In yet another anecdote that proves the global recovery can only be political, acting Brazilian President Michel Temer appointed Ilan Goldfajn to be the next central bank head for that nation. Goldfajn is about as orthodox as they come: trained at MIT (saltwater, as if makes any difference), former director at the central bank who has “consulted” with the IMF, World Bank, and United Nations. The nomination has pleased all the “right” people who are absolutely certain that Brazil’s worst days are now behind.

Reuters probably wrote about it best, unintentionally, under the headline Brazil Government Taps Wall Street Favorite To Head Central Bank.

“Well-trained technocrats … should allow the government to establish a clear regime shift,” Goldman Sachs senior economist Alberto Ramos wrote in a research note.

Trained by whom? To do what? More of the same. Along with Mr. Goldfajn’s recommendation, the interim government also indicated it would formalize rules making Banco more independent and supposedly less susceptible to political influence. The current structure for the central bank is highly unusual, with a shared power structure among the National Treasury, the Bureau of Currency and Credit while also including a private sector foundation in Banco do Brasil. “Independent” central banks, even here where it is insisted that independence will be expressly limited, are all economists want to hear as it gives them unrestrained power.

The move was welcomed by economists, who said the rule change would help bring down inflation, which is still running at more than 9 per cent — twice the country’s official 4.5 per cent target — in spite of an interest rate of 14.25 per cent.

“This is a positive step and a quick win for the government, and should help to anchor long-term inflation expectations,” said Neil Shearing, economist with Capital Economics.

How? His MIT degree will scare away monetary imbalance through sheer reputation alone? Long-term inflation expectations don’t source from MIT, the IMF, or the United Nations no matter how noble Mr. Goldfajn might be in person. Brazil has an enormous “dollar” problem and they respond predictably with the most orthodox man ever educated. Those who are praising the appointment actually believe they are complimenting him by calling him a “technocrat.”

To be a technocrat one has to demonstrate competency and a good grasp of the subject (and object). Those that are now being quoted all over the media in favor of this direction are the same that cheered on his predecessor who in 2011 acted on Finance Minister Guido Mantega’s first screams of “currency wars” and then committed Brazil to its predicate doom.

In early 2011, there were no disqualifying conflictions of interest or format, as the central bank (which I usually refer to as Banco alone, for many reasons) was intent upon halting the real’s appreciation against the growing tide of Mantega’s currency wars. By mainstream accounts, Banco (the acting agent) initiated auctions for 20,000 contracts of a “reverse swap” arrangement whereby Brazilian monetary authorities (of whichever end) promised to pay the overnight rate in reals against a set, fixed rate in dollars.

The Brazilian dollar network node is a bit of an odd arrangement, compared to other places, which isn’t all that surprising given the setup here. But what are taken as currency swaps by the central bank aren’t really that, instead they are rate swaps intended upon influencing the onshore “dollar” rate, really a spread – the cupom cambial. The intended effect of what Banco was doing in January 2011 was to reduce the cupom cambial in order to make it less profitable for Brazilian banks or foreign subs operating in Brazil to “import” “dollars.”

After making “dollars” relatively scarcer in 2011 and 2012, these proficient technocrats were suddenly caught in the vise of another technocrat’s inflated esteem – Ben Bernanke. As if some kind of Golden Age Hollywood comedy, the orthodoxists at Banco suddenly were “forced” by their own actions into truly drastic and sudden reversal.

The real’s appreciation eventually did halt, but instead of providing the utopian monetarism Banco sought has turned into an ongoing nightmare in the opposite direction. In August 2013, there was more cupom auctions to be had only this time not “reverse swaps” but of the straight variety, as much as they may be in Brazil. Rather than try to influence “dollars” away from Brazil to halt appreciation, the central bank was getting desperate to induce Brazilian banks to attain them. And so the bank began a series of auctions, historically large, which had the practical effect of making Brazilian banks even more “short” the “dollar.”

It’s an exceedingly weird and difficult concept, as in convention almost everyone talks as if there is actual currency in all this – there is not. The wholesale system does not operate on such platitudes and anachronistic arrangements that make for currency as it was always known. What happens are bank exchanges among, and only among, various forms of ledgered liabilities. When Brazilian companies need dollars to engage in foreign trade (on both sides, to buy and in reception during a sale) Brazilian banks source those “dollars” via the eurodollar market and then lend them internally, pocketing whatever spread they can find after whatever influence is acting wherever. That means the “dollars” they obtain are eurodollar bank liabilities typically of small duration – they are synthetically short the “dollar.”

In the context of summer 2013, then, Banco’s intentions were clear and even understandable at least in the very narrow orthodox conception but well more than a little dangerous. By incentivizing Brazilian banks, through the cupom cambial rate, to increase “dollar” exposure the central bank was, in effect, having Brazilian banks “short” the “dollar” to a much larger extent than they already were. It seemed like a worthy gamble, as every economist in the world proclaimed both global recovery and placidity in global finance as a result.”

We know well the result even if the technocrats continue to deny how it ever got that way. Here’s the Wall Street Journal today congratulating the nomination while simultaneously describing what happens when economists like Goldfajn become central bankers given so much discretion:

The Selic is among the highest benchmark rates in the world. Punishing interest rates have hurt businesses and slowed consumption at a time when the economy is already mired in a brutal recession. GDP shrank by 3.8% in 2015 and is expected to contract by that much again this year. Unemployment is nearing 11%. Yet Brazil’s inflation is still nearly 10%.

That in no way argues for bringing in yet another MIT (or Princeton, or whatever) economist who would have done nothing differently. This new appointment is being couched in political terms as if it were left vs. right; impeached President Rousseff was a leftist so we are supposed to believe Temer’s more center-right politics is all the difference. These terms don’t apply in central banks and markets – left or right, they are all orthodox economists who have proved time and time again they don’t have any idea what they are doing. To wit:

The roster of Brazil’s woes is almost unbelievable; -4% on GDP not once but in at least consecutive years; 11% unemployment; 10% inflation. And all of it without the slightest hint of yet a bottom even though this depression has been building for those three years. When Alexandre Tombini, the man Goldfajn is to replace, was nominated in November 2010, economists were also quite thrilled for all the same reasons because he possessed all the same characteristics.

“Tombini is an excellent choice for the central bank, his nomination should be well received by the markets,” Marcelo Carvalho, head of Latin American research at BNP Paribas in Sao Paulo said in an e-mail. “He is highly qualified, has a solid academic background, important international experience and a strong professional reputation.”

Goldfajn is functionally no different than Tombini, but he serves the primary purpose of rebranding. And so after one orthodox head destroys the economy he is replaced by another orthodoxist though under a different political party as if that were a meaningful distinction. That is what I mean when I write that the recovery is political – it isn’t about parties, it is about economists. In economic and monetary policy terms, there is no binary circumstance there is only one option – orthodox attaches to both “left” and “right” with great ease and flexibility. It’s not “R” or “D”, it is the first political movement that realizes central bankers are and have been entirely the problem.

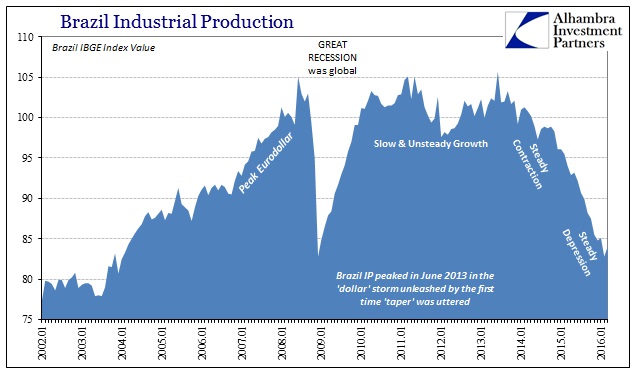

As if to prove that point, Goldfajn argued last year at an event in Israel that Brazil needs to raise taxes and cut government spending but also “boost exports.” In other words, they just repeat these words as if they have meaning; taken at his word, should we expect Banco to dramatically lower SELIC now and undertake more reverse cupom swaps to get the real even lower, meaning even tighter “dollar” supply? Are we supposed to just ignore that exports in Brazil have collapsed and industrial production imploded while the preferred orthodox “stimulus” toward exports, a weaker currency, has already devastated Brazil?

They really don’t know what they are doing and their only demonstrated ability is to make bad situations that much worse. It just doesn’t end until the whole politics of economics changes.