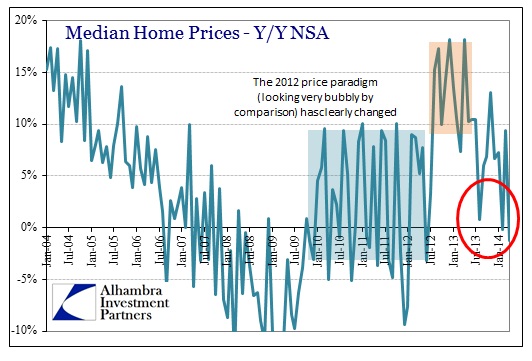

I often stand in amazement at what passes for conventional wisdom, or more precisely what is being attempted as such. Only one year ago the tendency to view the housing market as the next great growth engine was ubiquitous all across economic commentary. It had “clearly” and “unarguably” turned from a maddening headwind to a comforting tailwind. More than a little backslapping in policy quarters had taken place; victory laps and all that.

There was some growing discomfort with the pace of expansion, particularly in comparison with prior experience during the “obvious” bubble days, but such concerns were thought to be minor in the afterglow of “successful” QE. Going back further in time, the third episode and its adventure in MBS TBA was expressly offered for just that intent – to restart housing nearly from scratch.

Now the tune has changed dramatically, to the point of being unable to recognize those same conclusions. What was obvious last year has been lost and replaced with no end of contradiction.

“Mortgage financing is extremely tight,” said Ellen Zentner, senior economist at Morgan Stanley in New York. “And that’s not something the Fed can manipulate.”

How do you reconcile that statement with last year? The whole point of QE3 was to “loosen” mortgage finance to the point housing could be manipulated into an economic growth factor. The very mechanics of QE3 follow exactly that course, as it created an increase in spread (lower production coupons) that made lending in volume more profitable. That’s not something the Fed can manipulate? That was the entire point.

The trouble from the Fed’s perspective is that many of the forces holding housing back are outside of its control. While the Fed can influence mortgage rates through its conduct of monetary policy, it can’t do much, if anything, to counteract the other causes of faltering demand: lagging household formation, stingy lenders and wary borrowers.

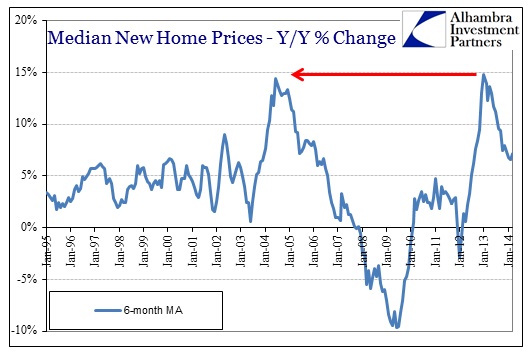

Those factors were readily evident last year too. Lenders were stingy then as lending standards have remained tight throughout; it is only recently that the GSE’s are being courted to reduce standards and head back toward bubble profligacy. Those wary borrowers were the exact opposite before May 2013, particularly in refis, attracted so because of the behavior of interest rates.

It is the inclusion of household formation that stands out here, however. All of these factors cited are common as remnants of past monetarism. The author of the article is blaming past monetarism for the failures of current monetarism, without acknowledging that it was current monetarism that changed the character of housing from last year to this year. The FOMC was nearly omniscient last year, but now is utterly helpless?

The tortured asset and housing markets are merely the expressions of using those channels for policy aims. And this is more than a little bit childish – when it moves in the “right” direction, the Fed meant to do it; when it moves in the “wrong” direction someone or something else is to blame. The real truth lies in interest rate targeting and the fusion of that with the desire to control “aggregate demand.” Destroying price signaling, as this “control” does (including artificial financial profit subsidies), renders “markets” overly susceptible to bubbling.

The current “helplessness” of the central bank is nothing more than the inevitable downside of its own experimentations.

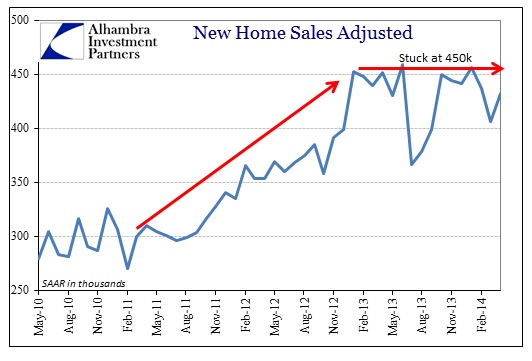

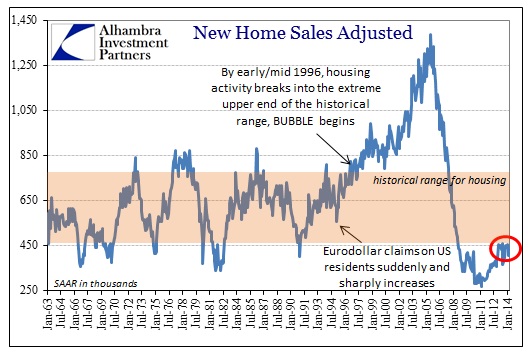

The pace of new home sales recently seems to have hit a ceiling.

It is more than a little curious that such a ceiling is located right at the bottom edge of what I would call the historical range. That provides as much evidence for a bubble as anything, since prices have advanced at a pace consistent with the middle of the last decade on only a fraction of the volume. In the grand scheme of the economy, that is actually fortunate in that the leftovers of the last bubble (household formation, lending standards) have actually prevented a wider misallocation. In other words, actual market forces are preventing policy aims from making it far, far worse once again. But to policymakers, that was a “drag” to be overcome.

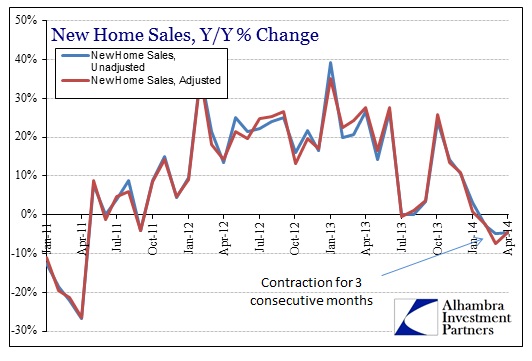

The problem for the rest of this year is whether or not those that have ignored actual market signals for the comfort of last year’s central bank “omniscience” will be forced to the exits in an orderly fashion; or whether recent signals from the “utterly helpless” part of the FOMC blame deflection apparatus will spark something more like disorder. The former will be unhelpful; the latter would be more than a small drag.

In any case, whether or not you feel the Fed is helpless here does not take away ownership of all of these zig zags tracing back into the 1990’s.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@alhambrapartners.com