By Tyler Durden at ZeroHedge

Back in August 2012, when negative interest rates were still merely viewed as sheer monetary lunacy instead of pervasive global monetary reality that has pushed over $6 trillion in global bonds into negative yield territory, the NY Fed mused hypothetically about negative rates and wrote “Be Careful What You Wish For” saying that “if rates go negative, the U.S. Treasury Department’s Bureau of Engraving and Printing will likely be called upon to print a lot more currency as individuals and small businesses substitute cash for at least some of their bank balances.“

Well, maybe not… especially if physical currency is gradually phased out in favor of some digital currency “equivalent” as so many “erudite economists” and corporate media have suggested recently, for the simple reason that in a world of negative rates, physical currency – just like physical gold – provides a convenient loophole to the financial repression of keeping one’s savings in digital form in a bank where said savings are taxed at -0.1%, or -1% or -10% or more per year by a central bank and government both hoping to force consumers to spend instead of save.

For now cash is still legal, and NIRP – while a reality for the banks – has yet to be fully passed on to depositors.

The bigger problem is that in all countries that have launched NIRP, instead of forcing spending precisely the opposite has happened: as we showed last October, when Bank of America looked at savings patterns in European nations with NIRP, instead of facilitating spending, what has happened is precisely the opposite: “as the BIS have highlighted, ultra-low rates may perversely be driving a greater propensity for consumers to save as retirement income becomes more uncertain.”

Call it another massive error on behalf of Keynesian central planners who once again fail to appreciate the nuances of the common sense and the liquidity preference of ordinary consumers.

However, just because negative rates have not been passed on to savers yet or just because cash still has not been made illegal, that doesn’t mean it won’t be.

The question at this point is twofold: what happens after the savings of ordinary depositors in the bank officially taxed and/or cash becomes phased out, and more importantly, what happens just before.

In other words, will there be a run on physical cash?

The truth is that if society panics and there is a full blown rush out of existing electronic bank deposits and into physical currency to avoid negative rate taxation, only those who panic first will be safe. Why? Because of the “magic” of fractional reserve banking – there is simply not enough physical currency in circulation to satisfy all savers’ claims.

Here is HSBC’s Steven Major trying to explain the problem:

Based on the evidence so far, households have not rushed to withdraw cash and put it into a safe or, more significantly, pay for someone else to store it for them. This is because retail deposit rates have stayed at or above zero as banks have opted to not pass the lower market rates on.

The assumption that bank deposits can be rapidly converted into cash does not hold up, in our opinion. If everybody wanted to take their cash out of the bank at the same time, the system would soon run out as there are simply not enough notes in circulation. It would take a considerable time to print the currency needed to meet the demand. A central bank could enforce a negative rate for a considerable period of time under these conditions. For example, in the US, even if the production rate is doubled – and assuming the pace of retirement of old notes is unchanged and there is demand for USD3trn of new notes – printing would take 20-years.

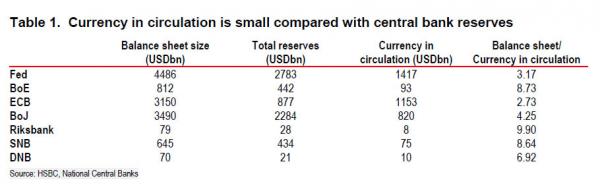

To explain this, consider the demand for currency created if savers tried to remove cash from the US banking system. This demand could total anything between USD2.5trn (of excess reserves) and USD4.5trn (the Fed’s total balance sheet). Currently there is USD1.5trn of currency in circulation and the total annual production had a face value USD149bn in 2014, suggesting the 20 years it would take to print the cash.

Currency in circulation is small compared to the potential demand in a negative rate environment. As an example, the Fed’s assets are three times the currency in circulation and the Riksbank’s nearly ten times (see Table 1), but production capacity is limited.

While largely correct, Major is wrong about two critical things.

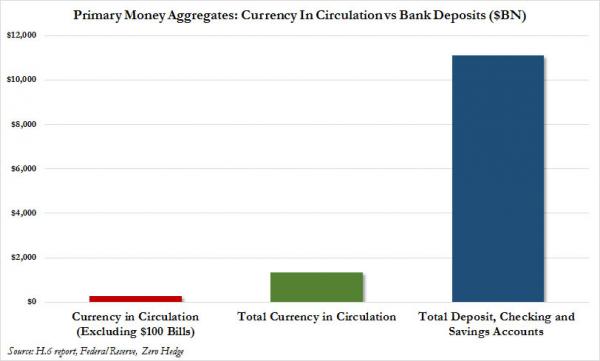

First, when estimating the potential demand for physical currency in circulation, one has to take into consideration not only the amount of total Fed reserves (or its entire balance sheet) but the entire fractional reserve banking system, and specifically the amount of paperless deposits parked at banks in the form of demand, checking, and savings account, or in other words, all the core components of M2. Not only that, but one must also consider the threat by increasingly more economists that large denomination bills may be outlawed, first in Europe with the €500 bill and then in the US with the $100 bill.

What a ban of Ben ($100 bill) would imply is that the total notional value of US currency in circulation would plunge from $1.35 trillion in the most recent week, to just $271 billion once the total $1.08 trillion value of $100 bills is eliminated. Putting this in context, there are as of this moment, $11.1 trillion in various forms of savings parked at banks as summarized in the chart below.

For the sake of simplicity, this analysis ignores what would happen globally in a comparable scenario in which paper currency in other developed markets is likewise “curbed” in part or in whole. Recall that for NIRP to truly work, paper currency has to be substantially eliminated everywhere it is implemented. We will analyze the impact of a global rush into paper currency in a subsequent post.

Still, what the chart above shows is that if, and when, a run on physical cash begins, there will be roughly $1 dollar in physical to satisfy $10 dollars in savers’ claims, a ratio which drops to 20 cents of “deliverable” cash if the $100 bill is taken out of circulation.

* * *

The second, and far more critical error Major makes, is the assumption that “households have not rushed to withdraw cash and put it into a safe.” As we explained previously, while this may have been true for a long time since 2014 when the first cases of NIRP were unveiled, that is no longer the case. Recall from “Safes Sell Out In Japan, 1,000 Franc Note Demand Soars As NIRP Triggers Cash Hoarding“

Now that the cash ban calls have gotten sufficiently loud to be heard by the generally clueless masses and now that the likes of Jose Canseco are shouting about negative rates, savers are beginning to pull their money out of the banks.

“Look no further than Japan’s hardware stores for a worrying new sign that consumers are hoarding cash–the opposite of what the Bank of Japan had hoped when it recently introduced negative interest rates,” WSJ wrote this morning. “Signs are emerging of higher demand for safes—a place where the interest rate on cash is always zero, no matter what the central bank does.”

“In response to negative interest rates, there are elderly people who’re thinking of keeping their money under a mattress,” one saleswoman at a Shimachu store in eastern Tokyo told The Journal, which also says at least one model costing $700 is sold out and won’t be available again for a month.

“According to the BOJ theory, they should have moved their funds into riskier but higher-earning assets. Instead, they moved into pure cash that earned nothing,” Richard Katz, author of The Oriental Economist newsletter wrote this month.

Meanwhile, in Switzerland, circulation of the 1,000 franc note soared 17% last year in the wake of the SNB’s move to NIRP.

“One consequence of the decision to cut the Swiss central bank’s deposit rate into negative territory in late 2014, and deepen the negative rate to -0.75% early last year, may have been to increase stockpiling,” WSJ reports. “Holding money in cash would protect it from the risk of Swiss banks at some point charging a broad range of customers to deposit money.”

“The connection between the increasing circulation of the big Swiss bill and the central bank policy is obvious,” Karsten Junius, chief economist at Bank J. Safra Sarasin said. Well yes, it is. Just as the connection between soaring safe sales in Japan and Haruhiko Kuroda’s NIRP push is readily apparent.

So once again, we see that when one experiments with policies that fly in the face of logic (like charging people to hold their money), there are very often unintended consqeuences and when you combine sluggish demand with NIRP in a monetary regime that still has physical banknotes, you get a run on cash. And on safes to store it in.

And then this from “Demand For Big Bills Soars As Japan Stuffs Safes With 10,000-Yen Notes“:

“Demand for 10,000-yen bills is steadily rising in Japan, even as the nation’s population falls and the use of credit cards and other forms of electronic payment increases,” Bloomberg writes. “While more cash might sound like a good thing, some economists are concerned that it shows Japanese households are squirreling away money at home instead of investing it or putting it into bank accounts — where it can make its way back into the financial system and be put to productive use.”

One safe maker who spoke to Bloomberg said safe shipments have doubled over the last six months. While part of the demand for safes is likely attributable to the country’s new “My Number” initiative, “the negative-rate policy is likely to intensify the preference of Japanese households to keep cash at home,” Hideo Kumano, an economist at Dai-ichi Life Research Institute said. “Overall, the trend of more cash at home reflects concern about the outlook for economy among households. This isn’t a good thing.”

No it isn’t, and not because of concern about the outlook for the Japanese economy: that had no chance long before Abe and Kuroda came on the scene, mostly as a result of Japan’s demographic spiral of doomed.

“It isn’t a good thing” because it confirms that the global run on physical cash – as much as the bankers of the world would like to keep it under wraps – has begun, and as the chart above shows, in a fractionally-reserved world in which there are $10 in savers’ claims for every $1 in physical currency, it quite literally pays to panic first, as the 9 out of 10 people who panic after the first one, will be stuck with nothing.

* * *

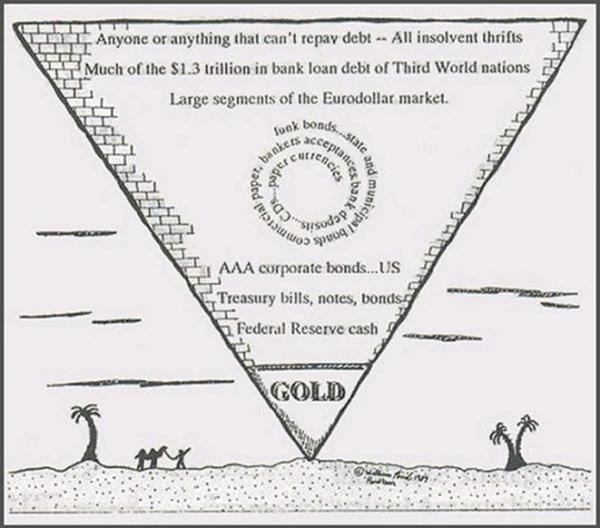

At the end of the day, what it all boils down to, is Exter’s inverted pyramid. As a reminder, this is how Elliott’s Paul Singer summarized the total notional value of all global asset classes:

- Over-the-Counter derivatives, notional amounts: $692 trillion at year-end 2014, per the BIS. For comparison, this figure was $72 trillion in 1998.

- Global real estate: $180 trillion, according to global real-estate services provider Savills.

- Global debt market, both securities and other forms of debt: $161 trillion at year-end 2014, per the Institute for International Finance’s Capital Markets Monitor. According to the Bank of International Settlements (BIS), debt securities make up $95 trillion of this total.

- Global equities: $64 trillion, per the World Federation of Exchanges.

- Global M1 money supply: $24 trillion at year-end 2013, per the World Bank.

- Gold: $6.8 trillion at year-end 2013, according to the Thompson Reuters GFMS Gold Survey.

Because once the banks’ physical cash runs out in a post-NIRP scramble, there is always – at least until it, too, is confiscated once again – gold.

Source: The Global Run On Physical Cash Has Begun: Why It Pays To Panic First – ZeroHedge