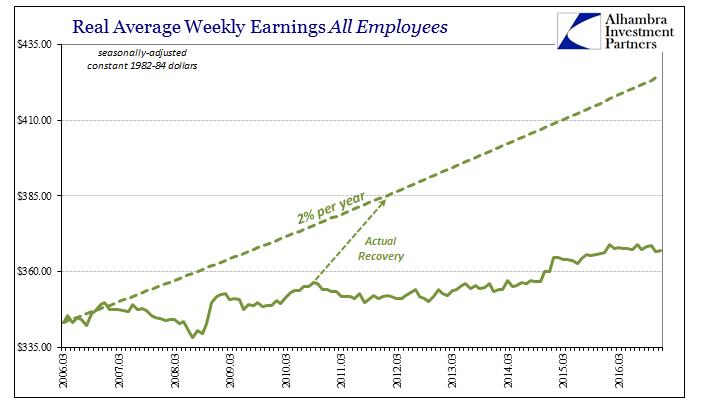

Earned income rates adjusted for inflation have been near zero growth for two months in a row. Real average weekly earnings were revised significantly lower in November 2016, turning a small 0.5% gain into just 0.2%. The latest figures for December estimate the same lack of growth to end the year. In seasonally-adjusted terms, weekly earnings did not keep pace with largely oil prices all throughout last year. Weekly earnings started out 2016 at $368.80 (constant 1982-84 dollars) and ended at just $366.95.

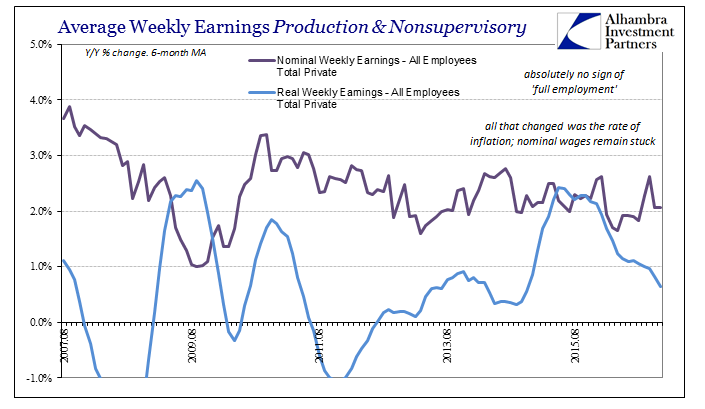

This is, of course, nothing new. It has been a constant feature the whole of what should have been recovery, where first and foremost the lack of income growth suggests “something” seriously wrong that no QE or “stimulus” policy can or will fix. The shift in real earnings in 2016 is due to both oil prices as well as the lack of nominal wage growth, with the latter far more important than the former. For an economy near or even at most economists’ definition of “full employment” for going into a third year, the lack of wage and income acceleration really is damning.

Workers know that nominally incomes are stagnant at around 2%, meaning deficient opportunities for personal advance overall, and therefore the effects of inflation (largely oil prices) are not helpful in either direction; it is only further volatility inside the stagnation dynamic. Consumers didn’t spend their oil price crash “windfall” in 2015 as economists expected because why would they? Without actual wage growth at the top, changes in inflation even favorably are not a permanent or even durable trend upon which workers would rely.

That suspicion was confirmed last year as wages nominally remained frustratingly stagnant all the while spending on gasoline eroded discretionary margins all over again. It is absolutely incredible that in terms of real earnings, the largest gain since before the Great “Recession” was actually delivered by the oil price crash. That tells you a great deal about this economy, especially as even then it was an exceedingly small gain.

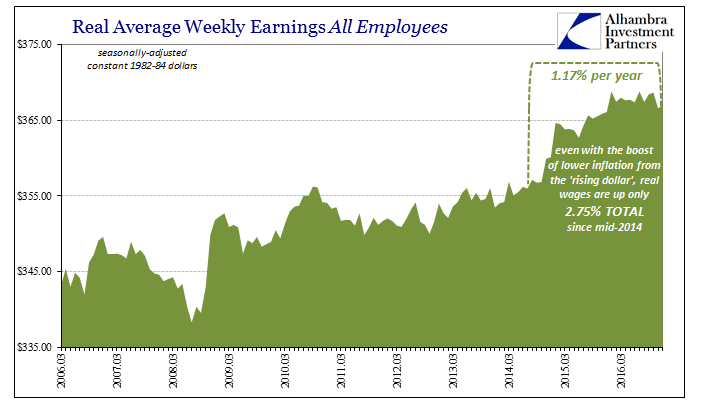

Since August 2014, real average weekly earnings have increased by less than 3%; total, not per year. That works out to a compounded 1.17% annual growth rate. Because of the sharp decline in inflation during that time, real earnings appeared slightly better than they had been before. There was almost no wage growth from the middle of 2012 until the middle of 2014, meaning that because QE failed in its primary task (to boost inflation) consumer conditions at least weren’t worse than they already were.

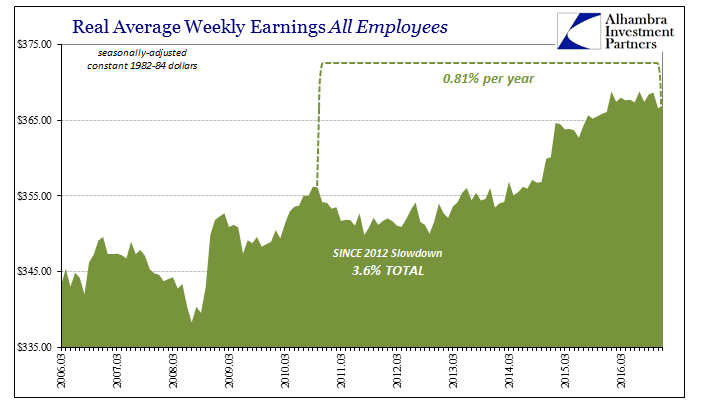

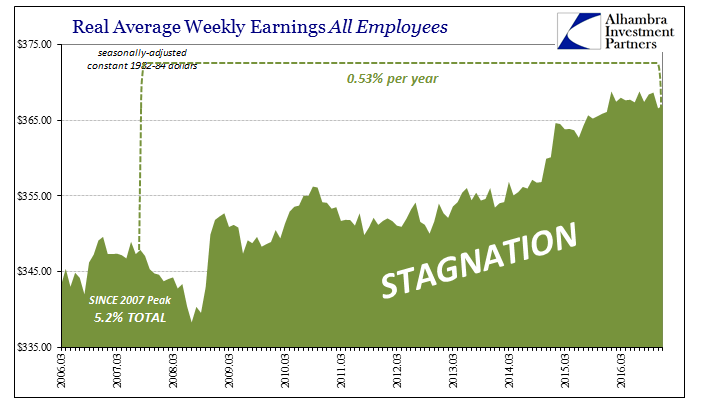

Going back to the worst in early 2008, real earnings are up only 8.5% in total, still less than 1% per year. Measuring peak-to-peak (current) real earnings have grown by just half a percent per year. Thus, there was no recovery in wages and incomes, suggesting why spending never recovered, either.

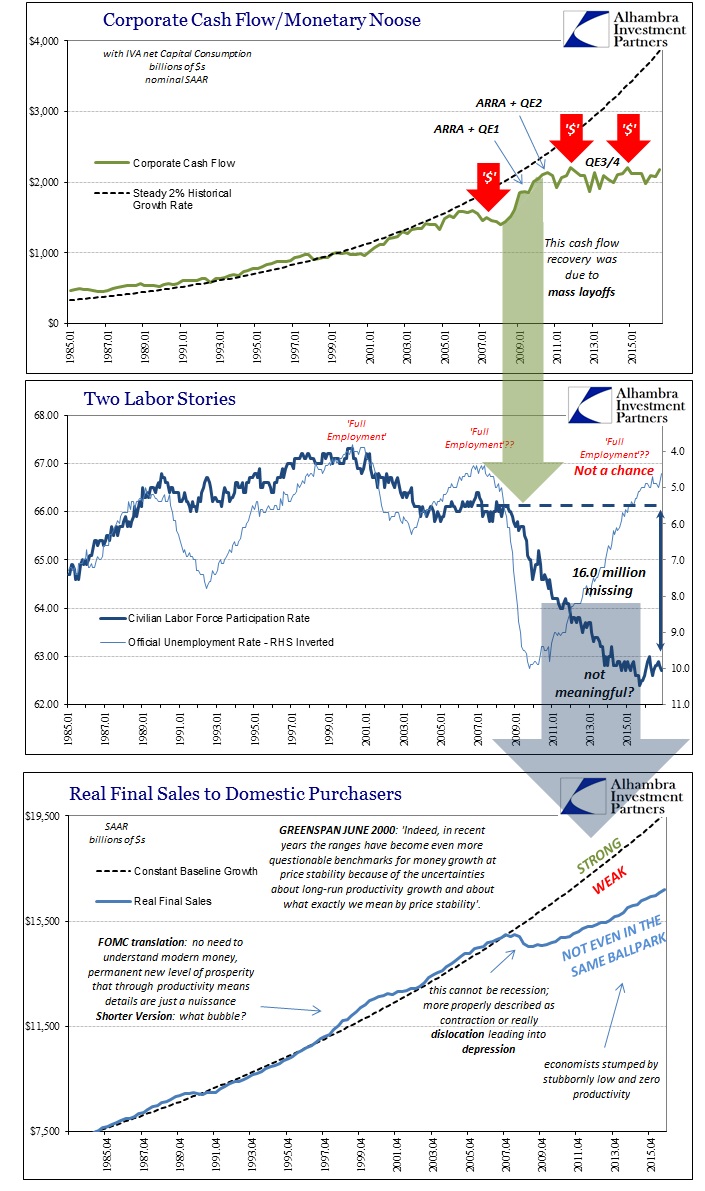

The lack of growth in income is but part of the economic problem, as it applies only to those who have remained employed throughout as well as the so very few who were fortunate enough to obtain whatever few new jobs have been created. These two factors are obviously related, as the lack of wage growth is a direct result of the participation problem on at least two counts. The first is the idea of “slack”, where clearly “full employment” cannot be correctly applied to the current circumstance. The second may be even more important than that, as for whatever reason the hit to the labor market during the Great “Recession” appears to have been oversized relative to certain measures of it.

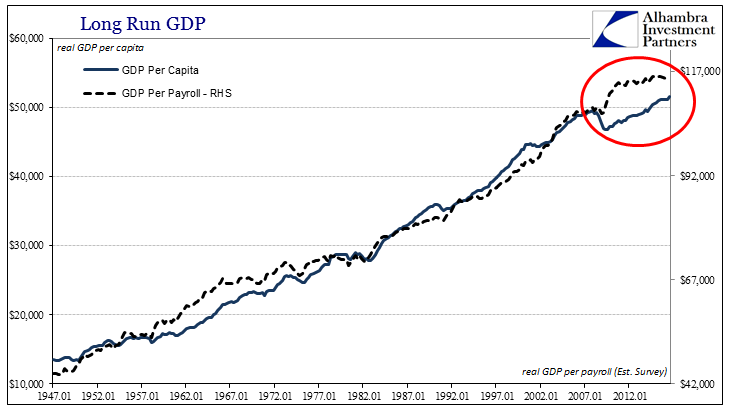

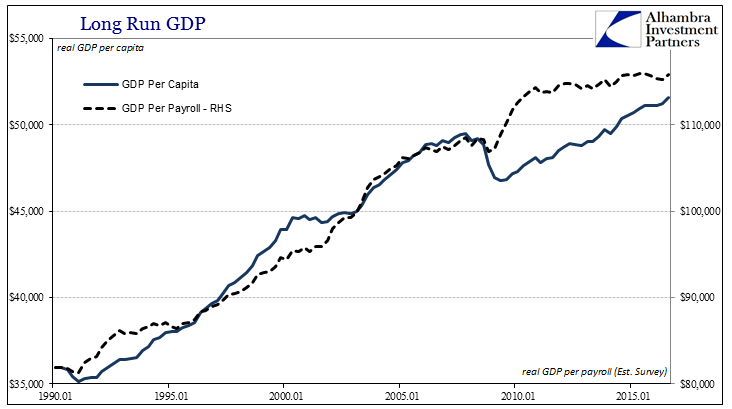

For example, GDP per Capita shows quite well the level of depression since 2007; like wages, GDP in this standard comparative format is barely above (just 4.1%, total) the prior peak reached almost a decade ago. But if we “deflate” GDP by the number of payrolls (Est. Survey), there was a huge discrepancy during the worst of the contraction.

This was totally unusual and not something we have seen before. Going back to 1947, GDP per Capita and GDP per Payroll remained largely in agreement, both temporal direction as well as degree. During the 1970’s and early 1980’s, for instance, GDP per Payroll was largely a leading indication for GDP per Capita which only makes sense; it is a less-refined version of productivity. Even during the worst of those recessions, the double dip in 1981-82, both GDP per Payroll and GDP per Capita rebounded sharply together.

In 2009, by contrast, GDP per Payroll rose sharply as the pace of layoffs was much greater than the pace of GDP contraction. It has been this difference that has defined the lack of recovery the past almost decade. Economists have attributed this to, where actually offering a possible explanation, Baby Boomer retirement and/or “skills mismatch.” Both are clearly nonsense.

What would cause businesses to all-at-once and all-at-the-same-time shed so many workers? Recessionary forces were part of it, though that doesn’t explain why they were so amplified especially in Q4 2008 and Q1 2009. Former Treasury Secretary Hank Paulson recounts in his own slanted memoirs a call from GE CEO Jeff Immelt about his company’s difficulties in financing not just its mortgage portfolio. Former Assistant Treasury Secretary Neel Kashkari, the government official who would run TARP, told Charlie Rose of PBS that:

We were getting calls from large American businesses, blue-chip businesses, saying they couldn’t fund themselves, they couldn’t make their payroll, they couldn’t fund their inventory.

Most have dismissed these comments as the ex post facto rationalizations of the late Bush administration handing out government money to their crony connections. I don’t want to discount that possibility, as clearly cronyism was a part of that mix, but the realities of post-Lehman and the funding relationship of banks to more than just the biggest companies was very real and very problematic. It wasn’t just non-financial commercial paper that was used by firms beyond GE to run working capital, there were standby letters of credit as well as revolving funding lines that were canceled and often all-at-once without notice. Thus, as revenues fell, there were no alternatives.

Global banks turned their backs on global businesses, and it was some months before conditions sufficiently calmed to where some businesses could begin to work around banks via the bond market. In other words, businesses all over the world, including small and medium-sized enterprises (as they are known in Europe), were highly leveraged their day-to-day activities. When the leverage disappeared, they had only one outlet – mass layoffs. So much of the Great “Recession” was monetary, which contradicts neutrality (again).

With such a huge shock, the system has been unable to recover. The massive forced “deleveraging” put upon the American (and overseas) labor force meant that revenue growth would remain low and lackluster, therefore keeping the re-hiring trend at a minimum wherein all prior recoveries had always been predicated upon it being at a maximum. And even when it appeared that recovery was at least plausible, those possibilities were always and very rudely interrupted by even more monetary problems (2011 banking, “rising dollar”).

The primary problem inherited by the incoming Trump administration is quite simple: there has been no wage growth. They surely know this, as it was the primary reason there is a Trump administration. The reasons for the lack of labor recovery, however, have little to do with what Trump might be able to do, except insofar as he could send Janet Yellen and all those empty suits like her to do more damage only in academia. He has recently declared his distaste for the “strong dollar”, which to me is a very bad sign; had he instead declared his distaste for the variability of the dollar (let alone the “dollar”) then we might have an open road to actual reflation.

Since we don’t really know what President Trump might do, it would be a mistake to be so declarative. But we should also make no mistake as to the scale and the true nature of the problem.