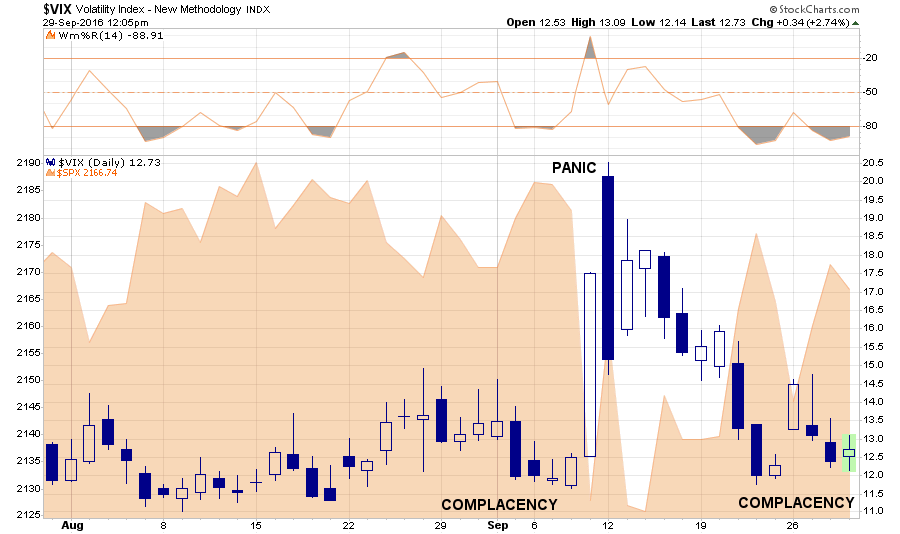

In last weekend’s newsletter, I discussed the “round-trip” move of the market following the Fed’s latest announcement to NOT hike rates.

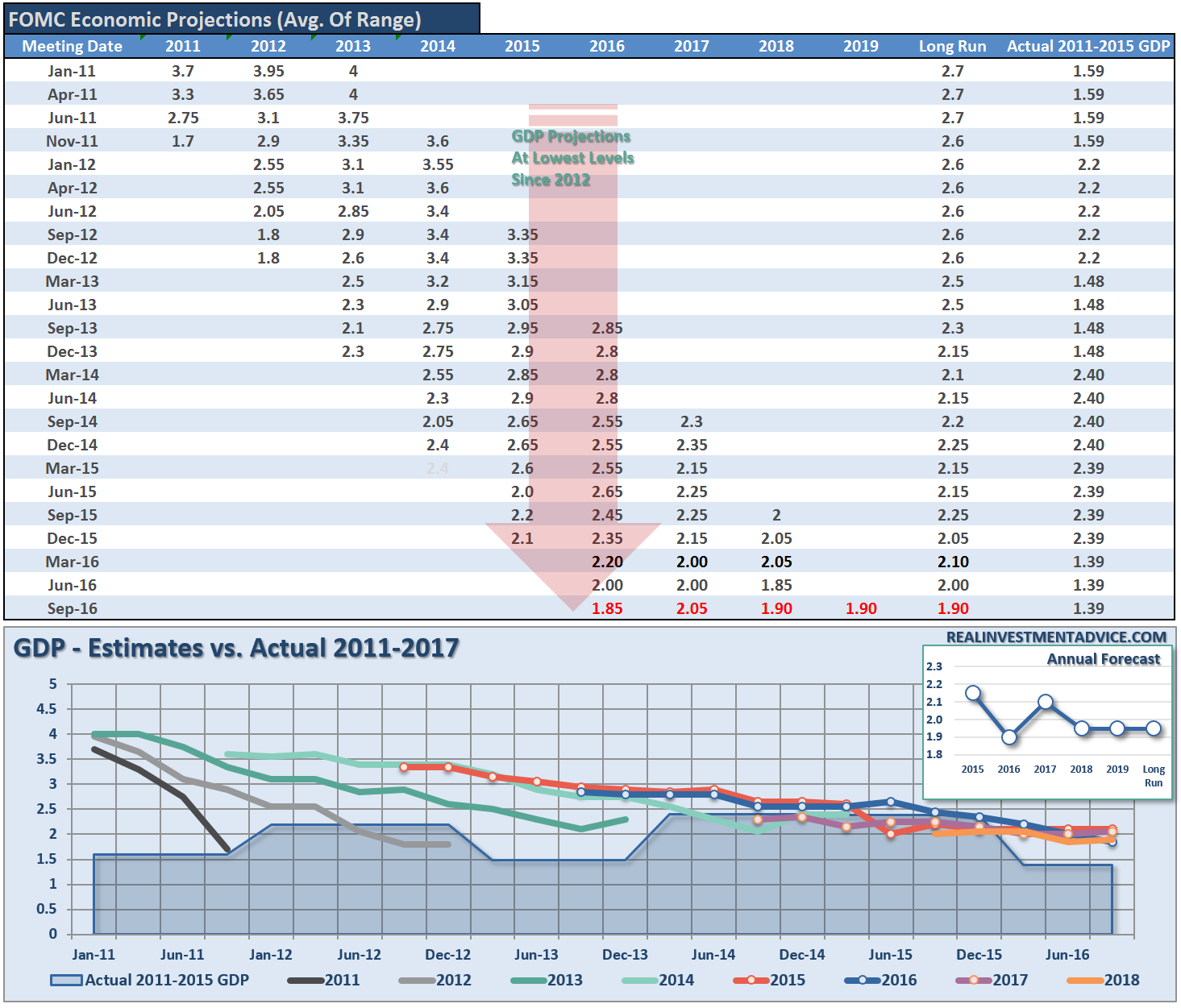

“It is not surprising the Fed once again failed to take action as their expectations for economic growth were once again lowered. In fact, as I have noted previously, the Federal Reserve are the worst economic forecasters on the planet.

As shown in the table/chart below, not only are the expectations for economic growth now the lowest on record, the Fed has given up on 2% growth for the economy with the long-run economic projections now at just 1.9%.”

“This should surprise no one. The Federal Reserve has continued to hope for the last several years that extremely ‘accommodative’ monetary policy, and near zero interest rates, would spark stronger levels of economic activity leading to a rise in broad-based inflationary pressures. Unfortunately, this has yet to be the case.

With the Fed holding still on hiking rates, with a promise to now hike in December (**cough****bullshit****cough), traders came rushing back into the market pushing prices right back into the trading range of the last month.”

The chart below shows the “round-trip” from complacency, to panic, and back to complacency.

Importantly, with the markets testing resistance below the bottom of the trading range in August, the issue becomes whether this bounce is a “sucker’s rally” or the beginning of the next leg higher. I continue to suspect the former as the deviation between prices and fundamentals continue to widen.

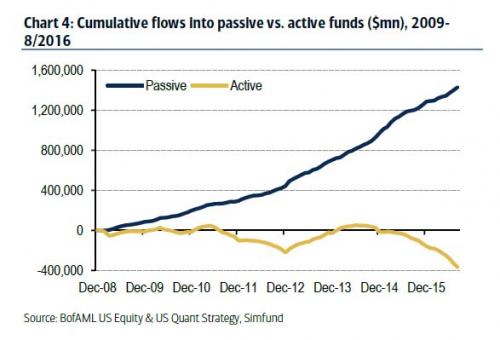

This idea is further supported by the following note from BofAML (via Zerohedge):

“As BofA’s Savita Subramanian reports, over the last several years, we have observed an accelerating trend of flows out of active funds and into passive vehicles. Price sensitivity of investors to fees, coupled with poor performance trends, have conspired against active funds, and year-to-date flows out of active have reached a post-crisis high.“

“The current year outflows from active funds have now surpassed a record $200 billion, with the bulk of cash outflows shifting to much cheaper (and better performing) passive funds, though as BofA notes, flows have slowed since last year suggesting that there may be a broader cash outflow from the equity asset class, as increasingly more Americans retire and pull out of the market entirely.”

The last sentence goes to the heart of what I discussed this past week with respect to “baby boomers” and the “new secular bull market” thesis:

“Old people are living longer and young people are delaying marriage and children. This means fewer people paying into a social welfare system, while more or taking out.

This demographic problem is not going to be fixed anytime soon and has manifested itself in lower rates of household formations. More importantly, the drag from the elderly on the financial system is going to be a much bigger problem than most currently expect.”

The problem is two-fold.

- As an increasing number of individuals begin to extract capital from the market, there will be a rising headwind to the markets which is dependent on cash inflows for advances.

- As Tyler notes, the accelerating transition from active to passive management will end in tears, as passive management only works as long as the rising tide keeps lifting all boats.

As I have discussed previously, while passive indexing works while all prices are rising, the reverse is also true. The problem is that once prices begin to fall the previously “passive indexer” becomes an “active panic seller.” With the flood of money into “passive index” and “yield funds,” the tables are once again set for a dramatic and damaging ending.

Why do I say that? Because we have seen this occur repeatedly in the markets. In the late 90’s everyone was piling into Technology stocks. Heading into 2007, it was all about real estate. Today it is passive indexing and Robo-Advisors.

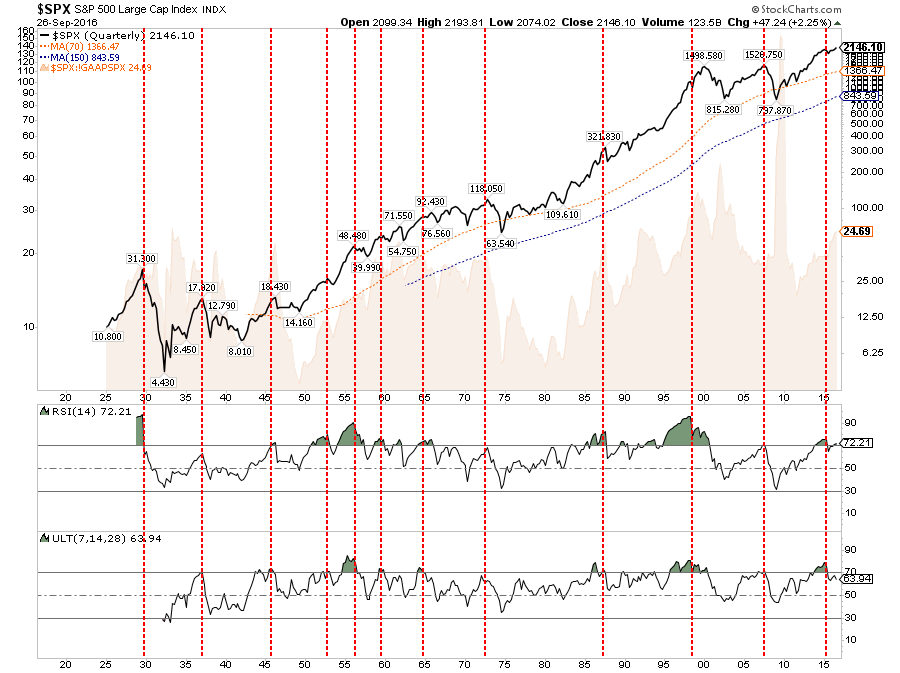

It is only near peaks in extended bull markets that logic is dismissed for the seemingly easiest trend to make money. Today is no different as the chart below shows the odds are stacked against substantial market gains from current levels.

But, in the meantime, here is what I am reading this weekend.

Fed / Economy

- PIMCO: Global Economy About The 3-P’s by Elena Holodny via BI

- Yellen Refutes Trumps Partisan Charges by Nathan Bomey via USA Today

- Economy Overheating Or Stuck via Reuters

- I Trashed The Economy As Fed Head by Mark Gilbert via Bloomberg

- Alan Greenspan Confused Again by Jeffrey Snider via Alhambra Partners

- Negative Rates Aren’t Working by Paul Kupiec & Alex Pollock via RCM

- Evidence Of Brexit Vote by Allister Heath via The Telegraph

- Rules Vs. Discretion by Narayana Kocherlakota via Brookings

- No Hillary, Tax Cuts Don’t Cause Recessions by Thomas Del Beccaro via Forbes

- Yellen May Quit If Trump Wins by Steve Goldstein via MarketWatch

- Is An Economy Reliant On Yellen Worth Saving? by John Tamny via RCM

- Central Banks Double Down On Failure by Stephen Roach via MarketWatch

- The Fed’s Path To Economic Hell via John Mauldin via Forbes

- Half Of Middle Class Lives Paycheck-To-Checkbook by Karol Markowicz via NY Post

Markets

- Passive Investors Unite by Danielle DiMartino-Booth via Money Strong

- 50-Slides For Gold Bulls by Akin Oyedele via BI

- The Ted Spread Isn’t Dead by Jesse Felder via The Felder Report

- October: Worst Month Of Election Year by Jeff Hirsch via Almanac Trader

- Profit Margins Fortell Credit Cycles by Daniel Oliver via Myrmikan Research

- Are Stocks In A “Big Fat Ugly Bubble” by Paul La Monica via CNN Money

- How Charts Make You A Better Investor by Michael Kahn via Barron’s

- Most Interesting Charts by J.C. Parets via AllStarCharts

- Sometimes, Just Do Nothing by Joe Calhoun via Alhambra Partners

- Julian Robertson: This Will End In Chaos by Bob Bryan via Business Insider

- A Persistent Profits Recession by Ed Yardeni via Yardeni Research

- Yield Curve. Does It Matter? by The Capital Spectator

- Outflows From Active Funds Surpass Records by Tyler Durden via ZeroHedge

- Fed’s Phony Housing Recovery by Lee Adler via ContraClub

Interesting Reads

- Wells Fargo: A Culture Problem by Bob Bryan via Business Insider

- Stock Charts: How They Work & How To Use Them by Michael Kahn via Barron’s

- 71% Aren’t Saving Enough For Retirement by Rodney Brooks via Washington Post

- 7-Reasons Middle Class Is In Trouble by Sean Williams via USA Today

- ObamaCare’s Death Spiral by Luke Hilgemann via IBD

- The Hot New Millennial Housing Trend by Ilana Strauss via The Atlantic

- The Basket Of Deplorable Investments by Tony Isola

- Yes, Valuations Still Matter by Meb Faber via Faber Research

- Sales Estimates Suggest No Growth by Eric Bush via GaveKal

- Millennials Must Save 22% Of Pay by Darla Mercado via CNBC

- Peak Debt Complacency by Carmen Reinhart via Zerohedge

- Fed: Dope Dealers On Speed-Dial by John Hussman via Hussman Funds

- Trump: We Are In A “Big Fat Ugly Bubble” by David Stockman via Contra Corner

- Stocks Test Post-February Uptrend by Dana Lyons via Tumblr

- Must Watch: Central Bank Independence? by Jesse Felder via The Felder Report

“Acknowledge the complexity of the world and resist the impression that you easily understand it. It’s a basic fact of life that many things ‘everybody knows’ turn out to be wrong.” — Jim Rogers

Questions, comments, suggestions – please email me.