. Slok’s case, you can go back to the summer of 2014 when he suggested that stocks would go up until there was recession (ironically, the title of that post in 2014 was Deutsche Bank Economist: ‘Buy Equities’):

I believe the stock market will continue to go up until we get a recession. And we are nowhere near entering a recession. Recessions happen because of a bubble bursting in capex (as we saw on 2000) or because of a bubble bursting in consumption (as in 2008) or when monetary policy is too tight, i.e. when the fed funds rate is well above its neutral level. None of this is happening at the moment. If anything, we are seeing too little capex and consumption.

It’s safe to say it has been all downhill since that moment, ironically as the “dollar” has only “risen”; or what economists like Mr. Thok would claim, if they were aware of wholesale banking, as money being too tight. The problem with holding outside the financial paradigm is that it is impossible to recognize the relevant circumstances. The primary reason Thorsten Slok is so sanguine is either intentional obtuseness or great miscalculation. Back to his proclamation today:

Put simply, the U.S. leverage problem of today is peanuts compared with the Great Recession. The key factor informing Slok’s position that fallout from crashing oil prices won’t be a repeat of the subprime meltdown is the yawning gap between credit outstanding tied to mortgages circa 2006 and high-yield debt in 2016. [emphasis added]

The chart accompanying that claim shows that mortgages as a whole were a much higher percentage of overall credit than high yield is now; it’s not even close. But that is highly disingenuous. It wasn’t overall mortgages that were the problem then, it was and started in subprime. Thus, the correct scaling and comparison is not all mortgages then to just junk bonds now, but junk bonds now to subprime mortgages then or even all corporate debt now to all mortgage debt then. As noted here, if there is a problem in junk bonds, it won’t remain solely a junk bond problem as if magically “contained.” The basis of wholesale liquidity and the structures that perform on the way up and then disintermediate on the way down destroy the idea of “contained.”

This isn’t, however, the first instance Mr. Slok has downplayed the potential reversal of banking leverage and the economic potential of that. In this presentation given in June 2008, Slok and Deutsche Bank were also quite positive on the outlook even at that late date:

Aggressive easing of fiscal and monetary policy could build a bridge in Q2 [2008] and Q3 [2008] over a potential recession.

Worse, he presented among his “often-ignore facts” that, “Banks have so far raised capital to cover an impressive 75% of their losses.” That was only “impressive” in that apparently Deutsche Bank didn’t, like now, expect it to get any worse. A good part of the reason for that was, “Stimulus provided by economic policy is significant.”

Then, like now, there were conflicting market accounts about where the economy was headed. That is the case for every recession or depression ever presented; there are no clear signals from markets or otherwise for the onset of economic dislocation, nor will there ever be. Slok instead took that as being inconsistent and thus defaulted to the standard monetary policy setting:

Mr. Slok is nothing if not consistent – and that is the problem. It’s not that he doesn’t think there will be a recession this year (or that there might have started one last year) like he thought the same as late as June 2008, recessions are always arguable when they start even to the point after they start. Instead, my contention is the manner in which he downplays the risks of it on two accounts. First, that monetary policy will save us all somehow now even though it did nothing on that count then. The monetary efforts that he believed would avoid a recession at that time not only failed to do so they were no mitigation whatsoever into a devolving panic and then economic catastrophe that we still seven and a half years later have not yet erased.

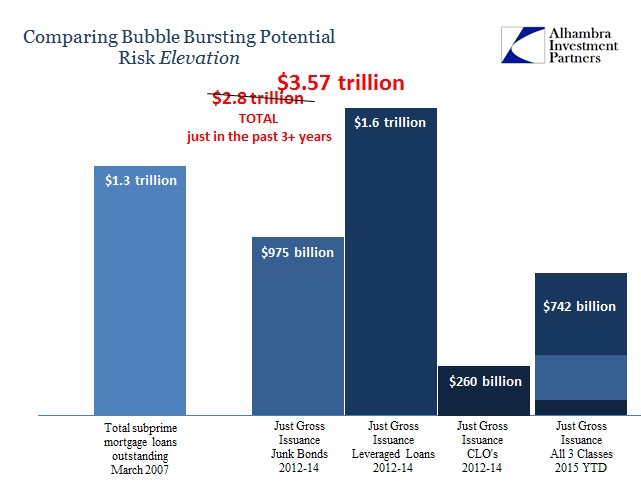

Worse, however, is this misreading of leverage and banking in his highly duplicitous manner. The comparison of junk bonds to overall mortgages is just plain wrong; the only question is whether it was intentional. On relatively comparative terms the current scale is much closer than anyone seems to recognize, but in raw, absolute numbers by the type of distribution it may be even worse than the subprime meltdown.

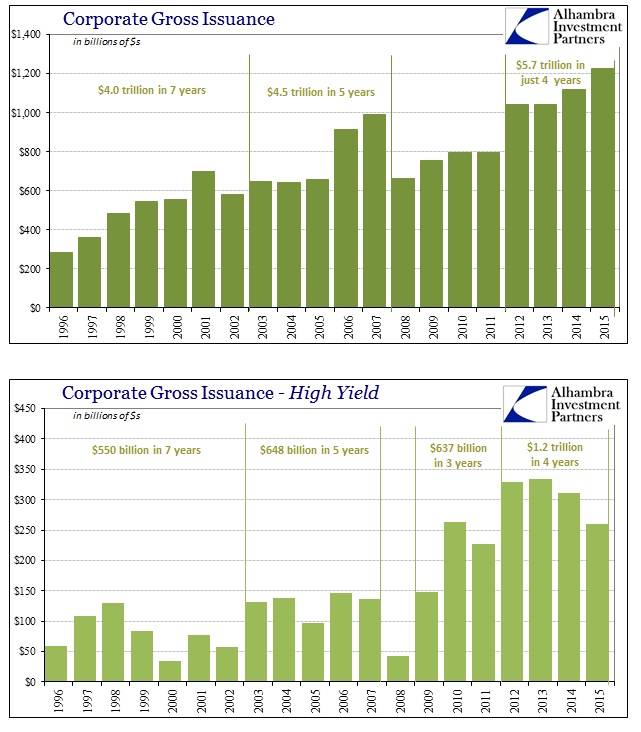

In the mania portion of the housing bubble, covering the six years 2002 through and including 2007, there was about $15.9 trillion in mortgage-related debt gross issuance according to current SIFMA estimates. That includes only a fraction in subprime. In the past six years, from 2010 though and including 2015 (with preliminary figures through December), there was $7.8 trillion in gross corporate debt issuance. That may have been a little less than half in terms of overall volume, but the proportion in junk was far, far higher than the relative containment of subprime. And I haven’t even included leveraged loans in that figure.

In net terms, there was about $9.4 trillion in MBS debt outstanding at the end of 2007; $8.3 trillion in corporate debt (again, not including leveraged loans) at the end of Q3 2015. To suggest there is no comparison of leverage or risk exposure then to now just isn’t in any way correct. There might have been more raw mortgage volume in the housing bubble, but not so much more as to preclude any risks at all in 2016 and certainly nowhere near the “yawning gap” Mr. Slok tries to claim. Instead, the proportion of junk within the latter corporate bubble might in many ways mean a much more precarious station as the junk bubble is just now starting to crack up.

Where there is even more common ground is that true monetary condition that seems to be far too similar to 2008. The Fed believed itself “aggressively” accommodative in terms of monetary policy but the results prove, inarguably, it was no such thing at least not in the method that would matter. The eurodollar system imploded and thus removed all support for asset prices which were liquidated in general fashion as it occurred; often swiftly. The eurodollar system now is in the same position if not yet with the same sustained intensity; however, we have seen glimpses of that already in general, global liquidations if only in acute, discrete outbreaks to this point. But that is as much a warning of the similar type of general monetary instability; a warning not heeded by economists that never see these things coming because they remain fixed to a central bank-centric monetary system that ceased to exist as early as the 1960’s.

In other words, there remains the potential for a great deal more blood to flow – into the streets or just contained within the realm of wholesale finance. In the end it may not matter which, as the imbalances then and now are in some ways just the same if expressed slightly differently. The risks are all still there, and economists are still determined to downplay if not miss them entirely.