With roughly 97% of the S&P 500 having reported earnings, as of the end of August, we can take a closer look at the results through the 2nd quarter of the year. Despite the exuberance from the media over the “number of companies that beat estimates” during the most recent reported period, 12-month operating earnings per share FELL from $98.61 per share in Q1 to $98.33 which translates into a quarterly decrease of 0.2%. While operating earnings are widely discussed by analysts and the general media; there are many problems with the way in which these earnings are derived due to one-time charges, inclusion/exclusion of material events, and outright manipulation to “beat earnings.”

Therefore, from a historical valuation perspective, reported earnings are much more relevant in determining market over/undervaluation levels. It is from this perspective the news improved modestly as 12-month reported earnings per share rose from $86.44 in Q1 to $86.99, or 0.6% in Q2. However, despite the improvement in reported earnings for the quarter, the trend remains clearly negative.

Always Optimistic

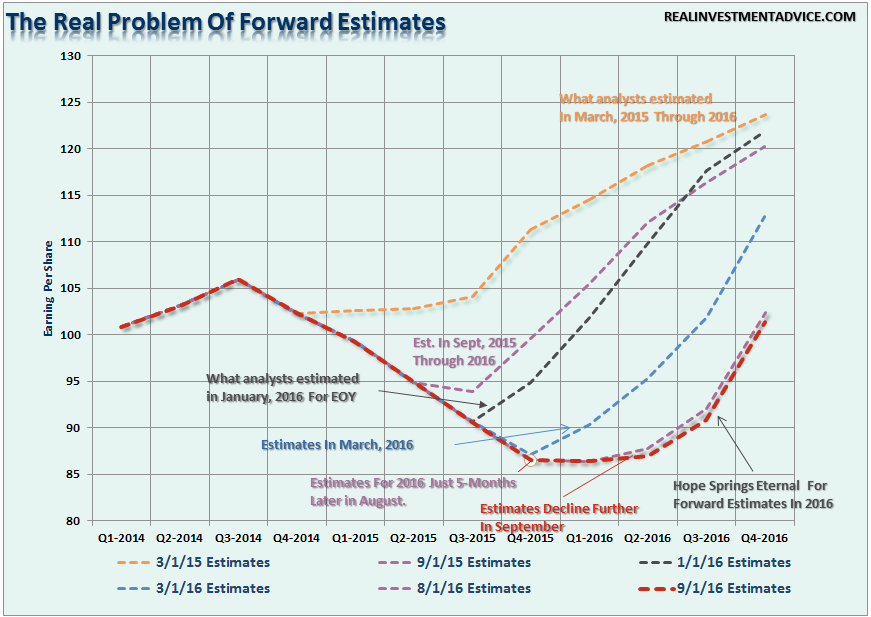

There is one commodity that Wall Street always has in abundance, “optimism.” When it comes to earnings expectations, estimates are always higher regardless of the trends of economic data. The problem is that the difference between expectations and reality have been quite dramatic.

The game is simple:

“Lower the earnings bar until companies can beat earnings to justify the ‘buy’ the bullish meme.”

Notice in the chart above that in just the last month forward earnings expectations have been lowered further for the year. The downward slide of earnings expectations over the last several months can be more clearly seen in the chart below.

Earnings Manipulation Reaching Limits

There is no arguing corporate profitability improved in the last quarter as oil prices recovered. The recovery in oil prices specifically helped sectors tied to the commodity such as Energy, Basic Materials, and Industrials. However, such a recovery may be fleeting as the dollar remains persistently strong which continues to weigh on exports and the recovery in commodity prices continues to remain muted as the global economy remains weak.

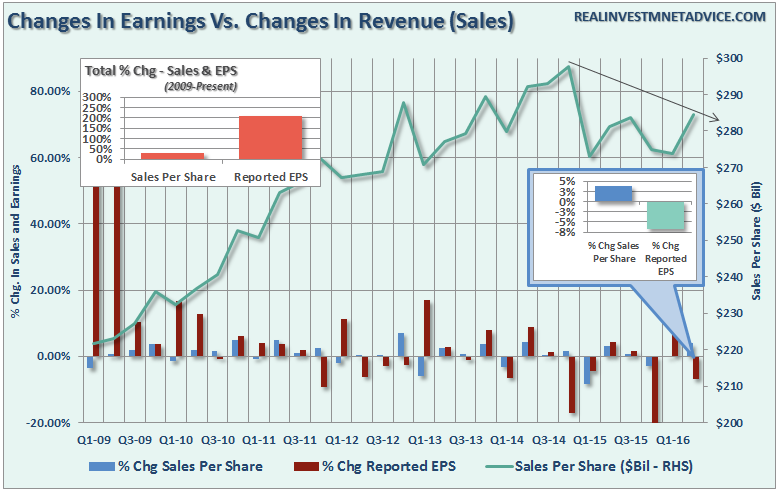

However, looking back it is interesting to see that much of the rise in “profitability” since the recessionary lows has come from a variety of cost-cutting measures and accounting gimmicks rather than actual increases in top line revenue. As shown in the chart below, there has been a stunning surge in corporate profitability despite a lack of revenue growth. Since 2009, the reported earnings per share of corporations has increased by a total of 211%. This is the sharpest post-recession rise in reported EPS in history. However, that sharp increase in earnings did not come from revenue which is reported at the top line of the income statement. Revenue from sales of goods and services has only increased by a marginal 28% during the same period.

In order for profitability to surge, despite rather weak revenue growth, corporations have resorted to four primary weapons: wage reduction, productivity increases, labor suppression and stock buybacks. The problem is that each of these tools creates a mirage of corporate profitability which masks the real underlying weakness of the overall economic environment. The problem, however, is that each of the tools used to boost EPS suffer from diminishing rates of return over time.

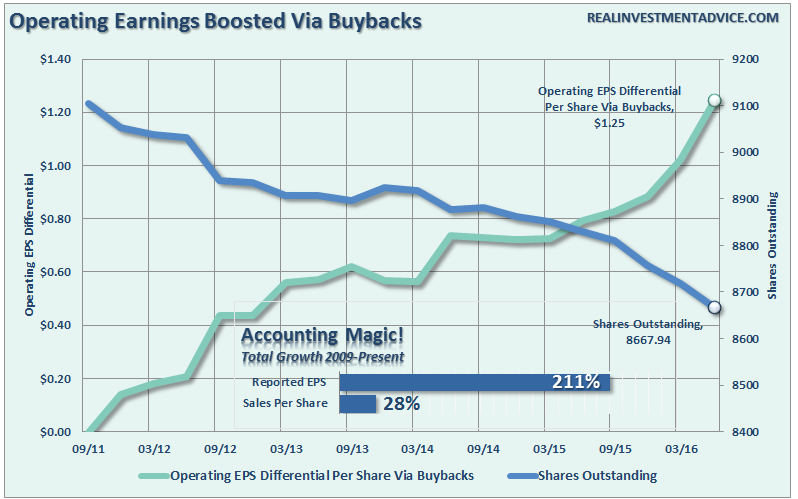

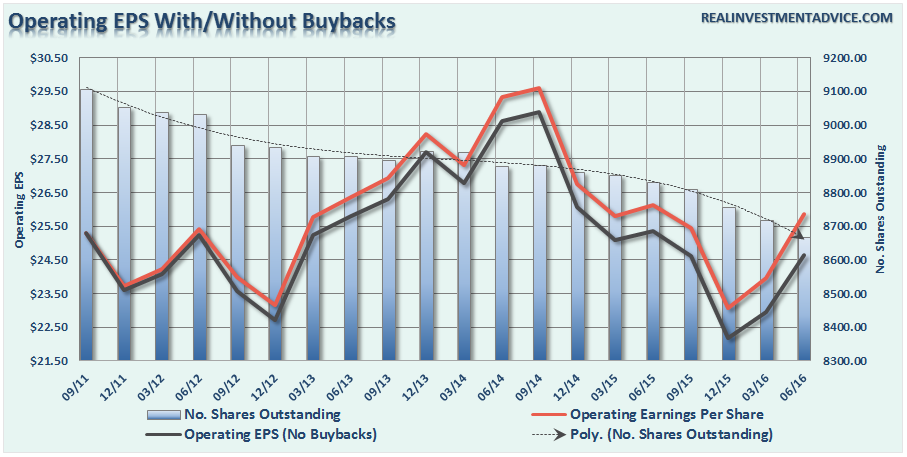

One of the primary tools used by businesses to increase profitability has been the accelerated use of stock buybacks. The chart below shows the total number of outstanding shares as compared to the difference between operating earnings on a per/share basis before and after buybacks.

The reality is that stock buybacks create an illusion of profitability. If a company earns $0.90 per share and has one million shares outstanding – reducing those shares to 900,000 will increase earnings per share to $1.00. No additional revenue was created, no more product was sold, it is simply accounting magic. Such activities do not spur economic growth or generate real wealth for shareholders. However, it does provide the basis for with which to keep Wall Street satisfied and stock option compensated executives happy.

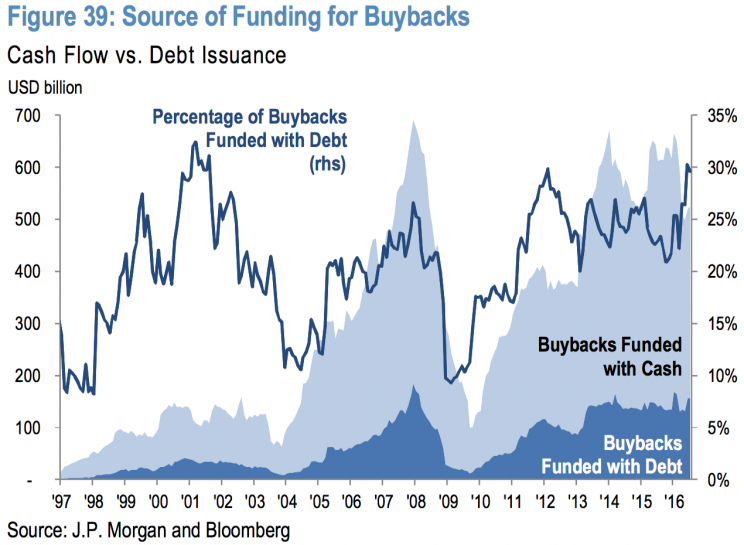

It is also worth noting the level of stock buybacks financed by debt has also reached previous peak levels. According to JP Morgan:

“S&P 500 companies announced 141 new buyback programs YTD with an aggregate dollar value of $327 billion. 39% of repurchases YTD were funded by issuing new debt versus 22% in 2015.”

Furthermore, while the majority of buybacks have been done with cash it just goes to show how much cash has been used to boost earnings versus expanding production, making productive acquisitions or returning cash to shareholders.

Ultimately, the problem with cost cutting, wage suppression, labor hoarding and stock buybacks, along with a myriad of accounting gimmicks, is that there is a finite limit to their effectiveness. Eventually, you simply run out of people to fire, costs to cut and the ability to reduce labor costs. The last point is most prevalent as I discussed previously:

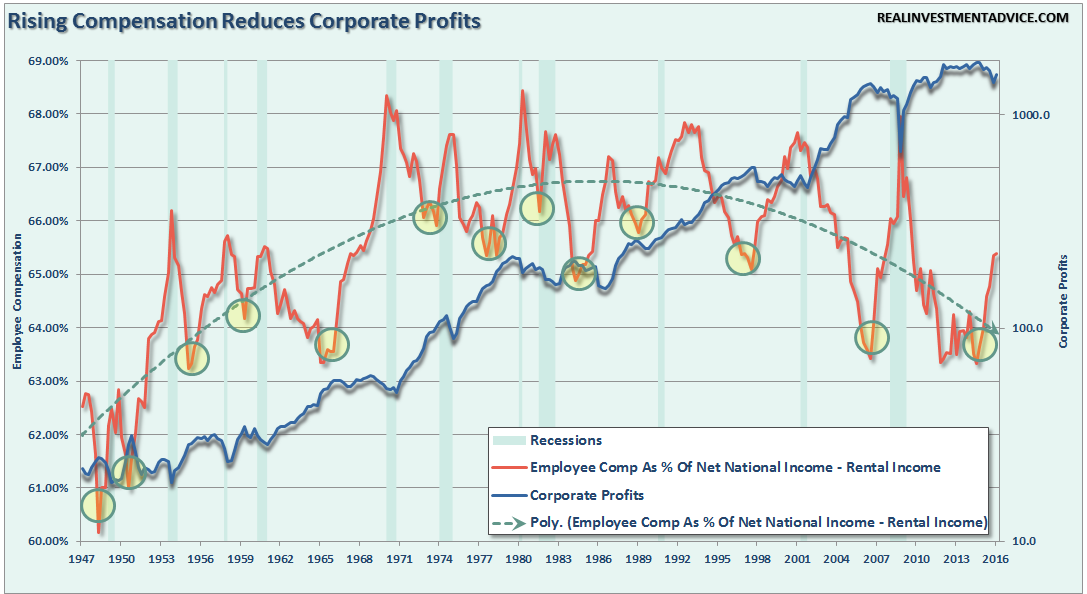

“While there are many hopes of an end to the current ‘profits’ recession, there is mounting evidence those hopes may once again be disappointed. One of the latest such indications is rising employee compensation.

While rising employee compensation is good from the view it should lead to rising consumption, it also reduces corporate profitability (wages reduce profits.) Furthermore, this is especially problematic currently as rising compensation is being offset by soaring healthcare costs due to the Affordable Care Act.”

“Like jobless claims, which hit historically low levels prior to recessions (see here), rising employee compensation has also denoted turns in economic growth and has preceded the onset of recessionary economic drags.”

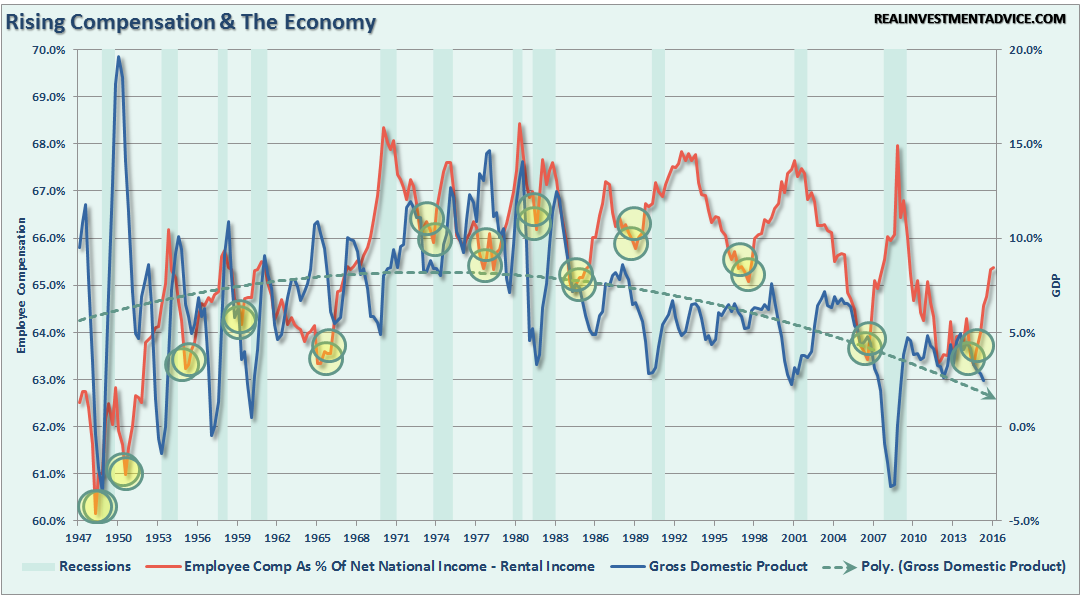

“It is worth noting that in both charts above, despite hopes of continued economic expansion, both employee compensation, and economic growth have continued to trend to lower since the 1980’s. This declining growth trend has been compensated for by soaring levels of debt to sustain the current standard of living.”

Economics Matter

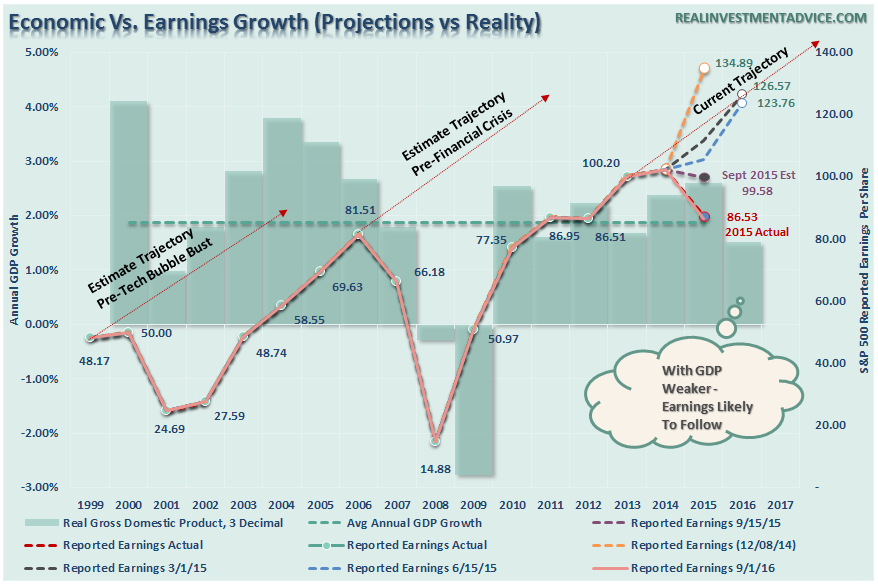

The chart below compares economic growth to earnings growth. Wall Street has always extrapolated earnings growth indefinitely into the future without taking into account the effects of the normal economic and business cycles. This was the same in 2000 and in 2007. Unfortunately, the economy neither forgets, nor forgives.

With analysts once again hoping for a “hockey stick” recovery in earnings in the months ahead, it is worth noting this has always been the case. Currently, there are few, if any, Wall Street analysts expecting a recession at any point the future. Unfortunately, it is just a function of time until the recession occurs and earnings fall in tandem.

There is virtually no “bullish” argument that will currently withstand real scrutiny. Yield analysis is flawed because of the artificial interest rate suppression. It is the same for equity risk premium analysis. Valuations are not cheap, and increase in interest rates by the Fed will only act as a further brake on economic growth.

However, because optimistic analysis supports our underlying psychological “greed”, all real scrutiny to the contrary tends to be dismissed. Unfortunately, it is this “willful blindness” that eventually leads to a dislocation in the markets.

The deterioration in earnings is something worth watching closely. While earnings have improved in the recent quarter, modestly mind you, it is likely transient given the late stage of the current economic cycle, continued strength in the dollar and potentially weaker commodity prices in the future.

Lastly, with stock buybacks slowing and corporate cost cutting now running in reverse, overly optimistic expectations may continue to be in jeopardy.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In