NFIB Survey Suggests Weak Economic Prospects

Earlier this week, the National Federation of Independent Businesses released their monthly Small Business Survey. While this data is much overlooked by the mainstream media, it really shouldn’t be. Out of the 26 million businesses registered in the United States, only 6 million have active employment and generate revenue. Of that total, almost 80% have fewer than 5-employees. Simply, it is small businesses that drive the economy, employment, and wages. Therefore, what the NFIB says is extremely relevant to what is happening in the actual economy versus the headline economic data from Government sources.

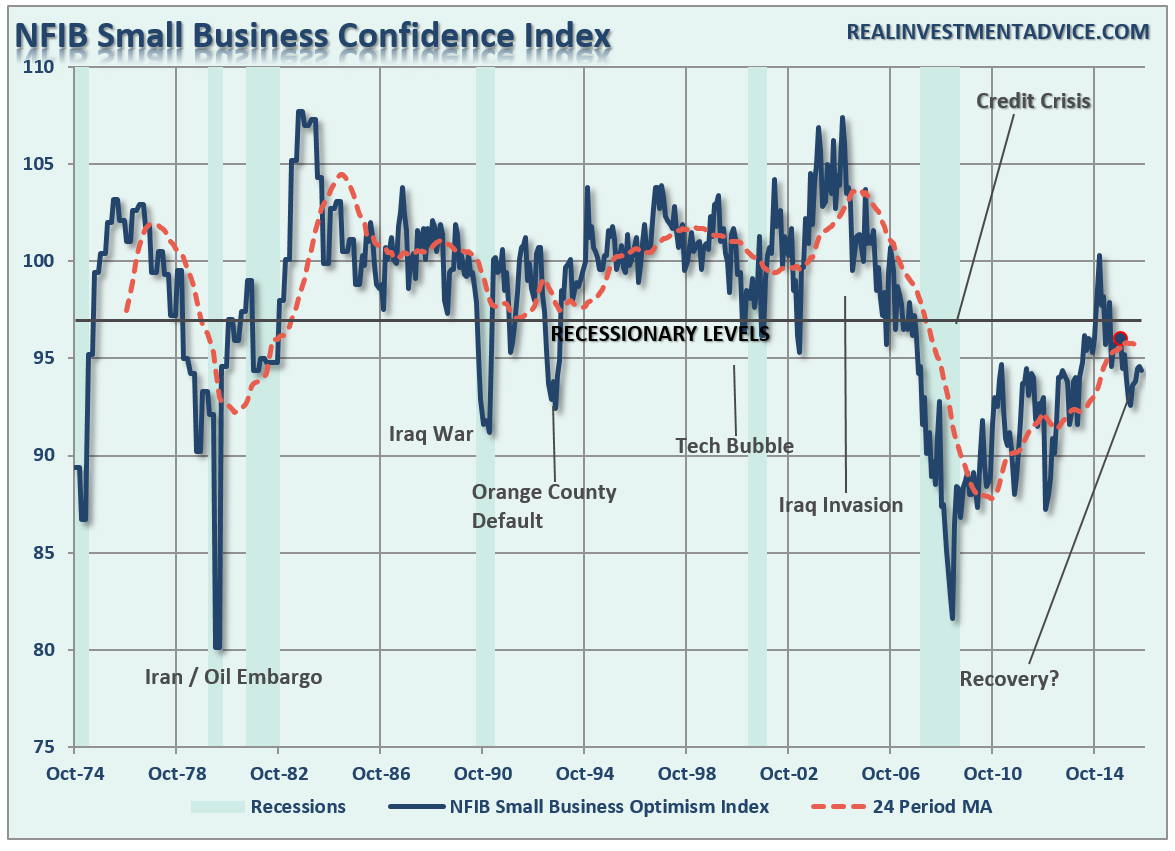

In August, the survey declined 2-tenths of a point to 94.4. While that may not sound like much, it is where the deterioration occurred that is most important. Furthermore, despite an improvement from the financial crisis lows, the current levels are still well below the levels normally witnessed at the late stage of an economic recovery.

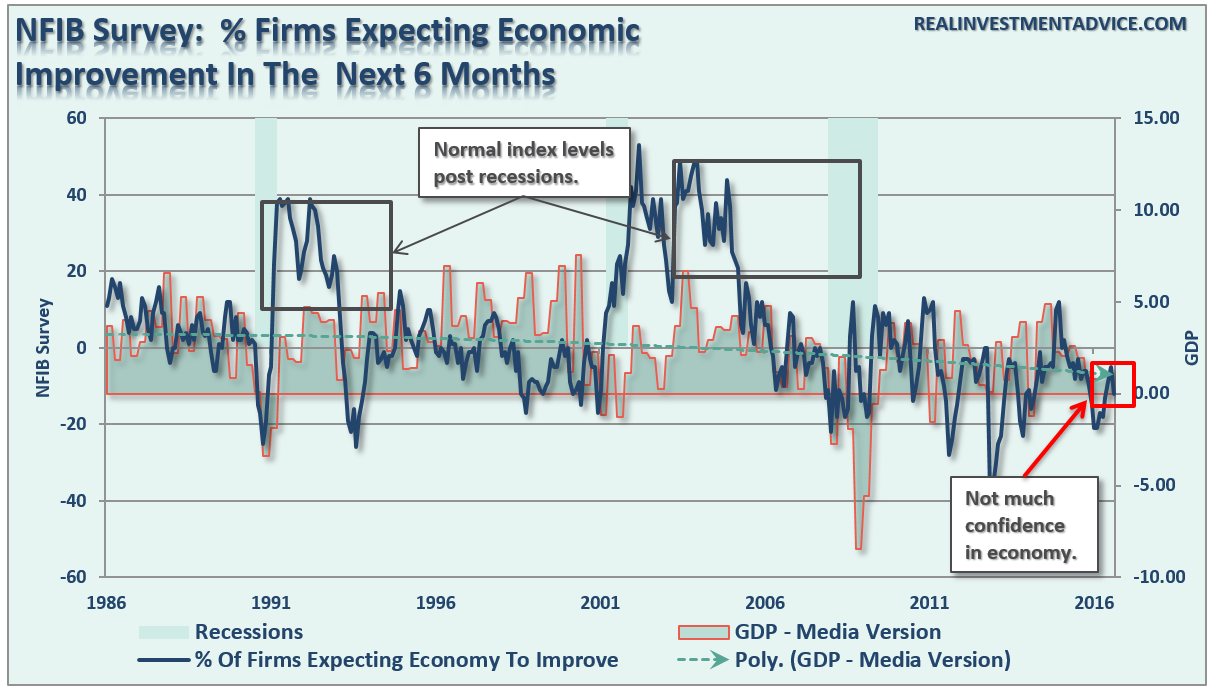

As noted in the chart below, the surge in optimism has now returned the survey to levels normally associated with the onset of recessions. And it only took 8-years to get there, hardly a recovery to “crow” about.

However, the internals of the report were much less exuberant as noted by the NFIB:

“Once again, the NFIB survey showed no signs of strength in the small business sector. Uncertainty seems to be the major enemy of economic progress and the political climate is a major contributor to the high levels of uncertainty that we’ve seen. The current economic environment is not a good one for strong or sustained growth.”

This certainly isn’t the message that we are getting from the mainstream media suggesting all is well within the economy. But, here are the interesting highlights:

- The outlook for business conditions in the next six months had the most dramatic change, dropping seven points.

- Setting an all-time high for the survey, 39 percent of business owners cited the political climate as a reason NOT to expand.

- Uncertainty about the economy and government policy also hit record highs among small business owners.

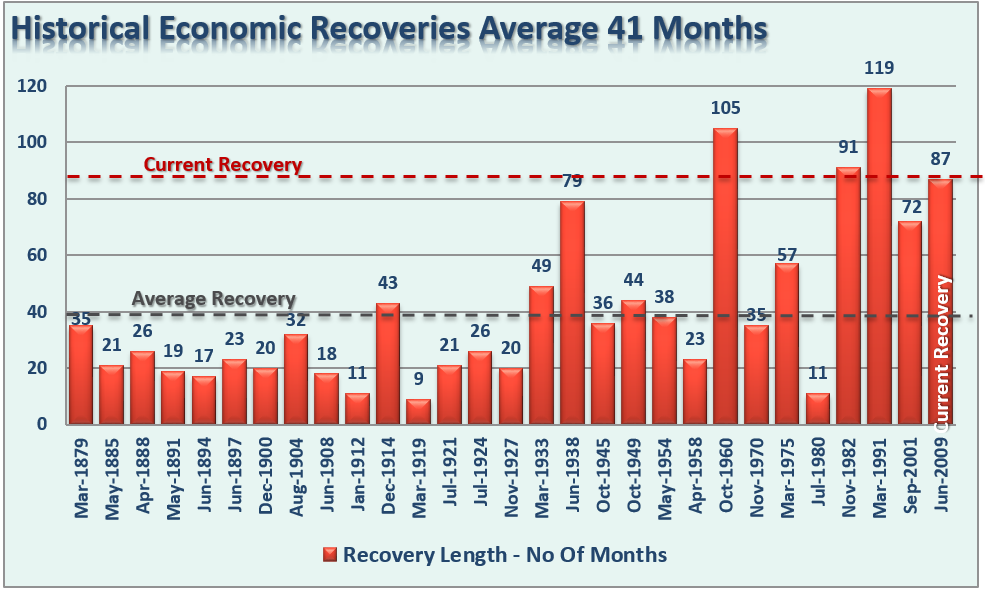

The issue, despite all evidence the contrary, remains a prevailing “blindness” to the reality of economic cycles. Economic recoveries are finite and by all measures the current economic recovery has been very long when considering this is the 4th longest expansion in history with the lowest overall rate of growth.

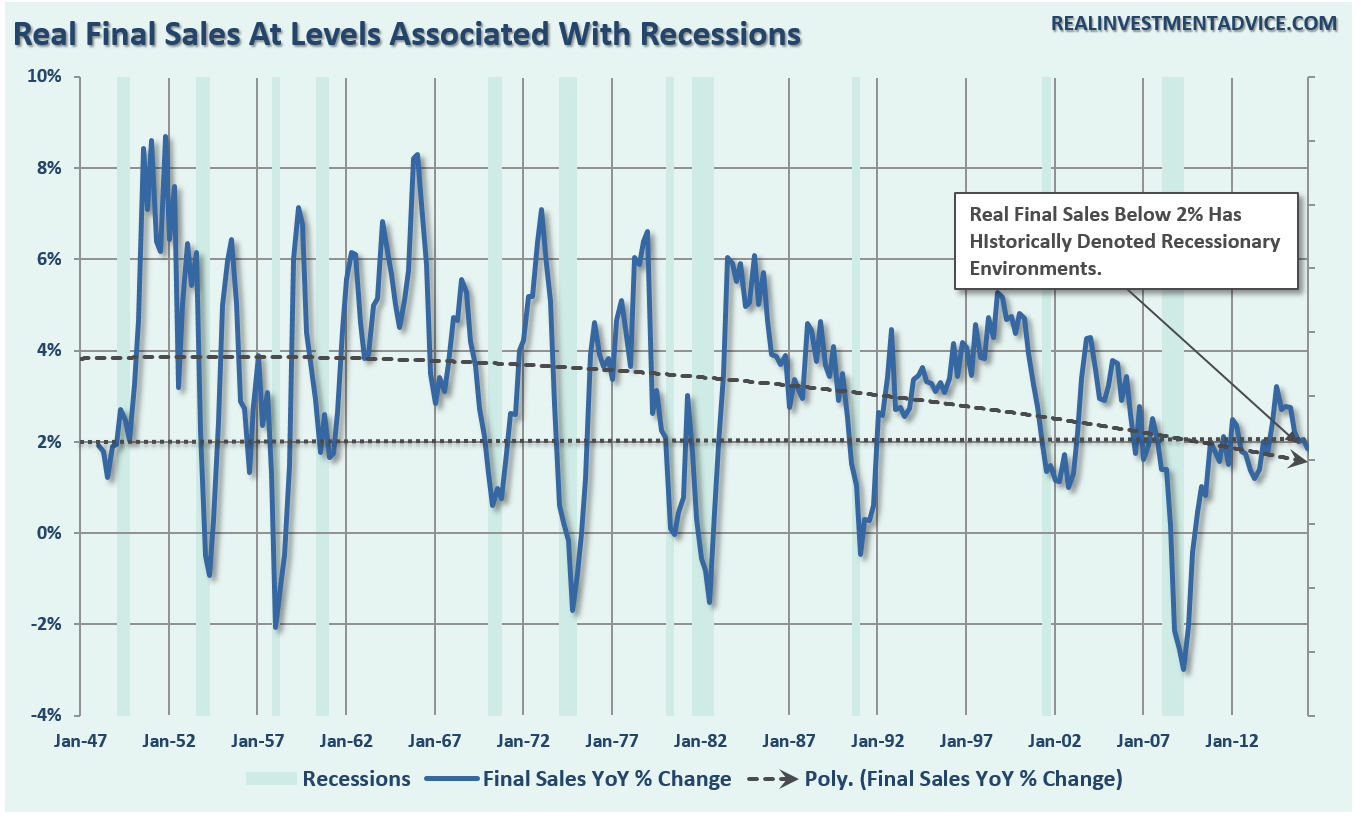

While longer periods of economic expansion have certainly existed, the underpinnings of those expansions are substantially different than what exists currently. The chart of real, inflation-adjusted, final sales exposes this issue.

During previous expansions, real final sales in the economy ran at 4% annualized growth rates or better. The current expansion from the 2009 lows only briefly touched 3% despite massive Government and Federal Reserve interventions.

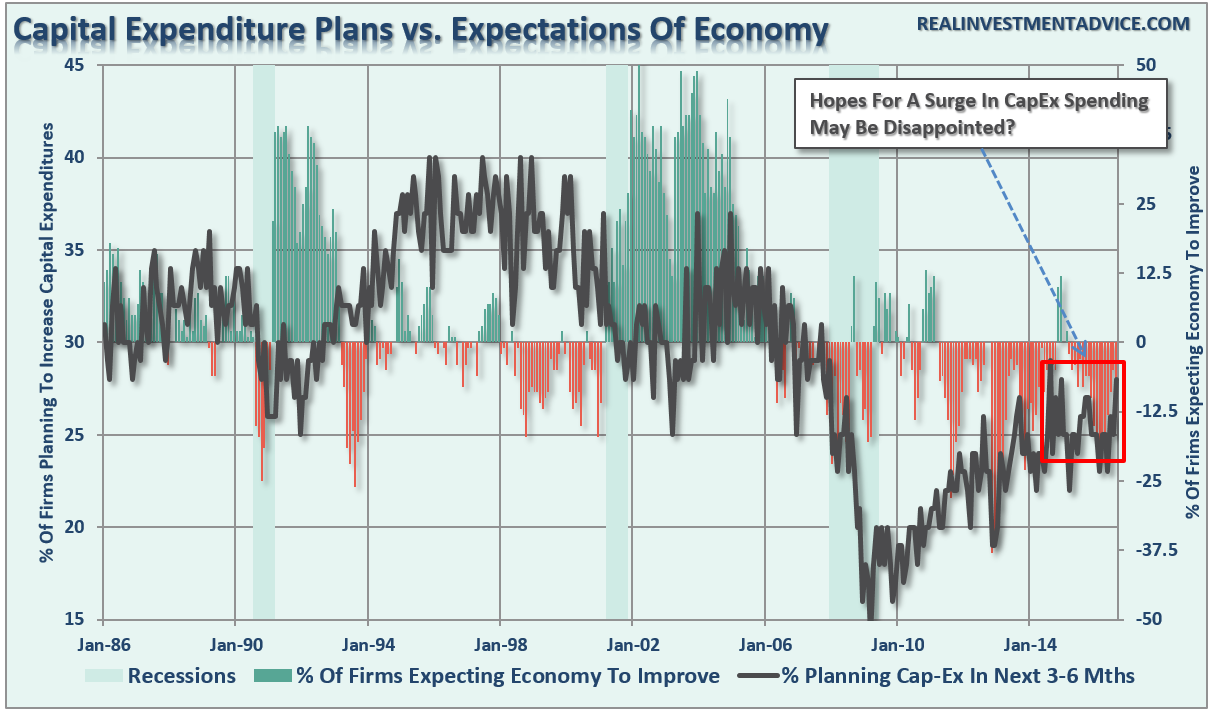

However, one of the hopes that continues to drive economic expectations is a return of capital spending to supplant the dearth of consumer spending. The problem is that corporate CapEs, as a percentage of economic growth, is far less than the nearly 70% contribution made up by consumers. The problem, as shown in the chart below, is despite hopes of a surge in capital spending, plans for such expenditures remains very retarded and at levels, not surprisingly, normally associated with recessionary environments.

Importantly, expectations are very fragile. Any stumble in the current environment will see those expectations quickly reverse. The chart above shows expectations of economic improvement (currently at -12%, down from -5% in July) as compared to plans for capital expenditures over the next 3-6 months (currently at 28% which is where it was January of 2015).

If small businesses were convinced that the economy was “actually” improving over the longer term, they would be increasing capital expenditure plans rather than remaining at the same level they were 20-months ago. The disparity between improved economic outlook and CapEx plans is likely a reflection that business owners are hoping for increased economic activity. However, they are not willing to ‘bet’ their capital on it.

This is easy to see when you compare business owner’s economic outlook as compared to economic growth. Not surprisingly there is a high correlation between the two given the fact that business owners are the “boots on the ground” for the economy. Importantly, their current outlook does not support the ideas of stronger economic growth into the end of the year.

Of course, the Federal Reserve has been absolutely NO help in instilling confidence in small business owners to deploy capital into the economy. As NFIB’s Chief Economist Bill Dunkleberg stated:

“The Federal Reserve has started its regular ‘hide the rate hike’ game, sending observers looking under every rock of data to see if there are 25 basis points underneath. Most of the ‘rocks’ look like pebbles, there’s not a lot of growth in the landscape, and there’s that darn international thing, the value of the dollar (which is officially not the province of the Fed) and all that. The inflation and employment goals are defined ‘downward’ in terms of what the Fed might accept, along with prognostications that assure ‘full’ attainment by 2018. Comments by Chicago Fed president Charles Evans, in remarks to the Shanghai Advanced Institute of Finance in Beijing, indicate that the Fed thinks it is the determining force shaping interest rates, not markets, a very troubling view. He said:

‘Long-run expectations for policy rates provide an anchor to long-run interest rates. So lower policy rate expectations act as a restraint on how much long-term rates could rise following a surprise over the near-term policy path.’

These contortions in policy cannot be maintained. We will regret this arrogance even more over the next decade as our private financial institutions become unable to meet the promises they have made.”

The Real Employment Report

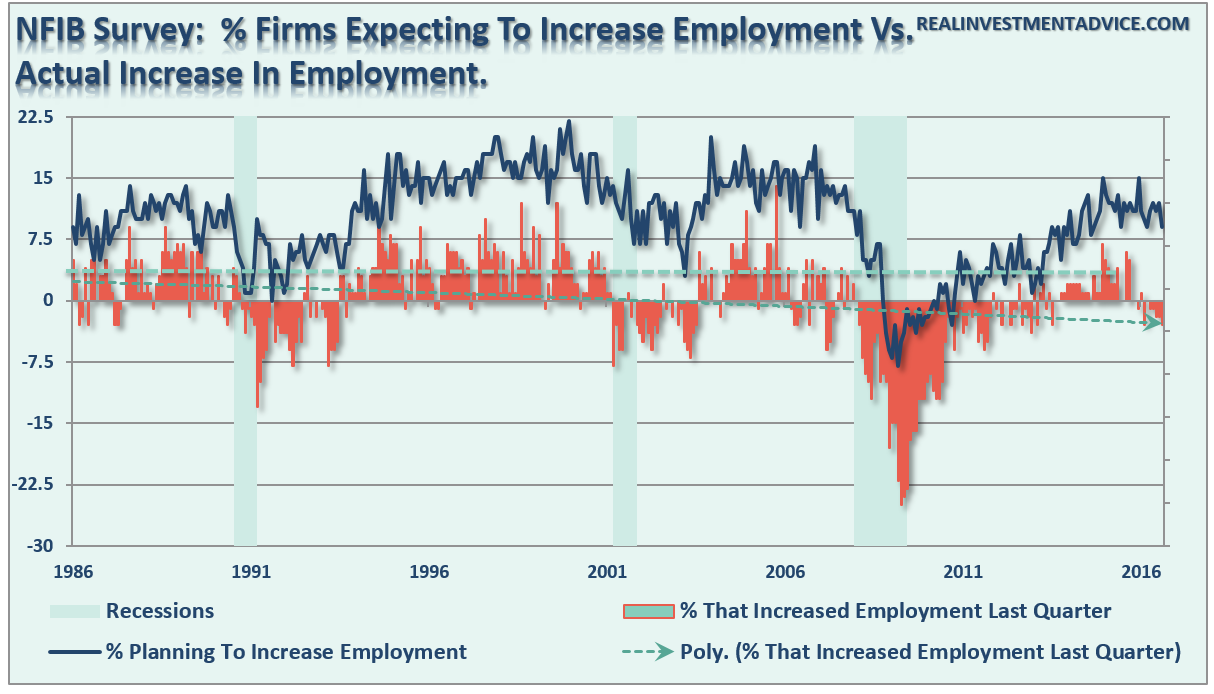

The divergence between the Fed’s “economic fantasy” and “Main Street reality” can also be seen between expectations to increase employment versus those that actually did.

Three months ago, the percentage of respondents that were expecting to increase employment over the next quarter, or two, rang in at 11%. Three months later, the percentage of respondents that increased employment was -3%. This currently is the lowest level of hiring since January of this year and greatly contrasts the stats produced by the BLS showing large month gains every month in employment data. While “expectations” should be “leading” action, this has not been the case.

The first chart below shows the raw data of how firms feel “today” about increasing employment over the next three months versus actual increases in employment over the last quarter.

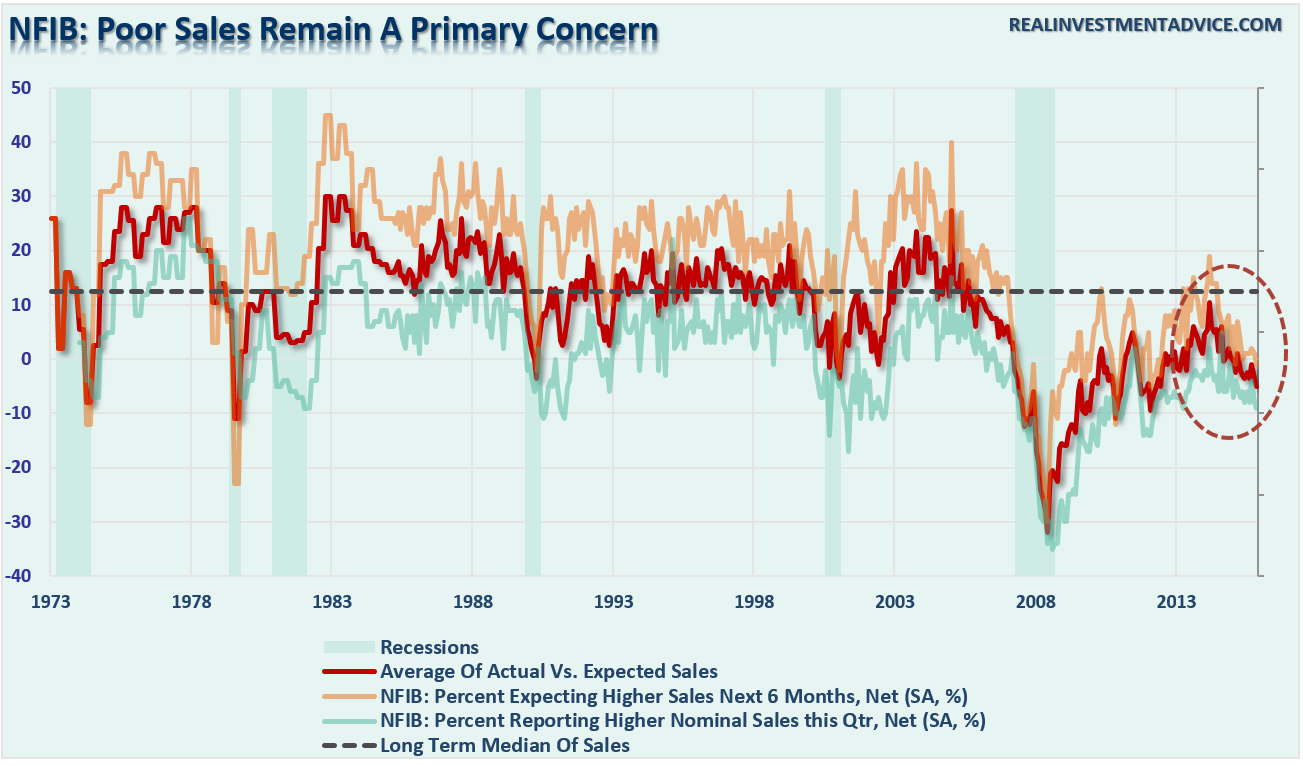

The divergence between expectations and reality can also be seen in actual sales versus expectations of increased sales. Employers do not hire just for the sake of hiring. Employees are one of the highest costs associated with any enterprise. Therefore, hiring takes place when there is an expectation of an increase in demand for a company’s product or services.

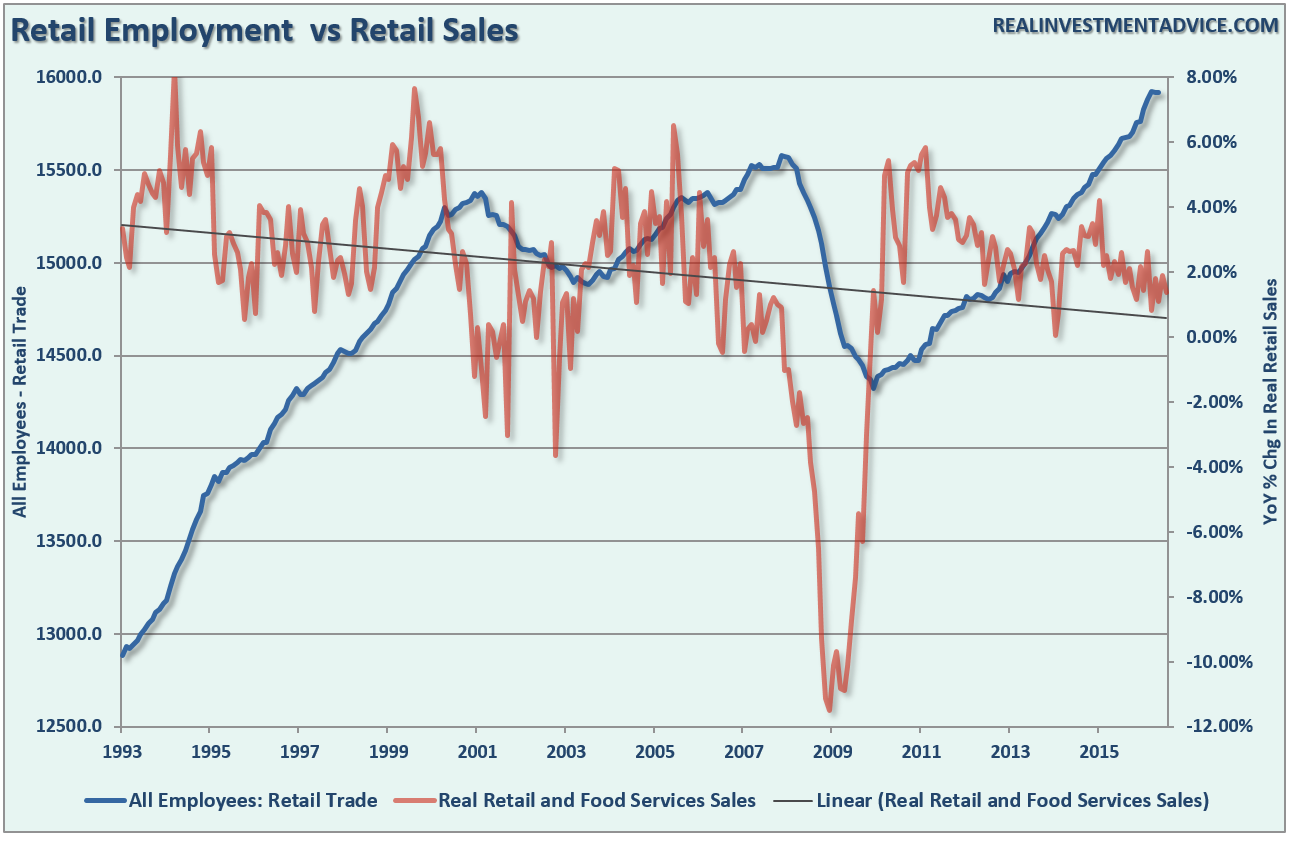

This is also one of the great dichotomies of the employment reports that continues to show strong hiring in retail services despite a weakening outlook for, and actual, retail sales.

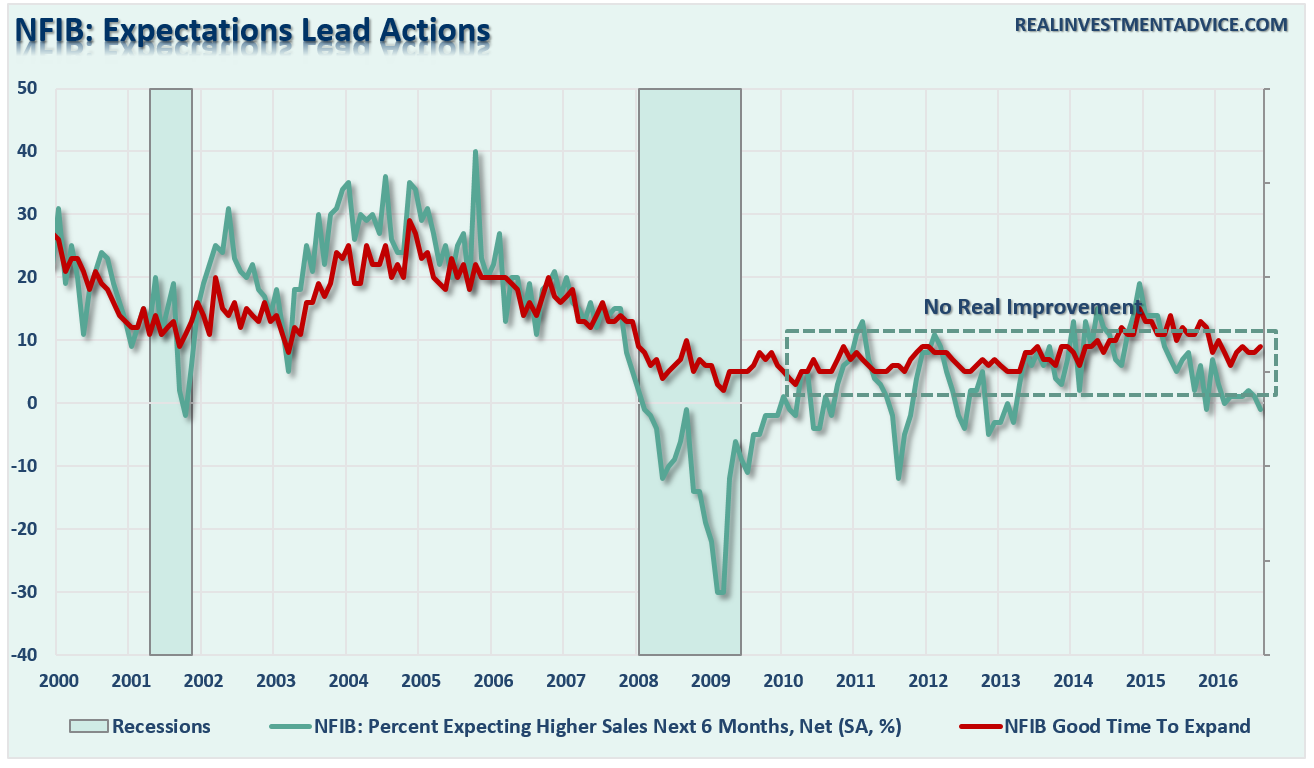

Furthermore, despite hopes of continued debt-driven consumption, business owners are still faced with actual sales that are still well below long-term trends. Since revenue is what ultimately drives expansion, it is not surprising that when asked whether this is a “good time to expand” their operations, the large majority of responses remain negative. That view has remained unchanged since the depths of the financial crisis.

It’s The Government, Man!

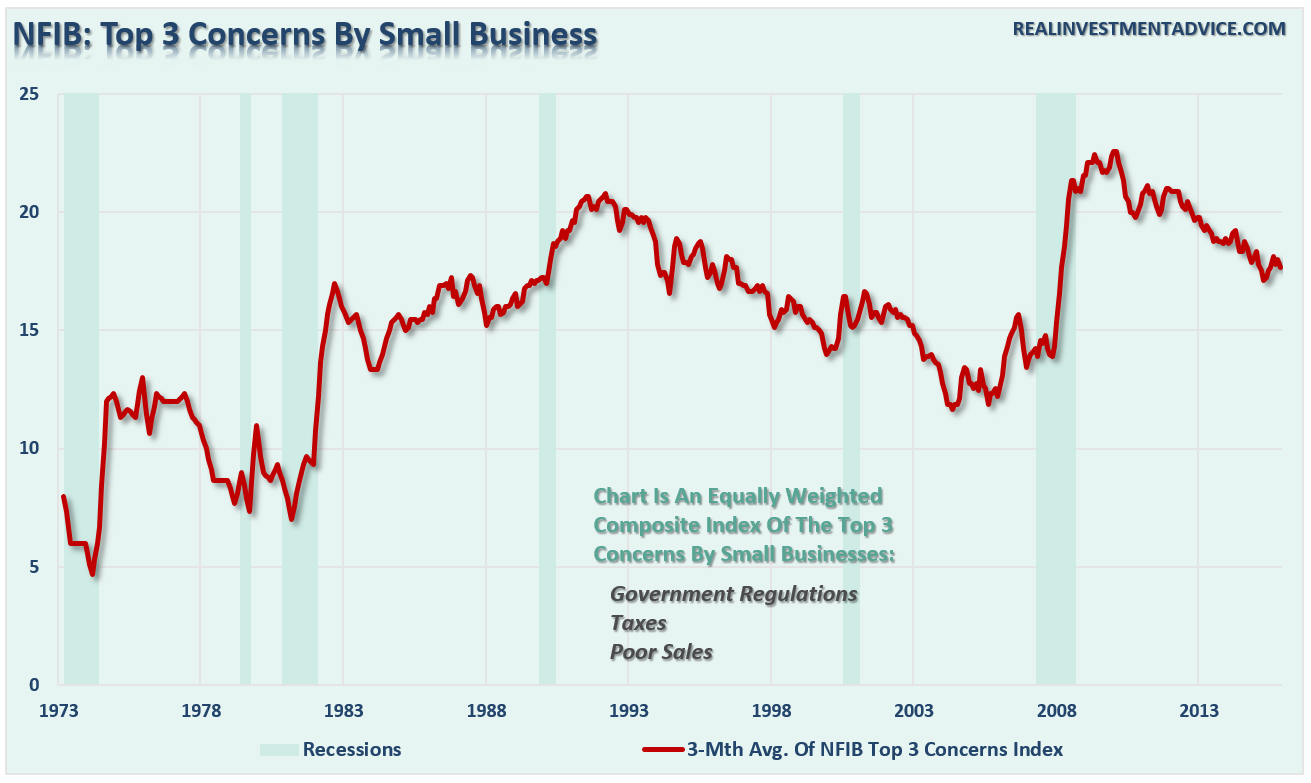

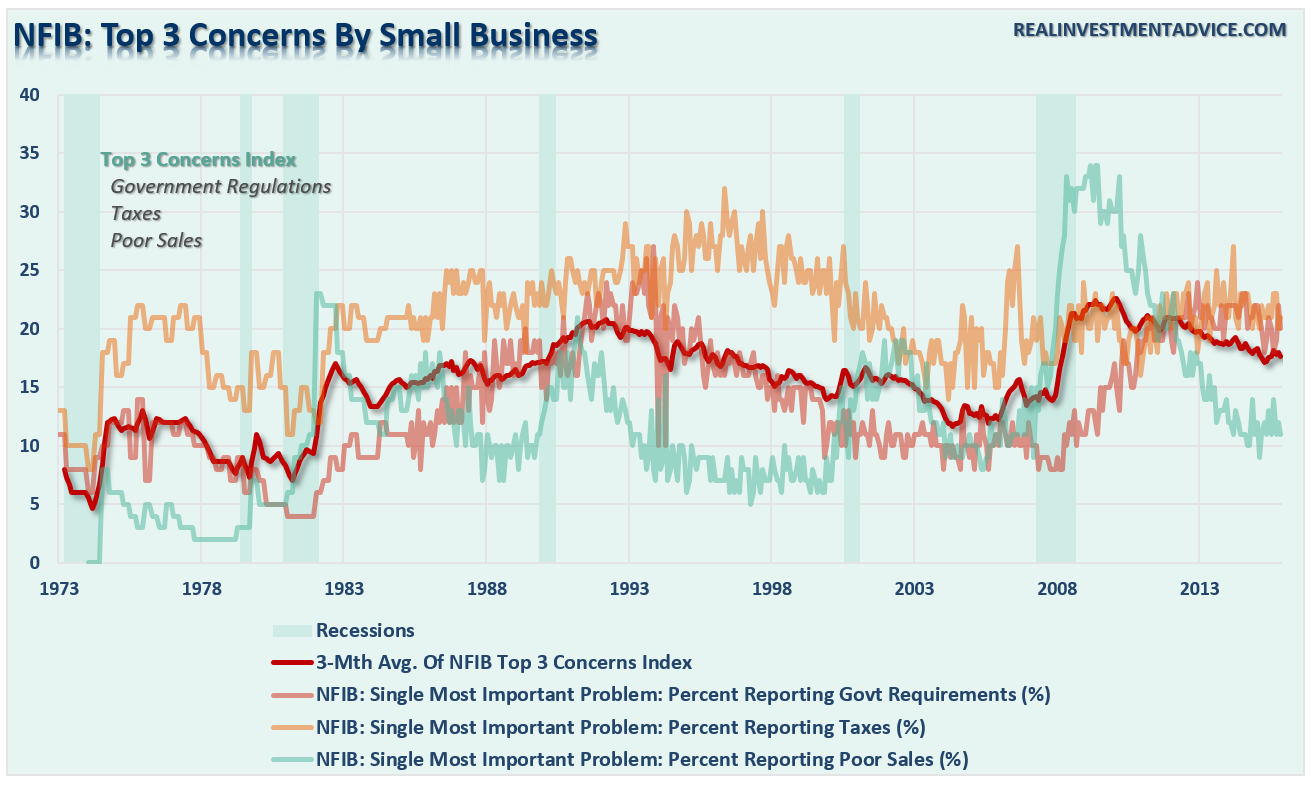

For small businesses, the overall environment remains very challenging. The top 3 concerns of small businesses remain government regulations, taxes and poor sales as shown by the composite indicator below. While improved somewhat from the financial crisis, levels remain well entrenched at levels where recessions are starting, not eight years into an expansion.

Increased regulations, the onset of the Affordable Care Act (ACA), increased taxes (due to the ACA), and increased costs of compliance keep budgets tight with profitability a primary focus. Taxes and Government Regulations continued to be at the forefront of the decision-making process by business owners.

With small business optimism waning currently, combined with many broader economic measures, it suggests the risk of a recession has risen in recent months.

As I discussed previously, the gap between incomes and the cost of living is once again being filled by debt. However, using credit to maintain a standard of living is far different that using debt to increase it. This is why consumptions expenditures are weak and “final demand” in the economy remains anemic. In turn, business owners remain on the defensive, reacting to increases in demand caused by population growth rather than building in anticipation of stronger economic activity.

Lastly, as Bill notes, some of the increases we have seen in spending and wages have come at the expense of economic growth rather than a benefit from it.

“Health insurance costs keep rising, diverting compensation gains into benefits rather than take home pay. Other regulatory pressures such as a rising minimum wage and mandatory paid leave also put an upward pressure on reports of compensation increases. Capital spending will remain M.I.A., plans are at the highest level for the recovery, matching the previous peak in 2014, but not typical of an expansion and reports of actual spending have been weakening.”

What this suggests is that the current “struggle through” economy will likely continue until some unexpected exogenous shock tips the proverbial “apple cart.”

The problem for the Fed is that once again the window for a “rate hike” has likely closed. Economic uncertainty, deflationary threats, and market volatility will keep them boxed in for now. Unfortunately, the recent spike in LIBOR has likely already done a bigger job of tightening monetary policy than the Fed actually intended to do. This could cause problems in the not too distant future.

Just some things I am thinking about.